Sector strategy for 2026: Offices to anchor allocations as demographics and technology drive diversification

The Active Capital Survey 2026 series.

The Active Capital Survey 2026 series.

1. Offices are the most targeted sector in the Active Capital Survey by number of respondents (69% plan to target this sector in 2026), albeit less than the proportion of respondents with existing exposure (75%), reflecting common legacy issues.

2. Living sectors are set to be the second most targeted in 2026 (65% of survey respondents) driven by demographic tailwinds and defensive income streams. Within the living sectors, multifamily (46%) and student accommodation (35%) attract the most planned investment by number, while most frequent proportion of allocation to investment is highest in the living sectors for multifamily and co/flex living (10%<20%).

3. Industrial / logistics is a high-conviction sector, attracting 63% of investors. This strength is supported by persistent supply chain challenges, steady e-commerce penetration in select markets, and the sector’s growing role in national resilience and security-related requirements.

4. Retail on the radar 56% of investors are set to target retail indicating opportunities as the sector emerges from its right-sizing phase.

Offices are set to be the top targeted sector in 2026. While being top of the wish list, this is a smaller proportion of respondents than those with existing office holdings (75% of respondents) suggesting conviction remains selective. Investors, particularly institutional are likely to focus on prime, ESG-compliant assets in core CBDs, where there is income resilience. Well-located assets with good bones in secondary geographies, where pricing has adjusted to a level to make refurbishing or repricing accretive are also likely to be of interest.

Source: Knight Frank

Living sectors are set to continue to anchor planned investment allocations for 2026. In terms of living sub-sectors:

Source: Knight Frank

From data centres to infrastructure, commercial real estate investors are widening their net to capture structural headwinds:

While planned investment allocations are set to remain modest on average (typically 1–10%), their inclusion signals a structural shift towards thematic growth and income resilience. The above highlights that demographic changes and technology adoption are shaping sector strategies at least at the fringe.

The survey results indicate that while traditional sectors for now remain the stalwart, thematic diversification and exposure is increasingly on the agenda. Execution risk is likely to be highest in sectors requiring operational expertise, reinforcing the need for partnerships and specialist capability to manage this risk and unlock the necessary returns.

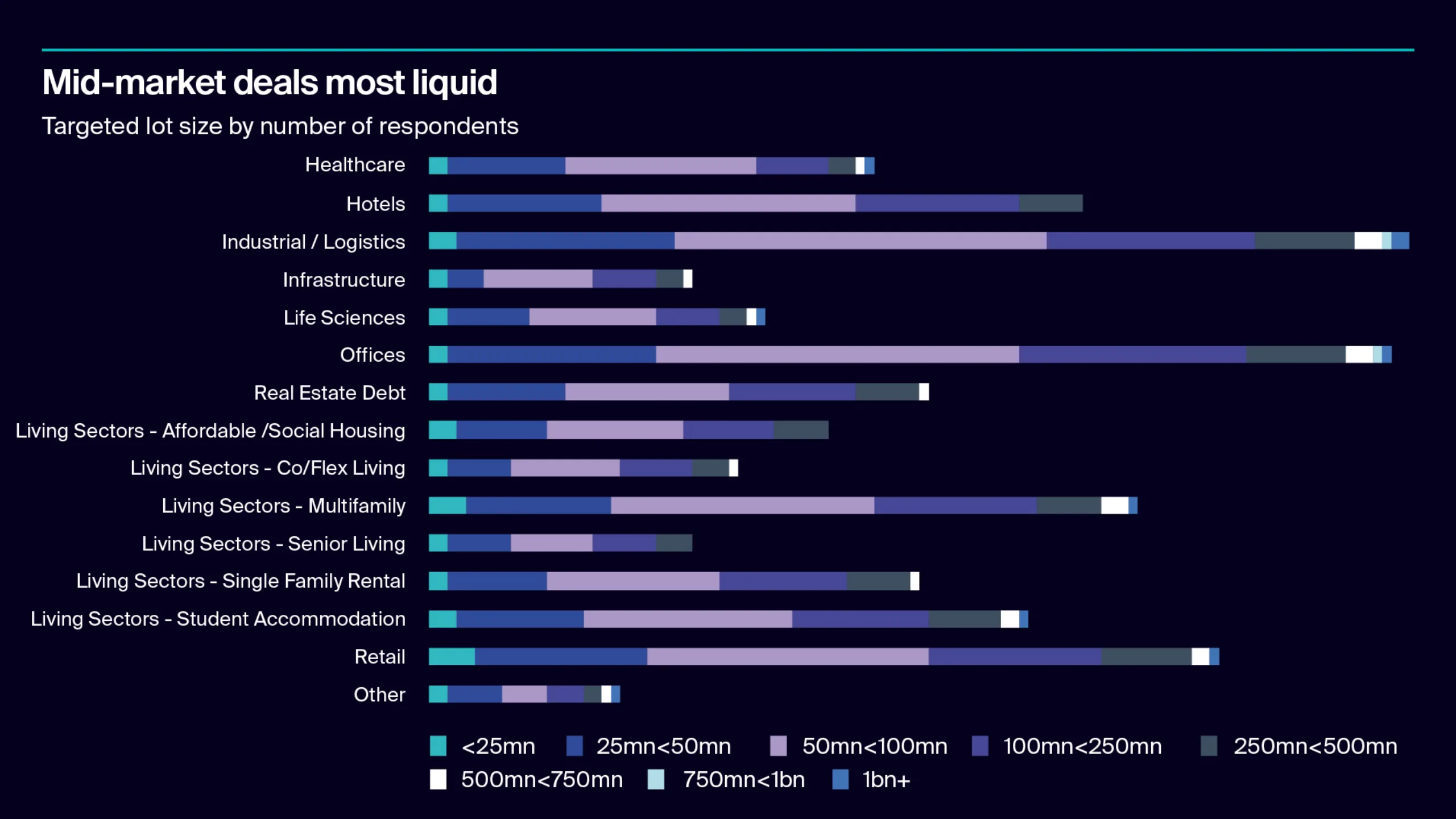

Mid-market deals (50<100 million in respondents chosen currency) will remain the engine of global deployment, striking the balance between meaningful scale and execution efficiency. The survey finds that larger tickets (250 million +) will concentrate in industrial / logistics, offices and retail, while living and operational sectors add depth at smaller sizes on average. Deals in the 50<100 million bracket dominate. The next most liquid ranges are 25<50 million and 100<250 million.

This reflects a market where pricing clarity is emerging selectively and the investment committee favours relatively more bite-sized execution over single-ticket concentration.

Source: Knight Frank

Based on survey intentions, the mid-market is forecast to remain the liquid centre of global CRE investment. The survey does indicate appetite for larger transactions to occur – and this is typical at this stage of the cycle, but it is likely these will occur selectively. They are likely to be anchored in sectors with structural tailwinds and pricing clarity. This also indicates that for some investors, deploying at scale will mean multiple mid-sized positions and / or partnering for access to larger, more complex opportunities.

Sign up to receive regular Active Capital insights.

Explore the rest of our Active Capital insights.

Active Capital

Investor sentiment is shifting from caution to conviction following higher interest rates, pricing uncertainty and constrained liquidity.

20 January 2026

Active Capital

The survey reveals how capital flows, sector priorities and strategic positioning will shape 2026.

20 January 2026

Active Capital

How optimistic investors are targeting direct commercial real estate in 2026.

20 January 2026

Active Capital

Offices will be the top targeted sector in 2026. Investors will likely focus on prime assets in core CBDs where there is income resilience.

20 January 2026

Active Capital

The Active Capital Survey 2026 indicates an investor base delicately balanced between caution and conviction.

20 January 2026

Active Capital

Core investment is set to regain momentum, driven by stabilising debt, narrowing bid–ask spreads and improving return profiles.

20 January 2026

Active Capital

Investor hurdle rates follow a hierarchy across strategies. The gap shows liquidity, complexity, execution risk and market volatility.

20 January 2026

Active Capital

Respondents to the survey identify three dominant opportunity clusters shaping investor strategy for the year ahead.

20 January 2026

Active Capital

The Active Capital Survey 2026 identifies seven tightly clustered forces that will define investment decisions in the year ahead.

20 January 2026

Sorry!

An unexpected error has occurred.

Please try again later.