Finally, an update on MEES for non-domestic real estate in the UK

02 July 2026

If you are in the UK like I am, you will have experienced the second heatwave of the year coinciding – rather ironically - with London Climate Action Week making sustainability even more front of mind. In this edition, I turn to the long-awaited response to the Minimum Energy Efficiency Standards (MEES) consultation into non-domestic real estate (from 2021!) and share my view that we may see more pricing of physical risk in valuations. On a personal note, I will be away for August’s edition but back in September.

The five-year wait is over (ish)

Back in 2021, the then Conservative government consulted on the introduction of more stringent Minimum Energy Efficiency Standards (MEES) for non-domestic buildings. Under current rules buildings require an EPC rating of at least E to be lettable, with the consultation on raising that standard to an EPC B minimum by 2030. Last month, we finally had a response – albeit light on detail and ‘interim’ – confirming the target of EPC B by 2031, but for buildings over 1,000 sqm. The response also removed an interim step mandating buildings to hit EPC C by 2027.

This provides a clearer endpoint for the market, yet compresses decision-making into a single horizon. For landlords, particularly those holding assets of EPC C and below, the focus now shifts from incremental upgrades to whole-building strategy. What remains unclear is how the 1,000 sq m threshold will be applied in practice. EPCs are often assessed at a sub-building level, raising complexity for multi-let, mixed-use and fragmented ownership structures. If implemented at whole-building level, the policy could capture a broader segment of stock than current EPC data indicates.

The cost implications are also uneven. While the government points to £360 million per year in energy savings, retrofit requirements will be significant for parts of the market. The retention of the seven-year payback test, among other elements, offers some flexibility where upgrades are not economically viable, but delivery will depend on access to capital, clarity on exemptions, and supporting fiscal measures.

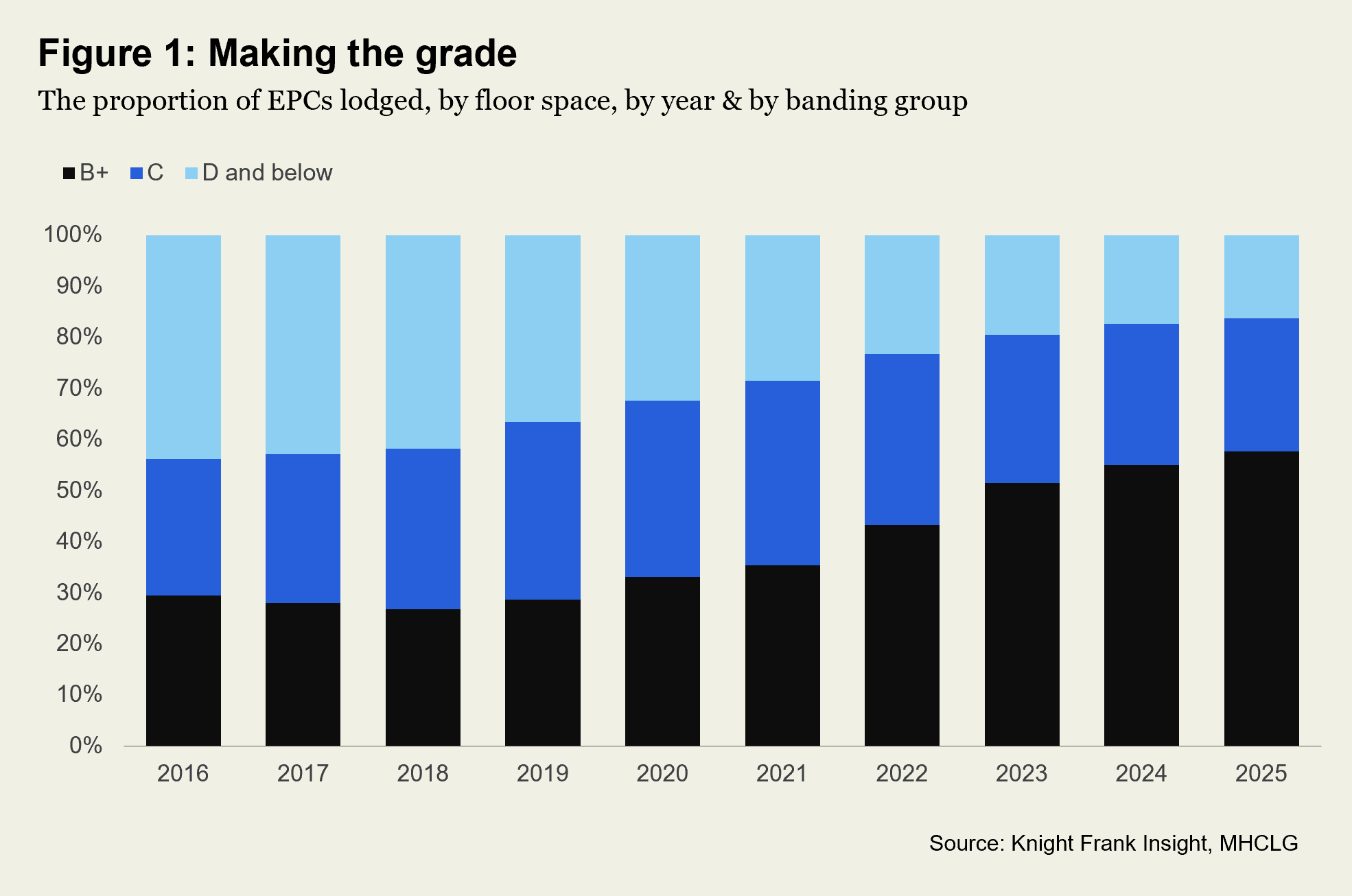

Where are we now?

Market dynamics are already reinforcing this shift. Larger buildings, especially new builds which are easier to electrify, are further advanced. Close to half of floor space assessed for EPC in the last ten years and above 1,000 sq m already achieved an EPC B or higher, but there is still a long way to go. Since the 2021 proposals, some of this progress reflects early action by landlords responding to regulatory risk and investor pressure. However, ratings may have also been supported by changes to EPC methodology, particularly the 2022 shift in electricity and gas carbon factors, which has favoured electrified buildings. As a result, part of the recent uplift reflects recalibration as well as retrofit, raising a broader question over whether EPC B will consistently translate into genuine operational performance.

At the same time, pricing signals continue to sharpen. The ‘flight to quality’ has widened rental differentials, with EPC C-rated and below office space in London seeing an average c.40% discount compared to headline prime rents, although this may not be solely attributable to efficiency performance as other factors such as age of stock and specification are likely to be a factor. Investment strategies are also evolving, with increasing focus on electrification and transition risk, and retrofit costs being priced more systematically into acquisitions.

For occupiers, this signals growing exposure to both disruption and potential cost pass-through. Buildings that fall short of EPC B, particularly above the 1,000 sq m threshold, are increasingly likely to undergo upgrades or repositioning. While this should expand the pool of compliant space over time, near-term retrofit activity may tighten availability and intensify timing pressures around lease events.

How assets are upgraded, not just whether they meet EPC B, will increasingly determine value, liquidity, and occupier appeal. For a deeper dive into the data, market dynamics and occupier implications, see the full piece. Also see this piece around the 2023 changes and what it could mean for business rates.

Is physical risk priced into real estate?

My take is not yet, but the market is moving in that direction. A recent Bloomberg article highlights rising demand from hedge funds and asset managers for natural catastrophe modelling expertise, often drawn from insurance-linked securities markets. This reflects a shift towards quantifying exposure to extreme weather and embedding it into investment decision-making.

The urgency is increasing. The prospect of a “super El Niño” (which is reportedly already underway) and more frequent extreme weather events points to greater volatility, challenging the treatment of physical risk as a long-term issue. Early signs suggest this is translating into financial outcomes. In our 2025 ESG Property Investor survey, 28% of respondents reported higher capital expenditure linked to weather-related damage, while 34% cited increased operational costs, including insurance premiums and energy. Nearly two-thirds of occupiers in our (Y)OUR SPACE survey also identified sustainability as critical to managing financial and operational risk, including business interruption and insurance availability.

The challenge remains how this risk is priced. Frameworks such as TCFD have improved disclosure, but risk metrics may not yet be consistently reflected in valuations. Key questions persist around whether pricing captures reinstatement costs alone or also incorporates income disruption and asset-level value impacts.

Insurance markets provide a leading indicator. Swiss Re estimates the gap reached $424 billion in 2025, while Munich Re data shows weather-related events accounted for 92% of total losses. As insurance becomes more constrained or expensive, this will increasingly feed through into asset pricing, financing conditions and liquidity. Evidence is beginning to emerge, as previously noted, with higher climate risk linked to a measurable increase in cost of capital.

As data improves and financial markets adopt more sophisticated modelling, the mechanisms to embed physical risk into real estate valuations are likely to accelerate.

91% - stat of the month

On the theme of electrification, 91% of executives globally believe it enhances energy security (from a survey of 2,000 across 18 countries by green campaign groups but conducted independently and outside of their membership report in this FT article). This is a dynamic we explored in our (Y)OUR SPACE digest and Real Assets report – it’s a cost and security of supply imperative at play.

What else I am reading

Previously we mentioned the ideas of data centres in space, but now we have operational ones underwater (Guardian) – powered by wind, Ofgem announce possibility of flexibility in demand connections, the UK unveils £1.3 billion of battery investment plans (Net Zero Investor) and taken a ‘significant step forward’ in the development of long duration electricity storage.

Sign up to Knight Frank Research.