What will it take to get to B by 2031?

With the minimum of EPC B by 2031 restated as intention for non-domestic private rented buildings of 1,000 sqm or more we look at where we currently are and why.

02 July 2026

The five-year wait is over (ish)

The government’s restated intention to require EPC B for non-domestic rented buildings, albeit only those over 1,000 sq m, by 2031 brings long-awaited direction, but leaves key questions unanswered. After nearly five years since the initial 2021 consultation, the policy trajectory is clearer. Yet, this still requires secondary legislation and more detail on the delivery mechanisms and detailed implementation.

The removal of the interim 2027 milestone simplifies the pathway but compresses decision-making into a single compliance horizon. In practice, this shifts focus from incremental improvement to whole-building strategy - particularly for assets that remain below EPC C today.

Crucially, the announcement introduced the 1,000 sq m threshold. This is perhaps as targeting larger buildings could have a disproportionate impact due to higher energy use, whilst potentially excluding smaller, more capital-constrained holdings from the most stringent requirements. However, the extent to which this objective is realised will depend on whether the threshold is applied at building or unit level, with EPCs often assessed at a sub-building level. This would potentially be a particularly difficult implementation for multi-let, mixed-use or fragmented ownership structures.

Where are we now?

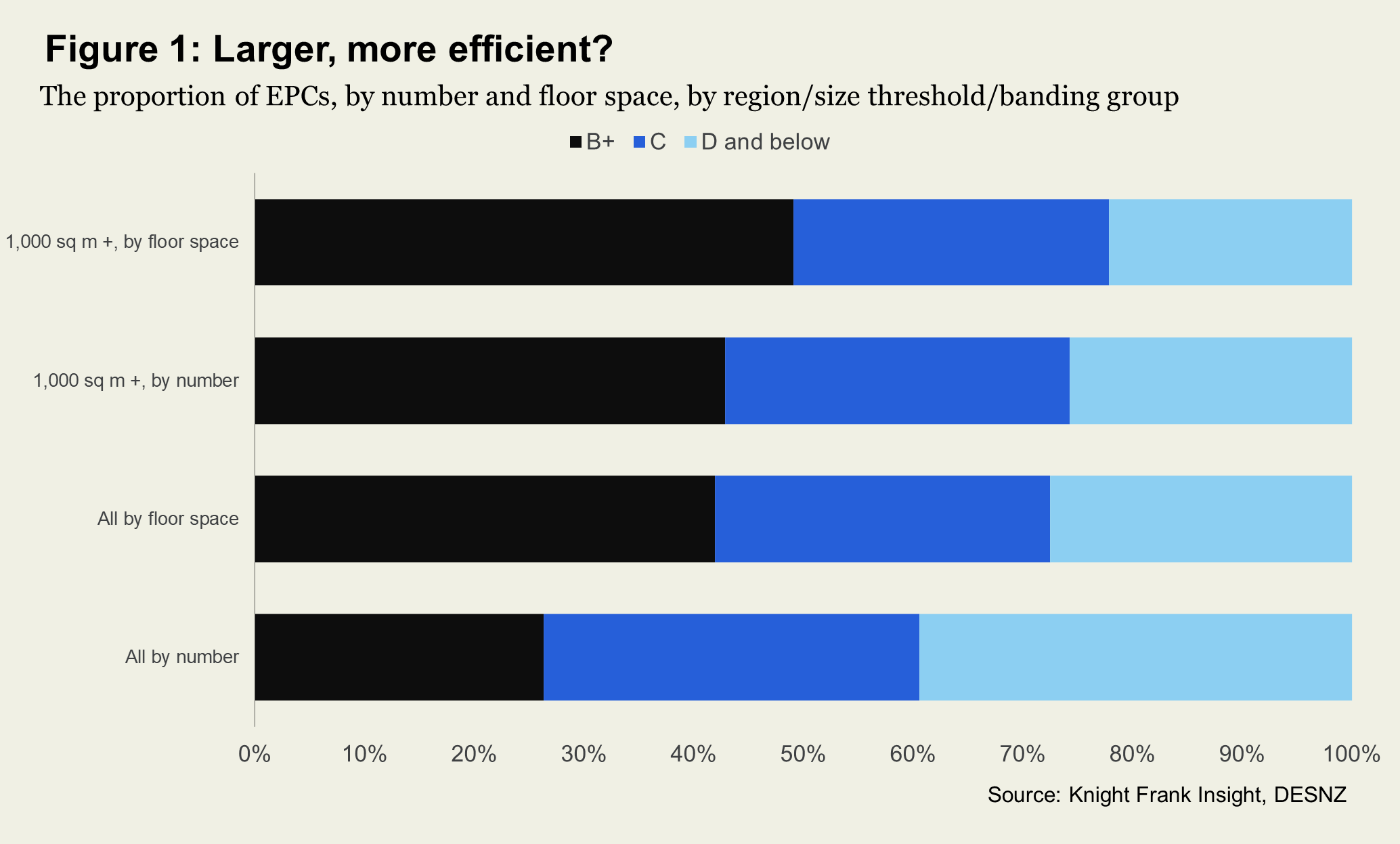

Larger buildings appear better positioned, but this is partly structural rather than purely performance-driven. Over the past decade, EPC B-rated units have averaged around 1,100 sq m, compared with c.600 sq m for C-rated stock and under 500 sq m for D-rated and below. Looking specifically at assets over 1,000 sq m, almost half (49%) of floor space is already EPC B or higher, although this falls to 43% by number (see Figure 1). While this is a more positive picture than the entire stock (42% of floor space EPC B+ or 26% by number), If applied at a whole-building level, the policy would capture a broader share of stock than current EPC data suggests - there is still a long way to go in five years.

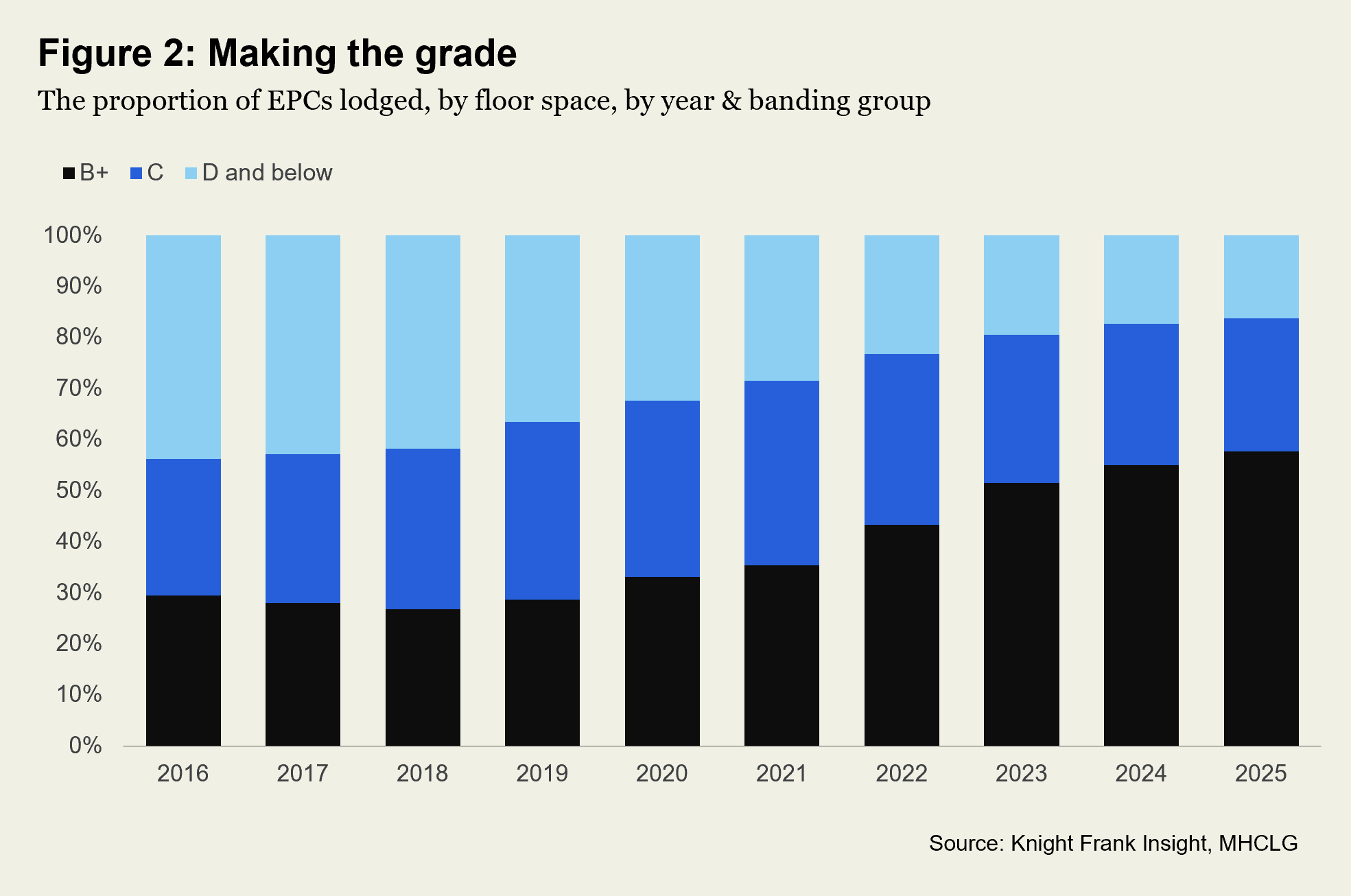

This reflects a combination of scale effects, where newer institutional assets dominate, early movement following the original policy proposals, and methodological changes. Across all EPCs lodged since 2021, by floor space, more than half have been rated B or higher, compared to around 35% for the five years prior (Figure 2). This is partly driven by new-build supply: around one third of floor space in our dataset relates to certificates issued due to ‘mandatory issue (property on construction)’, of which 95% is rated B or higher.

The 2022 update to EPC calculations reduced the carbon intensity attributed to electricity and increased that for gas, accelerating apparent ratings improvement, particularly for electrified buildings. More than half of EPC B-rated floor space is now electrically heated, compared with roughly a third of C-rated and below.

As a result, part of the recent improvement may reflects recalibration rather than physical retrofit. Buildings assessed pre-2022 may already see rating uplift on reassessment, creating a near-term ‘paper gain’ that could soften the immediate compliance gap, but work in reverse for those where gas is the primary fuel.

Market forces are already moving

Regulation is only part of the story. Market dynamics, particularly rental performance and liquidity, are accelerating the shift.

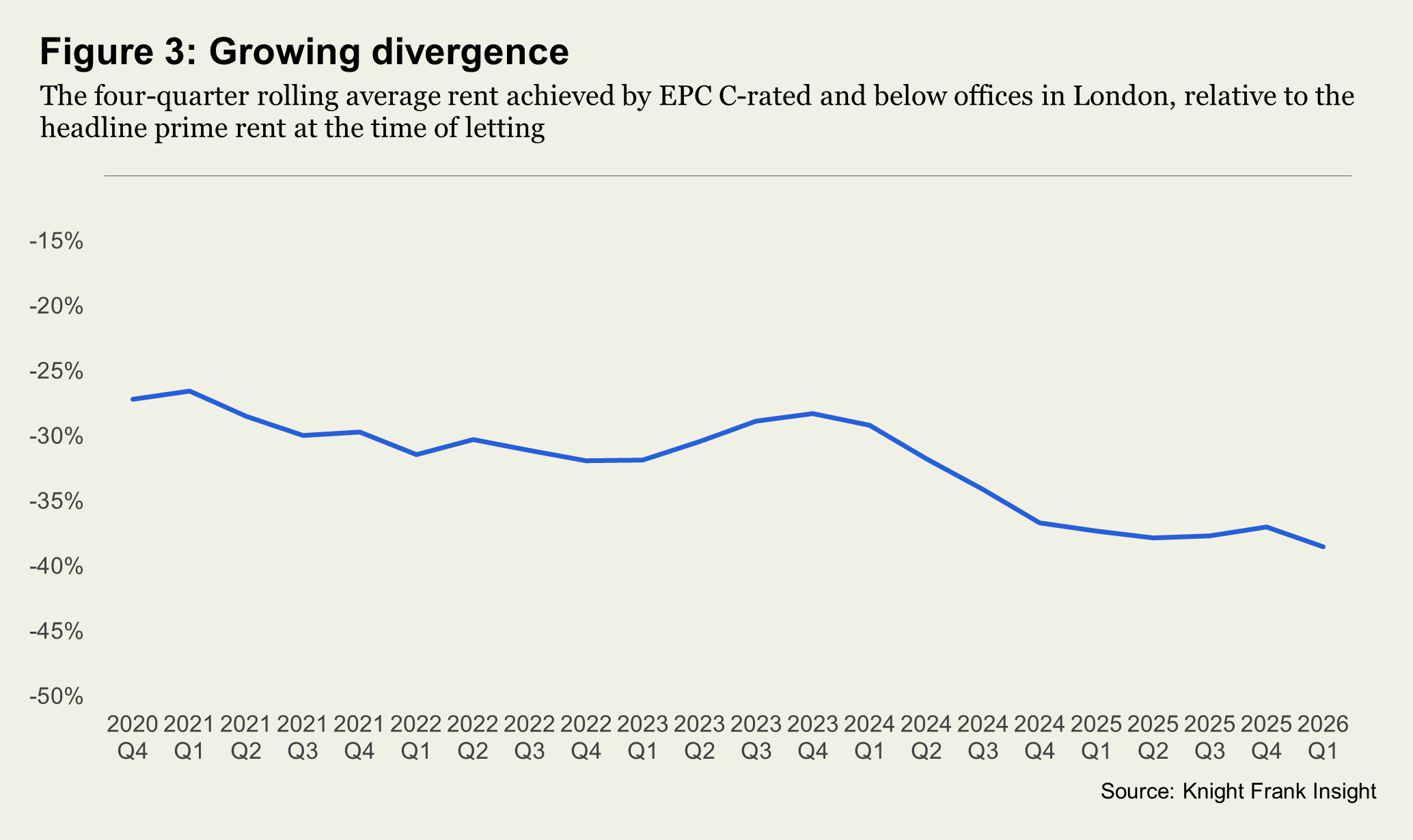

The post-pandemic ‘flight to quality’ has driven a widening gap in rental performance. Analysis of London office lettings shows that EPC C-rated (and below) assets have seen their discount to headline prime rents increase from around 27% at the end of 2020 to close to 40% more recently (Figure 3). However, this is likely not solely attributable to efficiency performance as other factors such as age of stock and specification are likely to be correlated and influence. As explored in our Meeting the Commercial Retrofit Challenge series, this divergence could widen further. Furthermore, analysis shows that the average lease length for those A or B-rated has been around one year longer than those rated C and below, with a four-quarter rolling average of c.7 years compared to c.5.8 years.

On the investment side, sustainability metrics are increasingly embedded in acquisition strategies. Listed real estate companies are targeting portfolios that are 100% EPC B or above by 2030, while our survey data indicates that around 26% of investors actively screen for fully electrified buildings. Where assets are not yet compliant, anticipated retrofit costs are now routinely priced into underwriting.

What does this mean for the occupiers?

The 2031 target shifts occupiers from passive exposure to active participants in building transition. A meaningful share of businesses already report that their buildings require upgrading in the Knight Frank (Y)OUR SPACE survey, regulation now anchors that sentiment to a fixed timeline. For occupiers in sub‑B buildings above 1,000 sq m, intervention is increasingly likely - through retrofit, repositioning, or, in some cases, loss of lettability.

This brings cost and lease dynamics into sharper focus. While capital expenditure will sit with landlords, recovery is likely to be reflected in service charges, green lease provisions, or rent negotiations. Occupiers will need greater visibility on retrofit plans, both to manage disruption and to understand how costs translate into total occupancy.

Supply effects are more nuanced. Retrofit activity should expand the pool of compliant space over time, but short-term disruption and stock withdrawal risk tightening availability. This reinforces the importance of timing around lease events. In practice, occupiers should assess EPC exposure across portfolios, engage early with landlords, and look beyond ratings to underlying energy performance and alignment with internal net zero targets.

For owner-occupiers the regulation does not apply. However, if there are considerations for potential future sale and leaseback strategies, the EPC would potentially be a consideration for value realisation and potential.

A market transition underway

The shift to EPC B is less about headline compliance and more about underlying performance. While overall efficiency is improving, progress remains uneven, driven primarily by larger, newer and more readily electrified assets. A substantial share of stock still faces exposure to tightening standards, capital expenditure requirements, and weakening liquidity where upgrade pathways are unclear.

As policy, pricing and occupier expectations converge, the focus will move from whether a building meets EPC B to how it performs in practice - particularly in terms of energy intensity, cost stability and resilience. For investors and occupiers alike, this signals a transition from rating-led decision making to performance-led strategy, where the quality of upgrade and operational outcomes becomes as important as achieving the threshold itself.

Sign up to Knight Frank Research.