Physical risks priced, asset owner views and sustainability in the Alps

In this edition, we explore how physical climate risk is influencing the cost of capital, how alpine resorts are adapting to climate change, and what SMEs and asset owners are doing around sustainability. We’d also like your perspective – if you think something is missing from today’s sustainability conversation in property, or you have a burning question, please share your thoughts on the link below.

06 November 2025

Physical climate, AI and continued momentum

Back in August 2023, I wrote about AI's potential role in ESG and real estate, now we are seeing it play out. Surveys from Deloitte, Bain & Company & Capgemini show that 60 to 80% of companies now use AI in sustainability efforts, with efficiency and optimisation cited as primary drivers and this is likely to apply to their real estate. Matt Hayes explores this further for occupiers in the latest Talking Points.

Now Norway’s Wealth Fund, Norges Bank Investment Management, has spotlighted AI in its new Climate Action Plan, prioritising embedding AI and proprietary analytics to streamline climate risk management and decision-making. Their analysis warns of “meaningful losses at the portfolio level even under current global emissions trajectory of the global economy”.

Norges Bank also commits to an enhanced focus on nature, physical climate risk, adaptation and resilience. Analysis by Bloomberg reinforces this, with exposure to physical risk linked to a higher weighted average cost of capital - +22bps per +10 climate risk points. This relationship held across sectors and regions, though asset-level risks appear to be the key driver.

While much of this is focused on equities and at the company level, there are direct reads for real estate: future-proofing asset value means factoring in physical climate impacts. Deloitte reports that 33% of companies rank the 'operational impact of weather-related disasters/extreme weather' as a top concern, with a quarter citing rising insurance costs or limited availability – echoing findings from our 2025 ESG Property Investor Survey.

Insurance is a major lever, but equally other aspects of real estate and business are likely to be impacted. From construction delays from extreme weather, supply chain disruptions and rising costs - food, for example is now experiencing 'climateflation' according to the Energy & Climate Intelligence Unit in the UK. Business interruption and CapEx impacts were also noted by a quarter of respondents in our 2025 Survey.

Regardless, physical climate risks will become paramount to understand at an asset level to ensure future resilience. As Semafor notes, the focus of COP30, starting in Brazil next week, is likely to shift from “how to avert climate change, to how to survive it.”

Resilience of the alpine resort

This is especially true in regions where climate underpins the economy, like the Alps. Physical climate considerations are central to investment and property decisions. That’s why the 17th edition of the Alpine Report introduces the Alpine Sustainability Index, assessing snow reliability and long-term resilience. It’s not all about risk, many resorts now offer year-round living.

Val Thorens, Courchevel 1850, and Val d’Isère top the French rankings, with Zermatt and Verbier also earning 5-star ratings. Kate Everett-Allen, the report’s author, notes that lower-altitude resorts with less snow reliability are diversifying to stay competitive, investing in climate-smart infrastructure and year-round offerings.

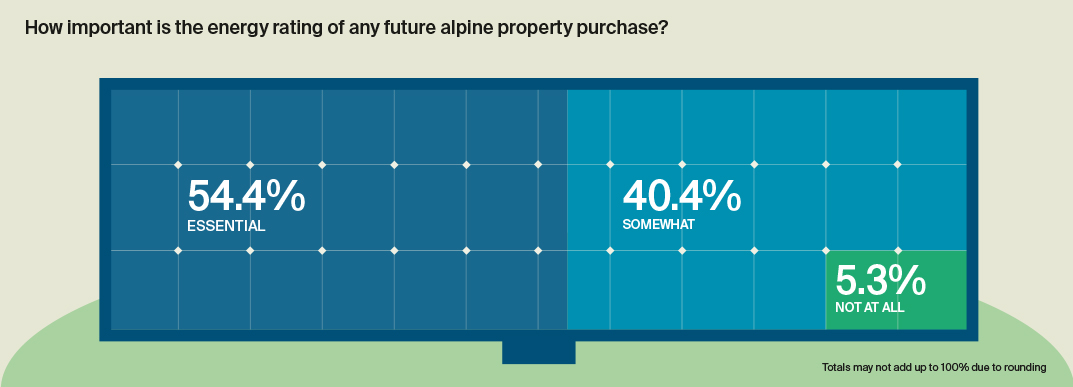

Energy efficiency is also rising in importance. Some 54% of prospective buyers see energy ratings as essential, and 40% as somewhat important. In part, this reflects new regulation - France requires minimum EPC ratings of F by 2028 and E by 2034 for rentals - something which may become more prominent in the UK should proposed rental changes come to fruition.

The report offers a wealth of information on all things alpine, including the top price performers, what €1 million buys across the mountains, the 'best for' recommendations and much more.

More on the continuation of ESG...

This month, we explore the asset owner perspective, drawing on Morningstar’s survey of over 500 asset owners representing $19.1 trillion in AUM. While not specific to real estate, the findings matter given 22.6% of AUM is allocated to private markets, reinforcing ESG’s importance across property sectors.

ESG is increasingly seen as part of fiduciary duty. In fact, 61% of respondents now say ESG aligns with fiduciary responsibilities, up from 53% last year. Integration continues to rise: 20% apply ESG to over 75% of their AUM, and 10% apply it across all assets. The average level of integration now stands at 44%, up six points since 2022.

Notably, stakeholder pressure has overtaken regulation as the primary driver of ESG adoption. This shift highlights how ESG is becoming embedded across investment and procurement chains and not just among large corporates, as shown in the UK Net Zero Business Census and British Business Bank’s specific SME Report, with focus sharper and real estate playing a role.

Last year, I highlighted the need for simplified ESG strategies in real estate focused on five REs, including reducing energy use and switching to renewables. The Census and Report show that while only 11% of SMEs have formal net-zero targets, 77% have taken emissions lowering steps, notably:

- energy efficiency measures (taken by 59% of SMEs and 76% of medium-sized businesses);

- waste reduction (55%/71%); and

- switching to renewables (33%/74%).

This demonstrates a clear trend toward electrified and green-energy-supplied buildings as it is directly linked to operational expenditure and efficiency. We’ve previously discussed practical ways to implement that here, and it’s encouraging to see it gaining traction among businesses of all sizes.

On the regulations

Morningstar found that 46% of asset owners view recent regulatory rollbacks as a step backward, versus 27% who support them. A growing majority (55%) see regulation as helpful and more importantly, consistency is what is needed to spur action, yet there is a lot happening in this arena.

The ongoing EU Omnibus proposals were approved by EU Legal Affairs Committee, but were narrowly rejected by EU Parliament indicating there is more to go - with some calling for more and some for less reductions in scope. The Committee Approved elements stated:

• Corporate Sustainability Reporting Directive (CSRD) and Taxonomy disclosures scope reduced to companies with >1,000 employees and >€450m turnover (previously 250 employees >€40m turnover or >€20m in assets). This reduces companies in scope by 80%

• Large firms can’t demand extra data beyond voluntary standards developed by EFRAG; sector-specific reporting becomes optional.

• Corporate Sustainability Due Diligence Directive (CSDDD), only to apply to companies with >5,000 employees and >€1.5bn turnover and non-EU firms with EU turnover >€1.5bn turnover (previously the thresholds were 500 employees >€150m turnover)

We will be watching this closely, yet clarity and continuity of regulation is one element that the real estate industry has been calling out for.

In the UK, the Scottish government has confirmed new Energy Performance of Buildings (Scotland) Regulations 2025, effective from 31st October 2026. The changes include, among other elements: new EPC rating system for domestic buildings focusing on fabric efficiency, emissions, efficiency and running costs of the heating system, and cost of energy to run the home; new EPC rating system for non-domestic buildings; EPC validity reduced to five years for both domestic and non-domestic. For England and Wales, we have to wait a little longer with The Warm Homes Plan, which will hopefully add clarity and direction for EPCs in the domestic and non-domestic sector, being delayed until later in 2025.

Stat of the month - 57%

What's in a name? While two thirds of assets owners in the Morningstar survey still report using ESG as a term (69%), mostly for the sake of consistency, a shift is noted with 'Sustainable investment' the preference of 57%, 'Sustainability', and 'Responsible investment’ follow, chosen by 53% and 52% respectively.

What else I am reading

UK Government publish Carbon Budget and Growth Delivery Plan and Clean Energy Jobs Plan, aiming to create 400,000 'green jobs' over the next five years, Nobel Prize winner for Chemistry sucks water from the air as is targeting data centres as customers, NESO has delayed the connections reform timeline for customer notifications by three months, consumer insights from Which? show appetite for heat pumps but barriers remain.

Sign up to Knight Frank Research.