Business Rates and EPCs: A new area of value adjustment?

From April 2026, EPC ratings may directly impact rateable values for commercial property, creating potential financial consequences for occupier and landlords of F- and G-rated assets.

02 July 2026

Since 1 April 2023, the Minimum Energy Efficiency Standards (MEES) for non-domestic property have required all let commercial assets, across both new and existing leases, to hold an EPC rating of at least E. Landlords are prohibited from continuing to let substandard properties (rated F or G) unless a valid exemption is registered.

While MEES has been in place for several years, it has only now become relevant to business rates valuations. With the start of the 2026 Rating List (based on April 2024 values), valuers can explicitly factor in regulatory constraints such as MEES when assessing rateable value. This marks an important shift, not just one of compliance but a priced-in factor affecting property value and business rates payable.

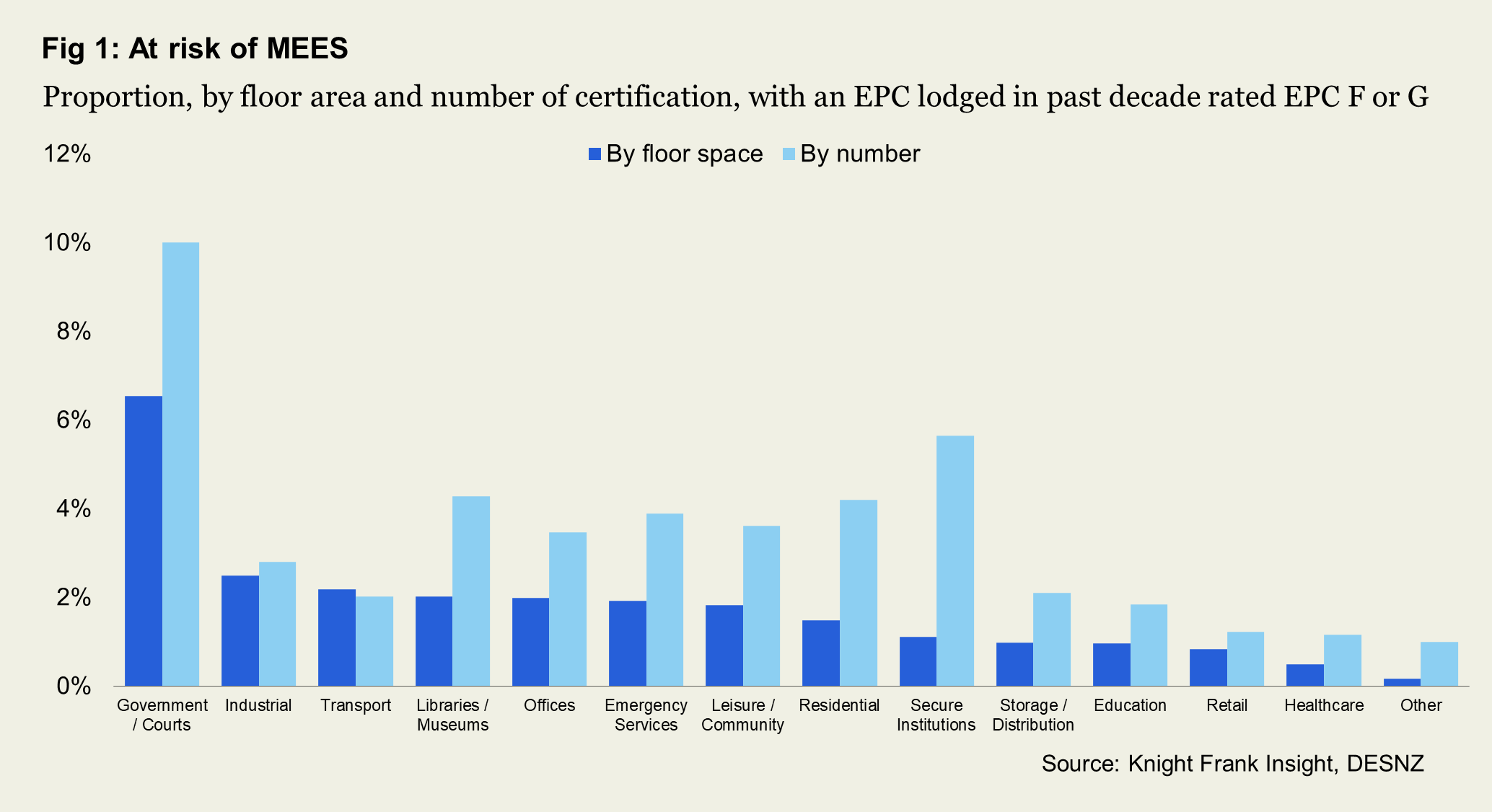

How much stock could be affected?

According to analysis of non-domestic EPCs lodged in the past 10 years, where only the latest for a building is counted around 1.4% of total floor space (c.2% by number of assets) is rated F or G. Variation by sector is material (see Fig 1), for example in Healthcare it is around 0.5%, but for Government/Courts certificates it is 6.5%. While relatively small in aggregate, the implications could be critical for the occupiers. In practice, some of these assets may qualify for exemptions or fail the MEES “payback test”, limiting required intervention and potential knock-on effects.

A hidden risk?

Another key but potentially overlooked dynamic is the June 2022 change in EPC calculation methodology, which reduced the carbon intensity attributed to electricity and increased that for gas, reflecting grid decarbonisation.

This has two important implications:

- Electrically heated buildings (including heat pumps) typically perform better in EPC assessments

- Gas-heated buildings are more exposed to rating deterioration upon reassessment

Of properties rated F or G before June 2022, c.33% used electric heating and may see their rating improve if re-assessed without intervention. Conversely of those rated E (i.e. currently compliant), more than half are noted to have gas as the main heating fuel and, if reassessed without intervention, may see their rating fall below the MEES requirement.

MEES in a bit more depth

There is the important nuance that MEES does not apply universally. Key exclusions include:

- Owner-occupier buildings

- Temporary buildings

- Small detached units (<50 sqm)

- Places of worship

- Certain industrial or agricultural buildings

- Some listed buildings where improvements would be inappropriate

Where MEES does apply, landlords are only required to implement improvements that pass a “seven-year payback test”. Enforcement is financial (penalties), rather than a direct obligation to carry out works. There are also a number of other exemptions such as: Lack of third-party consent (e.g. tenant, planning); Material devaluation (>5%) or all relevant improvements already completed.

What this could mean for business rates

To understand what this could mean on the ground, Simon Berkely, Partner in Knight Frank’s Business rates team, adds his thoughts:

“From the start of the 2026 Rating List, Rateable Values can now take account of the Government legislation in respect of EPCs and the restrictions placed on letting buildings with an EPC rating of F or G.

“The exact impact is likely to vary on a case-by-case basis, depending on the works required to improve the EPC Rating to a lettable standard, the impact of the EPC Rating on value and the impact of any potential penalty for continuing with a letting. Whilst there is a prohibition on letting a building with an EPC rating of F or G, the property may still be capable of being occupied by the owner. It is therefore likely that a substandard EPC rating will result in a reduced Rateable Value rather than fully reducing it to £0.”

“In Rating, there is a presumption that a property is in a reasonable state of repair. For some properties, simply changing the lightbulbs may be sufficient to improve its EPC Rating, and these minor works must be ignored for the purposes of Rating.

“However, if the works required to put a property back into a condition fit for occupation go beyond what a reasonable landlord would consider to be economic, this can be considered when setting the Rateable Value. Furthermore, for more substantial improvement works it may be possible to remove the property from business rates altogether during the course of those works.

A developing but increasing issue

This is a new and evolving area. With the 2026 Rating List now open to appeals, there is limited precedent on how MEES will be reflected in practice. However, this will become increasingly material with the UK Government confirming the intention, subject to secondary legislation, to raise the MEES threshold to EPC B by 2030/31 for larger (1,000 sqm) buildings (we take a look at this in more depth here).

For landlords, and occupiers, the implication is clear that EPC performance is directly linked to value, liquidity and tax exposure.

Sign up to Knight Frank Research.