Powering property and private capital

Energy has rarely been so prominent. From the ongoing conflict in the Middle East to the political focus on electricity prices for households and businesses, power is firmly a strategic issue. In this update I explore what this means for occupiers, and how the resulting pressure is bringing energy infrastructure to the fore for private capital.

14 May 2026

A new constraint on corporate real estate?

Energy is rapidly becoming a binding constraint in corporate real estate decision-making. Electricity demand is rising sharply as electrification accelerates alongside digitalisation and innovation, with data centres the most visible pressure point. The IEA projects global electricity demand from data centres will more than double to around 950 TWh by 2030, while Knight Frank forecasts data centre capacity growth of almost 25% over the next two years. This surge in demand is colliding with ageing grid infrastructure, increased power price volatility and constrained grid connection availability.

Geopolitics has intensified these pressures, with policy focus firmly on cost and security. The UK government has pledged to ”double down not back down” on its renewable rollout, alongside plans to decouple electricity prices from gas to support electrification and clean energy. Recent announcements include migrating legacy renewables into quasi CfD-style structures through voluntary long-term fixed contracts, and increasing the Electricity Generators Levy on ‘extraordinary revenues’ - currently set above £82.61/MWh (CPI indexed) - from 45% to 55% from July 2026. This sits alongside the British Industrial Competitiveness Scheme, extending support to a further 3,000 businesses, which is slated to see eligible firms’ bills cut by up to 25% from April 2027.

Regardless of policy intervention, occupiers are treating power availability, cost and carbon as strategic inputs rather than background utilities. A growing number are turning to long-term power purchase agreements to secure capacity and price certainty, particularly through the UK Corporate Power Purchase Agreement market (as previously spoken about). Publicly announced CPPA activity peaked at 21 deals in 2024 and remained elevated at 17 in 2025, well above pre 2022 levels, reflecting a structural response to wholesale market volatility. Several additional agreements have already been announced this year.

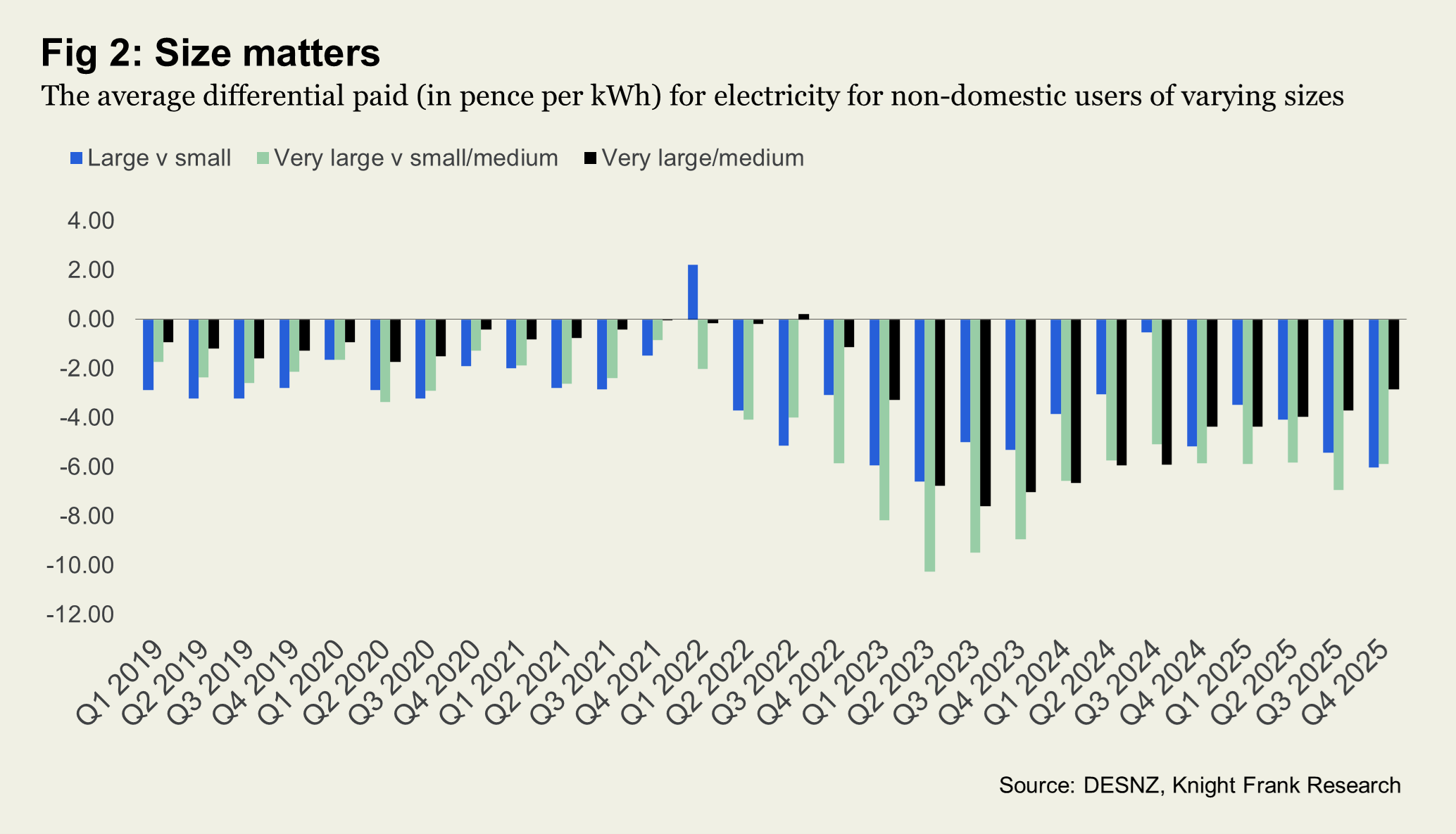

In the upcoming Knight Frank (Y)OUR SPACE digest we explore these routes to power and the considerations shaping procurement decisions - understanding future demand, power price drivers and the carbon implications of different models. Central to all three is high-quality energy data and scale. In the UK, the gap between electricity prices paid by very large users and small and medium users widened sharply after the 2022 price spike, increasing from an average 2.1 p/kWh in 2019 21 to 6.6 p/kWh in 2022 23, before easing marginally to 6.1 p/kWh in 2025.

The direction of travel is clear. Assets offering scalable power, credible low‑carbon supply and operational flexibility will likely attract tenants and capital, while constrained locations risk obsolescence. Energy strategy is fast becoming central to future‑proofing real estate portfolios.

Private capital is turning this into an opportunity

As power becomes a constraint for occupiers, it is also reshaping capital allocation decisions. This helps explain why private capital is increasingly targeting energy and digital infrastructure rather than viewing power as a background utility. “We are hugely bought into digital infrastructure, not just data centres, but utility projects that are powering data centres,” noted one respondent to our Family Office Survey for The Wealth Report 2026.

Last year, 28% of respondents had invested in solar generation, with a further 22% planning to. Battery storage was less established, with 20% already invested, but interest was rising sharply, with 29% looking to deploy capital. Bloomberg recently labelled 2026 ‘The Year of the Battery’.

This momentum reflects a broader structural shift. As outlined above, the global economy is electrifying rapidly. Heat pumps, electric vehicle fleets and energy intensive AI driven data centres are driving a sharp rise in power demand. Grid and generation capacity are struggling to keep pace, and investors, including professionalised private capital, are recognising the strategic value of infrastructure that can close this gap.

The economics are reinforcing the case. In its World Energy Outlook 2025, the IEA projects global energy demand rising 15.5% between 2024 and 2035, while renewable supply is expected to increase by 72%, still short of what is required. However, Ember’s Global Electricity Review 2026 shows momentum accelerating. In 2025, growth in clean power exceeded growth in electricity demand, with solar meeting 75% of additional demand and renewables overtaking coal as the largest source of electricity generation.

Battery economics are central to this shift. Ember reports battery costs fell 20% in 2024 and a further 45% in 2025, with global deployment rising 46% to around 250 GWh. This is materially improving system flexibility. In 2025, enough battery capacity was installed to shift 14% of new solar generation from midday to other hours. For power systems, this is critical to reduce intermittency risk and overall support the transition.

Rising energy costs and capacity constraints are also pushing efficiency higher up the agenda. Our review of nearly 50 public real estate sustainability reports from 2025 shows energy initiatives delivering measurable financial returns. This is not philanthropy. It is about value, resilience and long term competitiveness. With policy moving in the same direction, in the UK and more broadly across Europe, buildings with secure, affordable and efficiently used power are becoming a key determinant of asset performance.

$170 million - Stat of the month

Could energy and digital infrastructure be going out of this world? Washington based start up Starcloud has raised $170 million to build data centres in space. This aligns with something I covered in this year’s Wealth Report about “space in space” and its growing utility. Increasingly explored for solar power potential (UK government feasibility study here), but also for data centres and even semiconductor manufacturing (The Economist), space offers unique properties, including vacuum conditions. Long pivotal to energy efficiency through satellite imagery, the value of the space economy, and its link to real estate, continues to grow.

Sign up to Knight Frank Research.