“Double down, not back down”: what the UK government's recent energy announcements mean

It has been a busy time in UK energy policy. Speaking at the National Growth Debate on 21 April, Energy Secretary Ed Miliband was explicit that the government intends to “double down, not back down” on the clean energy transition.

22 April 2026

The announcements were framed against a stark backdrop. The UK is experiencing its second fossil fuel crisis in under five years, with Miliband’s arguing that “we can’t solve a fossil fuel crisis with more fossil fuels”. For investors and asset owners, the signal is clear: energy security, economic growth and decarbonisation are now treated as mutually reinforcing objectives, not competing ones.

A new paradigm of energy security

Energy security was repositioned as a core economic issue. UK exposure to volatile fossil fuel markets has already fallen, with renewables rising from 7% of electricity generation in 2010 to over 50% today (Figure 1). Government-cited ECIU analysis suggests wind reduced wholesale electricity prices by up to 25% in 2024 by displacing gas at the margin.

This framing mirrors developments elsewhere. Spain has been relatively insulated from price spikes as renewables generate close to 60% of power (80% National emission-free generation at the time of writing), while accelerated solar deployment is evident across Europe and emerging markets following Russia’s invasion of Ukraine. Clean power is increasingly positioned as critical national infrastructure rather than a net zero add-on.

Faster delivery: planning, grid and land

The government’s first priority is speed. The government committed to faster deployment through bringing forward the next renewables Contracts for Difference auction round (AR8), after previous record-breaking auction volumes, and progressing the largest nuclear build programme in half a century.

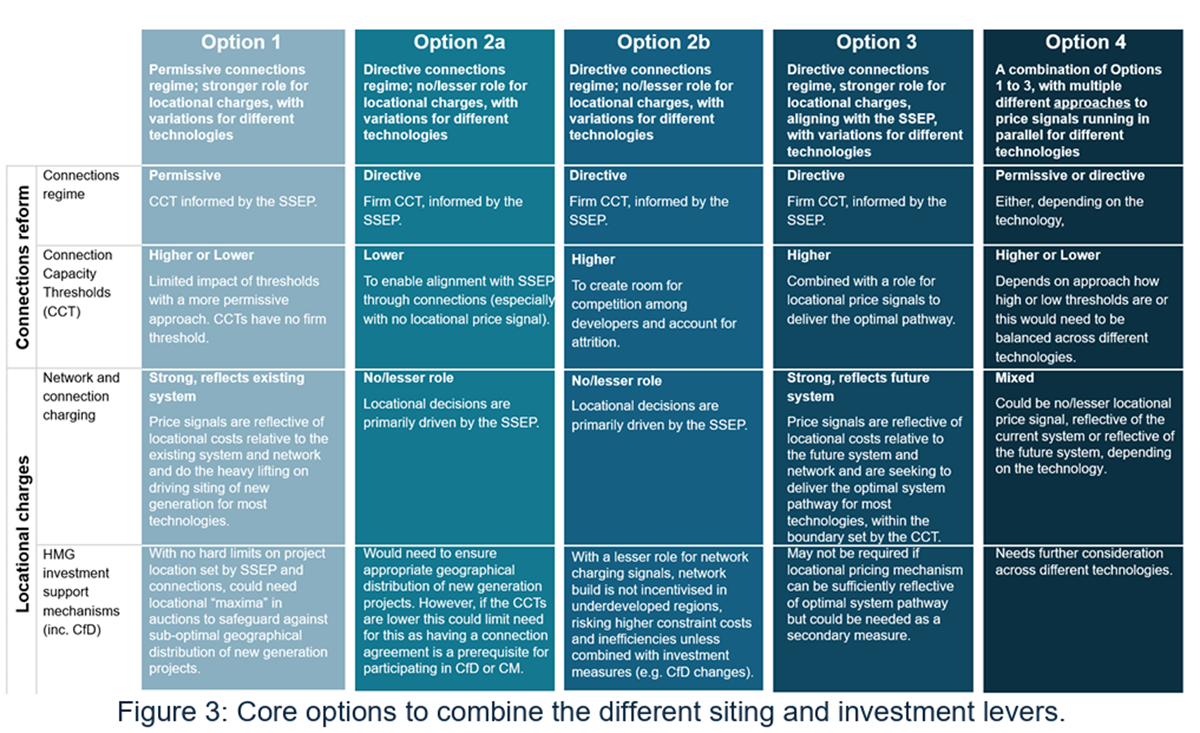

More material for developers was the acknowledgement that planning, grid capacity and land access remain binding constraints. Alongside pledges to accelerate grid infrastructure and remove “irrational bureaucratic barriers”, the Reformed National Pricing (RNP): delivery plan was published. Key elements are:

- reforming siting and investment levers to support delivery of the Strategic Spatial Energy Plan, alongside Ofgem’s Call for Input on network charges. The government noted a preference for doing this through Options 2a, 2b and 3 as Figure 2 below.

- reducing network constraint costs, with NESO estimating that accelerating three transmission projects could save around £4 billion in 2030

- improving system operability, including reforms to Balancing Mechanism participation thresholds, with decisions expected in late 2026 following NESO's Call for Input.

Figure 2: Government options on siting and investment levers

Source: Knight Frank Insight, DESNZ

Public land also emerged as a delivery lever. GB Energy will work with Network Rail, the MoD and Forestry England to deploy solar and storage on underused sites. Government estimates suggest around 10 GW of capacity could be unlocked using only a fraction of available land.

They also released a document confirming that they would take forward all proposals in Electricity network infrastructure: consents, land access and rights consultation. These included increasing the size of substation eligible for Permitted Development Rights from 29 meters to 45 meters as well as making approvals easier for temporary overhead lines, small utility buildings and extensions at existing substations

Electrification at scale

The second pillar is electrification. Heat pumps, rooftop solar and EVs are being advanced through the Future Homes Standard as well as confirmation to make them easier and cheaper to install, with a notably pragmatic tone. Falling EV prices, improved economics and fewer practical barriers are framed as consumer choices rather than ideological positions.

For real estate, the implications are clear. Buildings are increasingly energy assets. Electrification, on-site generation and flexibility are becoming central to operating costs, resilience and occupier demand. Data centres and logistics/industrial assets have been at the fore of this, both as higher energy users with power a key determinant in location and demand, and as demand drivers for energy. More broadly, there are opportunities for assets in terms of flexibility and reduced operational costs but also those capable of hosting EV charging, as we highlight in our recent report, may be able to turn grey space into income generating ones through EV hubs on strategic transport routes.

Repricing power

The third theme was electricity pricing reform. The government reaffirmed its intention to de-link power prices from gas, noting that gas now sets prices around 60% of the time, down from 90% in the early 2020s, with an ambition to halve this again by 2030.

They announced two key changes: migrating legacy renewables into quasi CfD style structures ia voluntary long-term contracts; and increasing the Electricity Generators Levy - charged on ‘extraordinary revenues’ currently set as excess of £82.61/MWh (CPI indexed) - from 45% to 55% starting in July 2026. The aim is reduce volatility for consumers while providing revenue certainty for generators.

What this means for real estate

For energy-intensive occupiers, these announcements sit alongside the British Industrial Competitiveness Scheme, extending bill support to an extra 3,000 businesses from April 2027, bringing to total to 10,000. Yet, delays to new domestic EPC methodologies and silence on non-domestic efficiency standards point to a widening gap between building-level regulation and a rapidly evolving energy system.

For owners and occupiers, energy cost volatility, grid access and decarbonisation readiness are becoming increasingly important for asset performance. Those aligned to electrification and flexibility could outperform (a quarter of investors seek all-electric according to our ESG Property Investor Survey) while those dependent on inflexible, high-carbon energy may face rising risk.

As Miliband concluded, the challenge is no longer how to avoid the next shock, but how to build an energy and economic system resilient to an age of geopolitical instability. These announcements reinforce that delivery, not intent, will define the transition.

Sign up to Knight Frank Research.