Routes to power: An update on the Corporate Power Purchase Agreement market

As demand for clean energy rises the routes for procurement are broadening with CPPAs offering benefits for energy users and energy project developers alike

22 April 2026

Corporate Power Purchase Agreements (CPPAs) are shifting from a niche procurement tool to an increasingly material route to securing clean, reliable electricity. Rising demand for low‑carbon power, a more volatile energy market, and intensifying grid constraints are drawing a broader set of occupiers and developers into the CPPA space. The direction of travel is clear: as supply–demand imbalances deepen, long‑term offtake arrangements are set to play a more central role in how businesses plan for power.

From early adopters to broader interest

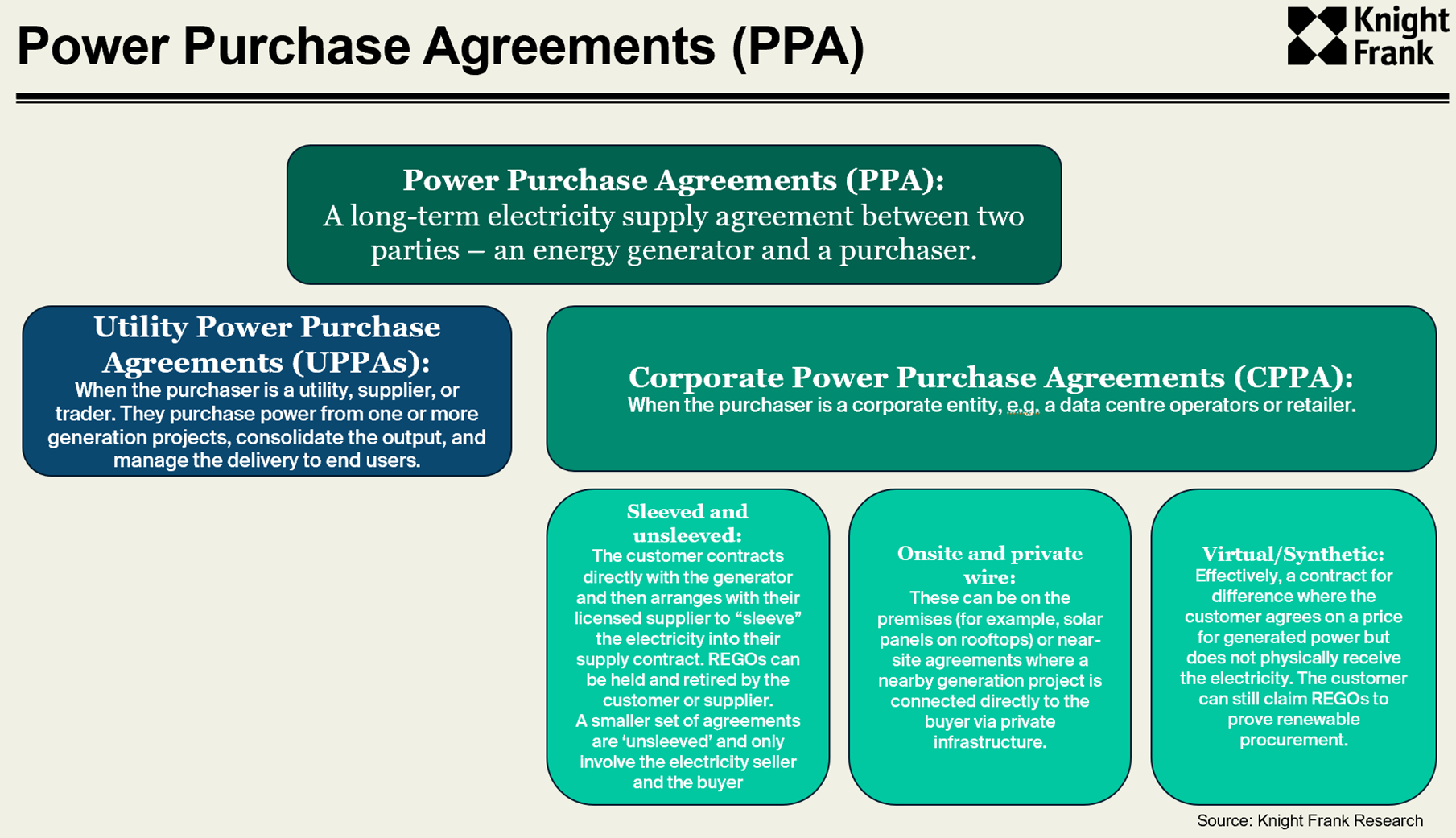

Recognition of this trend is growing across government and industry. Earlier this year the UK government launched a call for evidence on the CPPA market, defining it as any corporate purchaser of a PPA (Figure 1), with virtual or synthetic structures excluded for the purposes of that exercise. While CPPAs themselves are not new, uptake remains constrained by contractual complexity, operational requirements, and limited internal familiarity among many corporates.

Fig 1. CPPA definitions

Globally, the practice is more established, particularly among large technology companies that face rising energy loads and ambitious decarbonisation timelines. In Knight Frank’s Data Centres: Taking Stock of Sustainability report, we noted that cumulative clean‑power contracted capacity has expanded from around 24 GW in 2022 to more than 84 GW by 2025. In the UK alone, Amazon has publicly contracted close to 1 GW of CPPA capacity since 2019. This reinforces the role that large energy users can play in bringing new renewable projects forward.

Why turn to CPPAs

The value proposition for energy users is becoming clearer, many of which we laid out previously article, namely:

- Stable and competitive electricity pricing for businesses by decoupling electricity costs from the wholesale market price.

- Verifiable green energy to meet decarbonisation targets and commitments, CPPAs meet the critical ‘additionality’ metric that REGOs may not.

- Access to power, particularly relevant as power capacity becomes an increasingly important factor in real estate. CPPAs, mostly through direct or private wire could offer opportunity to secure additional power faster than through traditional methods.

For developers and investors, CPPAs create revenue certainty and therefore can enhance project bankability. They can offer superior export rates compared with selling directly into the grid, supporting higher valuations and smoother financing. These dynamics may become more prominent as energy market reforms progress and curtailment risk becomes a more visible constraint.

Sizing the market

Power availability is emerging as a critical factor in real estate decisions. Rising demand is colliding with ageing grid infrastructure, amplifying the premium for energy‑secure assets. New developments are increasingly designed with integrated generation and storage to mitigate connection delays and secure operational resilience. In some cases, power availability is beginning to outweigh traditional location drivers such as proximity or labour catchments.

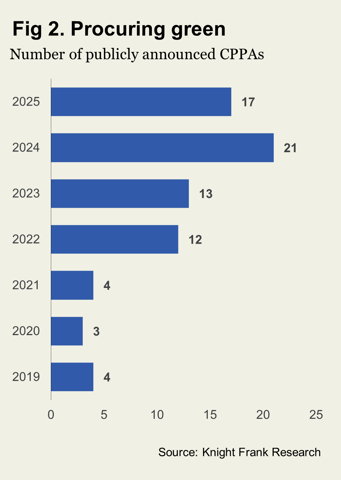

Against this backdrop, more large energy users are exploring CPPA options. Publicly announced activity remains only a partial indicator given the opacity of private‑wire and on‑site deals, yet the trend is evident. Announced UK CPPAs peaked at 21 in 2024 and totalled 17 in 2025, a notable increase compared with pre‑2022 levels before wholesale market volatility escalated. Most tracked agreements are sleeved arrangements, with embedded generation deals typically kept out of the public domain. Early announcements for 2026 suggest further growth, and the government’s call for evidence may lay groundwork for policy adjustments that accelerate adoption.

While CPPAs are unlikely to become a universal solution, they are rapidly becoming a strategic option for businesses facing rising energy loads, investor scrutiny, and constrained infrastructure. For developers, they offer a route to de risking projects in a market where grid constraints are shaping investment decisions. For the real estate sector more broadly, they signal a shift: access to clean, affordable electricity is becoming a competitive differentiator.

Sign up to Knight Frank Research.