Conflict Weighs on Buyer Sentiment as Markets Start Pricing in Middle East Endgame

March 2026 PCL Sales Index: 4,996.2 March 2026 POL Sales Index: 275.5

02 April 2026

The impact of the Middle East conflict on the UK housing market will be both sudden and gradual.

Some of the longer-term effects haven’t yet materialised, which Nationwide house price data underlined this week. Average prices rose by 0.9% in March, which was the strongest monthly gain since December 2024 and took the annual increase to 2.2%.

One key reason for the delayed reaction is that mortgage offers are valid for up to six months, which means buyers are sitting on sub-4% offers that pre-date the conflict. Indeed, there is a strong incentive to act before these favourable offers lapse.

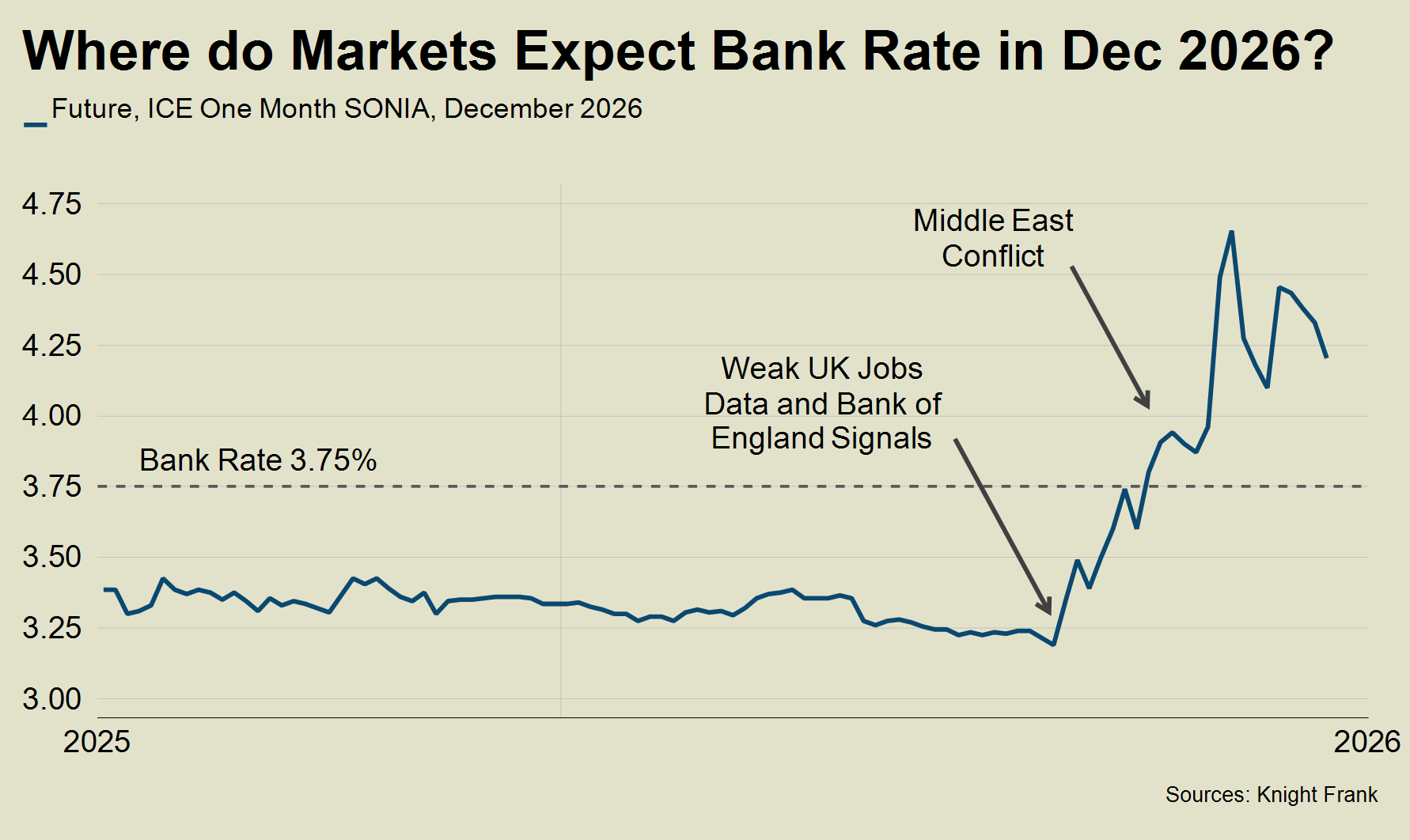

The best five-year fixed-rate mortgages were this week priced close to 5%, compared to just above 3.5% before the conflict began.

Higher borrowing costs will take more time to filter through into the property market. Data this week also showed that mortgage approvals and transaction numbers in February were less than 5% below their five-year average. However, that gap is likely to widen in coming months and downwards price pressure should intensify.

That said, the fact more residential property is owned outright (36%) than with a mortgage (29%) in England will soften the blow to some extent.

Immediate Impact

Meanwhile, the initial impact on the market as the war enters its second month is becoming more obvious.

The number of new prospective buyers registering in March fell 11% year-on-year in the UK, Knight Frank data shows. Demand typically rises as spring approaches, but the figure compares to a smaller 9% drop in February.

As well as the arrival of spring, activity had been building as buyers and sellers put the uncertainty of November’s Budget behind them.

Similarly, the number of offers made fell by 7% in March, compared to a 3% decline in February. The picture is muddied by the introduction of higher rates of stamp duty last April, which increased transaction numbers and may have softened new demand in March 2025.

In London, the number of new prospective buyers was down 6% after having increased 1% in February.

“March was slower than expected given how the year had been unfolding,” said Stuart Bailey, head of prime central London sales at Knight Frank. “It’s too early to tell if demand will eventually increase as a direct result of the conflict in the Middle East but for now, we have certainly seen more people come to the UK to hedge their options by renting in the short-term.”

Price Declines

Average prices in prime London markets continued to fall in March.

In prime central London (PCL), a monthly fall of 0.2% took the annual decline to 4.7%, which compared to a figure of -4.9% in February. In prime outer London, prices fell 0.6% over the year, which followed a 0.5% decline in the previous month.

It means average prices in PCL are 22% below their last peak in mid-2015, which has created a perception of value that is underpinning transactions, said Stuart.

“Prices continue to come down as buyers look for reductions, but they are quickly finding common ground with sellers and deals are holding together.”

Confused Outlook

For now, the outlook in the Middle East remains confused. Financial markets this week were tentatively factoring in a US withdrawal from the region, irrespective of whether it has re-opened the Strait of Hormuz.

Donald Trump’s television address on Wednesday didn’t confirm the withdrawal to the extent some had expected, but neither did he say anything particularly new.

UK 10-year gilt yields were trading below 4.8% on Wednesday after peaking above 5% in March, although markets were still broadly pricing in two Bank Rate rises this year.

“Even if conflict were to end immediately, there will be an inflationary impact from damaged energy infrastructure,” said Pepperstone analyst Michael Brown. “There is still ample reason for caution, but financial markets are for now drawing the logical conclusion that no war is better than war and some Hormuz flows are better than no Hormuz flows.”

We discuss the longer-term ramifications of the war on borrowing costs and the UK housing market on the latest episode of Housing Unpacked. The weak UK jobs market means raising rates may not be an ideal course of action, as we explored here.

That said, the prospect of higher rates due to rising inflation and the need for governments to borrow more in response to the conflict despite already-stretched balance sheets means bond investors may demand higher yields to hold government debt, said Helen Thomas, CEO of political and economic consultancy Blonde Money.

“Weak (bond investor) demand forces yields higher, increasing borrowing costs and potentially triggering a negative feedback loop for public finances,” she wrote in City AM. “This leaves the UK exposed. Markets have demonstrated their willingness to punish perceived fiscal irresponsibility. Hence the government is scared of suggesting anything more than limited, targeted, help over higher energy prices.”

In short, it means the Chancellor’s room for manoeuvre is shrinking, which must increase the likelihood of tax rises in this year’s Budget.

Sign up to Knight Frank Research.