Mortgage Costs Rise as Bank of England Risks Fighting Wrong Inflation War

As upwards pressure grows on borrowing costs, there are questions over whether the Bank of England’s hawkish posture is sustainable.

As upwards pressure grows on borrowing costs, there are questions over whether the Bank of England’s hawkish posture is sustainable.

Almost four weeks into the Middle East conflict, the Bank of England risks fighting its own inflation battle on the wrong front.

As oil and natural gas prices have surged, financial markets have bet central banks will need to raise rates to control inflation.

The Bank of England is expected to increase rates twice this year, which is a notable shift from the position at the end of February, when two cuts were priced in by financial markets.

Its Monetary Policy Committee (MPC) surprised many by voting 9-0 to hold rates last week (with no dissenting votes to cut) and said it “stands ready to act” on inflation, which was widely interpreted to mean rate hikes were on the table.

The Bank may be scarred by the memories of double-digit inflation in 2022 and 2023, when it was arguably too slow to act. However, underlying economic conditions are different today, which means raising rates could be a misstep.

“The Bank almost seems like they’re trying to fight the last war as opposed to this one,” said Pepperstone analyst Michael Brown, speaking on the latest episode of Knight Frank’s Housing Unpacked podcast. “However, almost every economic variable is in a very different, if not the exact opposite, place now compared to where it was in 2022.”

The UK economy is more susceptible to damage from rate hikes due to higher existing rates, a weaker labour market, lower GDP growth and a more punitive tax landscape than four years ago, said Michael.

US President Donald Trump announced this week that talks were taking place between the US and Iran. Irrespective of the competing claims about how true this was, the statement itself was significant as the first sign of de-escalation from Trump, said Michael.

On the podcast, we also discussed how long the inflationary effects from the conflict could last, even if it ended tomorrow, the reasons the UK is more exposed than its G7 counterparts to higher borrowing costs, and whether the current reaction on financial markets could alter the thinking of potential Labour leadership challengers after the May local elections.

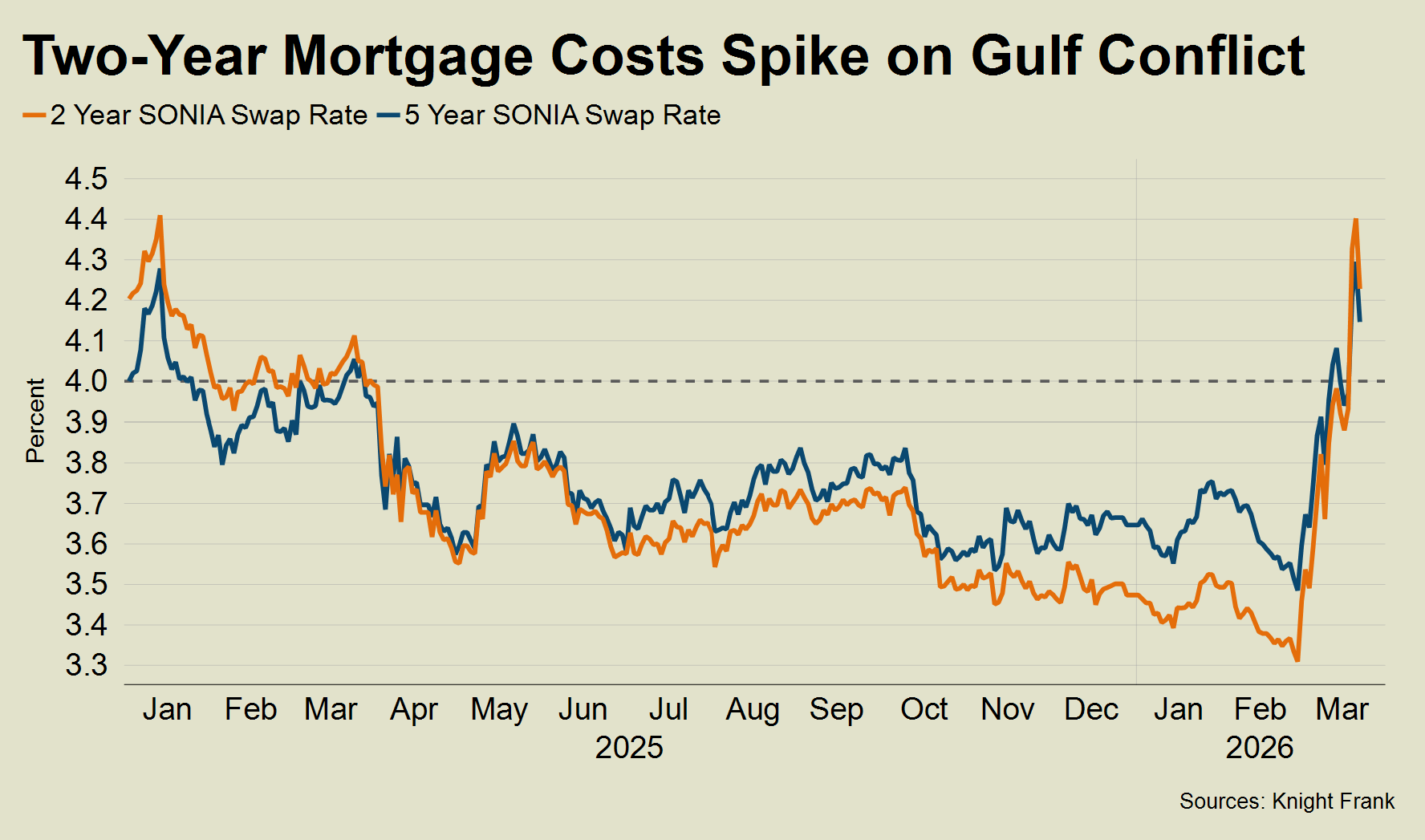

Rising swap rates have pushed fixed-rate mortgages higher in recent weeks, meaning most loans are currently priced above 4.3%, which is similar to the early weeks of 2025.

The two-year swap rate has climbed above the five-year rate in recent weeks, denoting the growing expectation of near-term upwards pressure on rates and the belief that any pressure will subsequently be downwards.

Alongside the negative impact on sentiment from the conflict, higher borrowing costs will put downwards pressure on UK housing transactions and prices in the short-term. Bank of England figures show that mortgage approvals were 10% below the five-year average in January and transactions were 5% down, said HMRC.

Demand had been recovering following the November Budget, which caused hesitation among buyers due to the prolonged speculation over possible tax rises.

Meanwhile, UK house prices rose around 1% in the year to February, according to Halifax and Nationwide. Growth was slightly down from the final months of last year as supply recovered from the Budget more quickly than demand.

Data in coming months will undoubtedly show a higher level of circumspection among buyers and sellers due to the Middle East conflict, which will also feed into the MPC’s thinking when it meets next on 30 April.

Another hold must be the most likely option next month. Whether that is still the most probable outcome closer to the time or whether we see some MPC members vote for a cut depends on how de-escalatory Donald Trump’s latest social media post proves to be.

As Michael euphemistically states on the podcast, the conflict still has “a wide distribution of outcomes”.

Sorry!

An unexpected error has occurred.

Please try again later.