Building low-carbon power for UK properties

13 March 2026

Welcome to the latest Sustainable Property Insights. How we power property, especially in the era of technological innovation, is gaining prominence as a topic. This month’s newsletter is all about the energy transition with a particular focus on the pipeline for investment and bottlenecks in the UK’s push towards renewables. We also discuss a positive step forward for net zero ambitions among institutional asset owners.

Contracts for Difference update: Will projects be delivered on time?

Energy markets remain sensitive to geopolitical risk, with recent events in the Middle East raising concerns over potential disruption to global oil and liquefied natural gas supply. The uncertainty may have pushed already high-up resilience further up the agenda, strengthening the case for domestic renewable capacity. This aligns with the UK’s ambition to at least treble installed renewable generation by 2030. On paper things are going well. A record 14.7 GW of offshore wind, onshore wind, solar and tidal contracts were awarded in the latest Contracts for Difference (CfD) round, the government-led process supporting renewables build out.

However, headline volumes mask familiar delivery challenges. Grid connection delays, supply chain constraints and lengthy planning processes remain decisive factors shaping whether awarded projects reach operation. Analysis of CfD Rounds 1–7 matched to REPD data shows only 22% of awarded capacity is operational, with a further 20% under construction. Almost half of the pipeline is awaiting construction and 13% remains in planning. Even among projects expected online during 2024 25, only 42% are delivering power, underscoring the persistence of delays.

Ofgem’s recent update highlighted ongoing connection delays, even for Gate 2 projects, with 210 projects (62% of all) affected. This means they will have their existing connection date and / or point of connection changed. Additional measures to accelerate connections and support construction readiness will be essential if the full benefits of AR7 are to be realised.

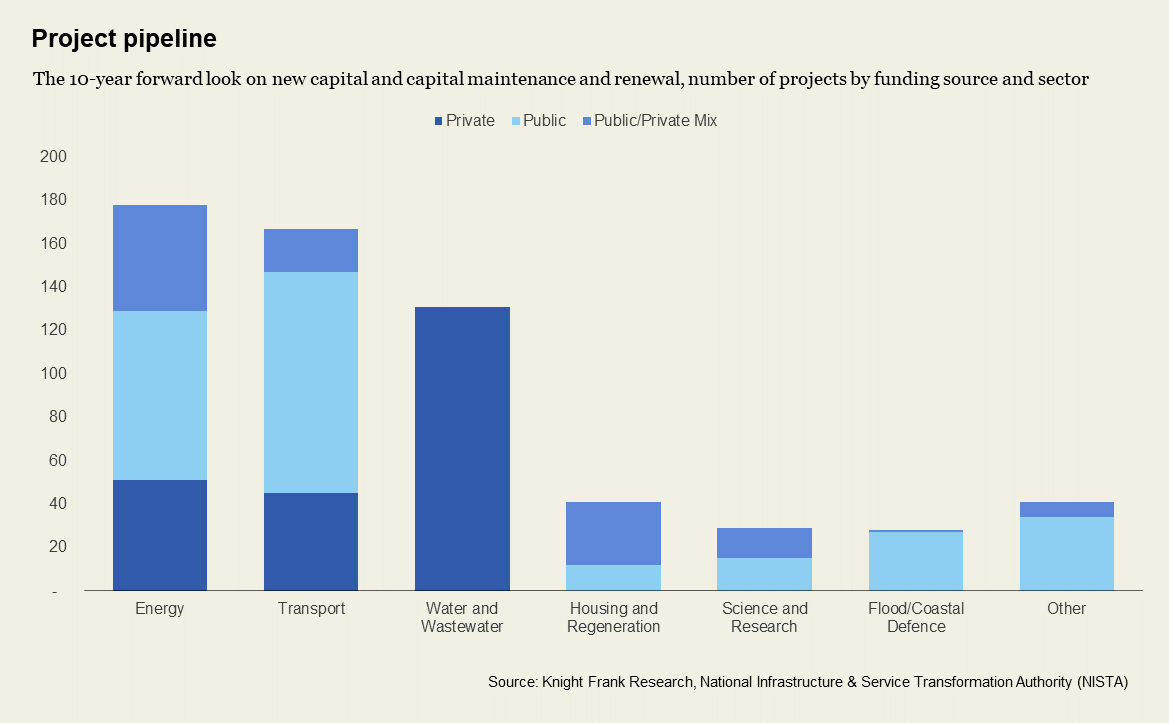

Building future connectivity

The queues for connecting clean energy infrastructure are not unique to the UK. Some 2,800 GW of solar and wind projects globally, including many in late-stage development are held up by connection queues according to the IEA’s World Energy Outlook 2025. This represents both a constraint and a potential opportunity, with value seen in the assets and systems that enable flow, as well as additional generation.

The UK’s updated National Infrastructure Pipeline from NISTA reinforces this shift. It outlines £718 billion of planned investment over the next decade, with roughly half directed towards energy. Of this a large proportion is aimed at transmission upgrades and renewable capacity. The allocation, which is predominantly public or public/private funds, signals intent to clear structural constraints.

The opportunity is echoed in a recent report from Barclay’s: Transition Realism: Financing Energy Systems That Work which highlighted “Value creation is now in the physical bottlenecks of the energy system. It is in underinvested energy infrastructure, in new mining and minerals capacity, and in the firming assets required to maintain system reliability".

For real estate, power constraints have been increasingly noted to influence development viability, operational resilience, and energy procurement. Provision of energy on-site, with rooftop or behind the meter solutions, has been garnering attention, alongside CPPAs, with the potential to provide flexible capacity, as well as enable occupiers to lower emissions and manage energy costs. More of this in the next edition.

250 - Stat of the month

The Net Zero Asset Managers (NZAM) Initiative relaunched in February with 250 signatories. After pausing in 2025 amid concerns over prescriptiveness and feasibility, NZAM has updated its Commitment Statement to better reflect divergent jurisdictional requirements and to streamline actions from ten to seven. More than fifty asset owners, including major pension funds, publicly supported the revision and reaffirmed that addressing climate related risks and transition opportunities is integral to fiduciary duty.

This aligns with my recent conversation with Will Matthews on the Commercial Minded Podcast where we explored why ESG and sustainability must inform strategy rather than sit within reporting cycles. You can find the full discussion here.

What else I am reading

The government published a study on the technical feasibility, costs and economics of space-based solar power which found that wind turbines could be key to the delivery of such mechanisms, the Net Zero Carbon Building Standard updated following pilot, Renewables accounted for 26% of electricity generated in US in 2025, and expected to be 93% of new generation capacity in 2026. Amazon 'trail blazing new low carbon logistics building’.

Sign up to Knight Frank Research.