Procuring renewable power with CPPAs – what are the options and why it matters for occupiers, landlords and renewable developers

Energy use in buildings is under increasing scrutiny, not just for efficiency, but for its source and emissions. There’s a growing demand for fully electric buildings with renewably sourced power, which is now a key topic in real estate and corporate sustainability discussions

26 June 2025

With the UK’s Modern Industrial Strategy highlighting the importance of developing the Corporate Power Purchase Agreements (CPPAs) market, these agreements are gaining traction. However, CPPAs are not a one-size-fits-all solution and must be considered alongside other renewable procurement options. This article explores the main routes to renewable energy, explains how CPPAs work, and assesses the potential demand across the market.

Routes for renewable

How can owners and occupiers secure renewable energy that counts towards emissions reduction targets? There are several ways, with the UK Green Building Council (UKGBC) recommending assessing procurement against three key principles:

- Energy attribute: Exclusive ownership and claim of the renewable electricity’s attributes, either through on-site generation or via Renewable Energy Guarantees of Origin (REGO) certificates. Each REGO represents the zero-emissions attribute of each 1MWh of renewable energy and must be retired to avoid double-counting.

- Renewable source: Energy must come from non-fossil fuel sources such as wind, solar, hydro, biomass, and others.

- Additionality: This principle is met when an organisation either generates its own renewable energy or enters into a contract that directly enables the construction of new renewable facilities. Projects that meet additionality result in real, verifiable emissions reductions by actively increasing renewable generation capacity.

Common procurement routes that meet all three principles are:

- On-site renewable energy: Owned or via a PPA from new, unsubsidised generation (including private wire).

- Off-site renewable energy: A PPA from new, unsubsidised generation or a high-quality green tariff from a supplier offering 100% renewable-sourced tariffs.

In the renewable energy hierarchy, on-site solutions are typically prioritised, followed by private wire, then off-site options that still meet the additionality principle.

What are Corporate Power Purchase Agreements

When on-site or private wire solutions aren’t feasible, which can often be the case in urban settings, a CPPA is often the best route. Here, the energy user (occupier or landlord) contracts directly with renewable generators, bypassing the need for physical proximity.

There are two types of CPPAs:

- Back-to-back: The customer contracts directly with the generator and then arranges with their licensed supplier to “sleeve” the electricity into their supply contract. REGOs can be held and retired by the customer or supplier.

- Virtual (Synthetic): Effectively, a contract for difference where the customer agrees on a price for generated power but does not physically receive the electricity. The customer can still claim REGOs to prove renewable procurement.

Across the real estate market, there are numerous reasons to engage with either type. As noted above, those which prove additionality meet the principles of renewable energy procurement and, therefore, should be prioritised to realise full emisison reduction benefits.

Why do occupiers seek these?

Occupiers with significant power needs may be more inclined towards CPPAs to hedge against volatile electricity prices, gain financial and environmental benefits, and meet ESG targets. The government’s notable support for developing the CPPA market in the Modern Industrial Strategy was as a way to help keep UK energy costs competitive. CPPAs can be procured by single large occupiers or a consortia of smaller ones, often with contracts starting in the future to support new project development, achieving additionality.

The occupiers hail from various uses – offices, industrial, data centres and retail – with larger CPPAs potentially supporting multiple real estate needs. For example, Vodafone secured more than 300 GWh per year for 10 years in two tranches (one announced in 2022 for around 100 GWh and one in for more than 200 GWh from various UK locations). The company’s mobile and fixed networks, data centres, retail stores and offices were now stated to be 100% powered by electricity from renewable sources.

Tech companies have been in the corporate PPA market for a while; Amazon more recently in 2024 signed for 473 MW from a wind farm in Scotland and 159 MW for an East Anglia offshore wind farm to support its goal of 100% renewable power by 2025. Google similarly signed a PPA in 2022 for 100 MW of offshore wind energy.

Across retail, there is a growing demand. In 2024, Tesco secured the UK’s largest solar CPPA for 15 years; the entire project has 373 MW capacity. In 2024, Sainsbury’s signed a 15-year deal for 50 MW from a Scottish wind farm, and H&M entered into an agreement in 2021 for power from two solar stations, which can generate around 50 MW. Industrial and manufacturing occupiers, who typically may go for on-site power generation due to rooftop availability and PPA options, also utilise CPPAs. One example is Britvic securing 3.1 GW of solar energy for factories in Rugby, London and Leeds, and Arla in 2023.

Office occupiers, while typically having lower requirements, are increasingly exploring CPPAs, often in partnership with landlords.

Why would a Landlord enter a CPPA?

Landlords can use CPPAs to enhance the marketability of their assets, lower carbon footprints, and help meet net-zero goals, especially as occupiers increasingly demand renewable power. CPPAs can be arranged for individual buildings or across portfolios.

For example, the City of London Corporation were one of the first in this space signing for a 49 MW solar farm in 2020, covering half of their electricity requirement. British Land notes that they have ‘signed several’ long-term agreements with renewable energy providers to purchase clean energy at a fixed price, and Landsec states they have source ‘100% of our electricity supplies for the sites we manage through our corporate contract from REGO-backed renewable sources’. The critical factor is becoming the quality and provenance as the market matures and understanding grows, particularly around the carbon implications. Procuring renewable energy through new projects, particularly those that are ‘ready to build’ can provide the organisation with real and verifiable emission reduction or emission avoidance.

For renewable developers and investors

CPPAs provide long-term contracts and revenue certainty, de-risking projects and supporting financing. Private wire or CPPA arrangements can offer better export rates than selling to the grid, making projects more attractive for investment and future sale. This may be increasingly relevant as energy market reforms progress.

How big is the market?

Some 90 UK companies have committed to procuring or maintaining 100% renewable energy through their Science Based Targets Initiative (SBTi) commitments, with an average target date of 2029. This figure climbs to around 400 when assessing the broader European markets or more than 550 globally.

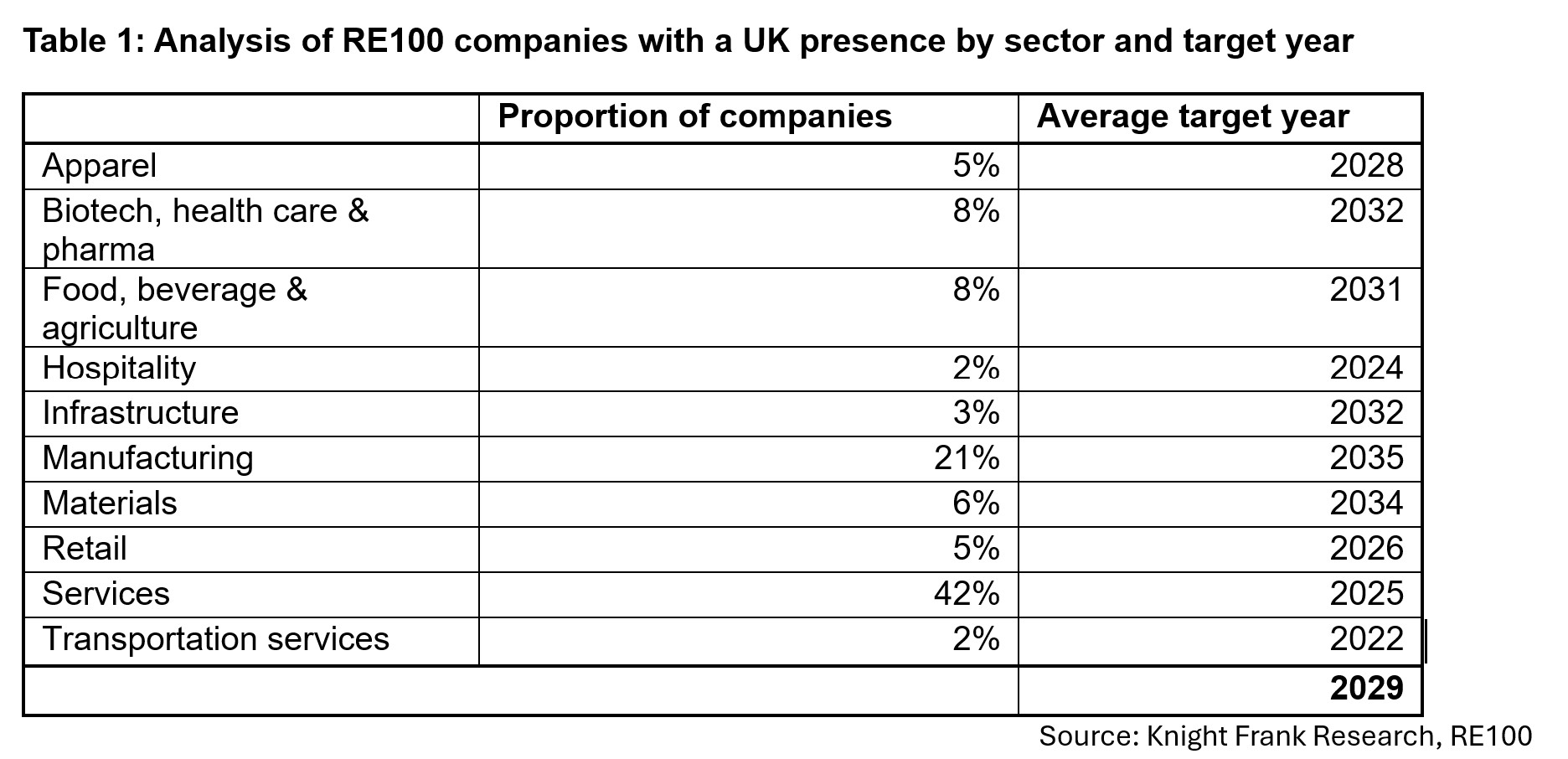

Another measure, with slight overlap, is the 440 members globally that have signed up for RE100, an initiative bringing together businesses committed to using 100% renewable electricity in their operations. While 49 of those are headquartered in the UK, almost 200 have some UK presence. The UK companies pledged to adopt renewable energy faster than global peers, with the average target date of 2026 compared to 2033 across all companies and 2029 for those with a UK presence.

The industry matters with a significant proportion, a third of all global, of those seeking renewable power in the service sectors. Looking specifically at those with a UK presence, 42% are in the services sector and 21% in manufacturing. Those in the service sector have a target date of 2025, this year. Perhaps this is unsurprising given that real estate and power would theoretically be a larger share of emissions, given the nature of the service sector.

Overall, the CPPA market is set to grow as organisations seek long-term price certainty and verifiable low-carbon energy. The crucial defining factor will be the additionality of agreements, the only verifiable alternative where on-site may not be an option.

To discuss CPPA options please contact David Goatman or Charlie Smith.

Note on carbon implications

When procuring renewable energy, carbon accounting is crucial. Under the GHG Protocol Scope 2:

- REGO-backed procurement (meeting all three principles): Zero emissions for market-based reporting; location-based reporting uses UK Government GHG Conversion Factors.

- On-site/private wire: Zero emissions under both GHG Protocol and Net Zero Carbon Building (NZCB) Framework.

- Partially aligned routes: NZCB Framework requires location-based factors.

Sign up to Knight Frank Research.