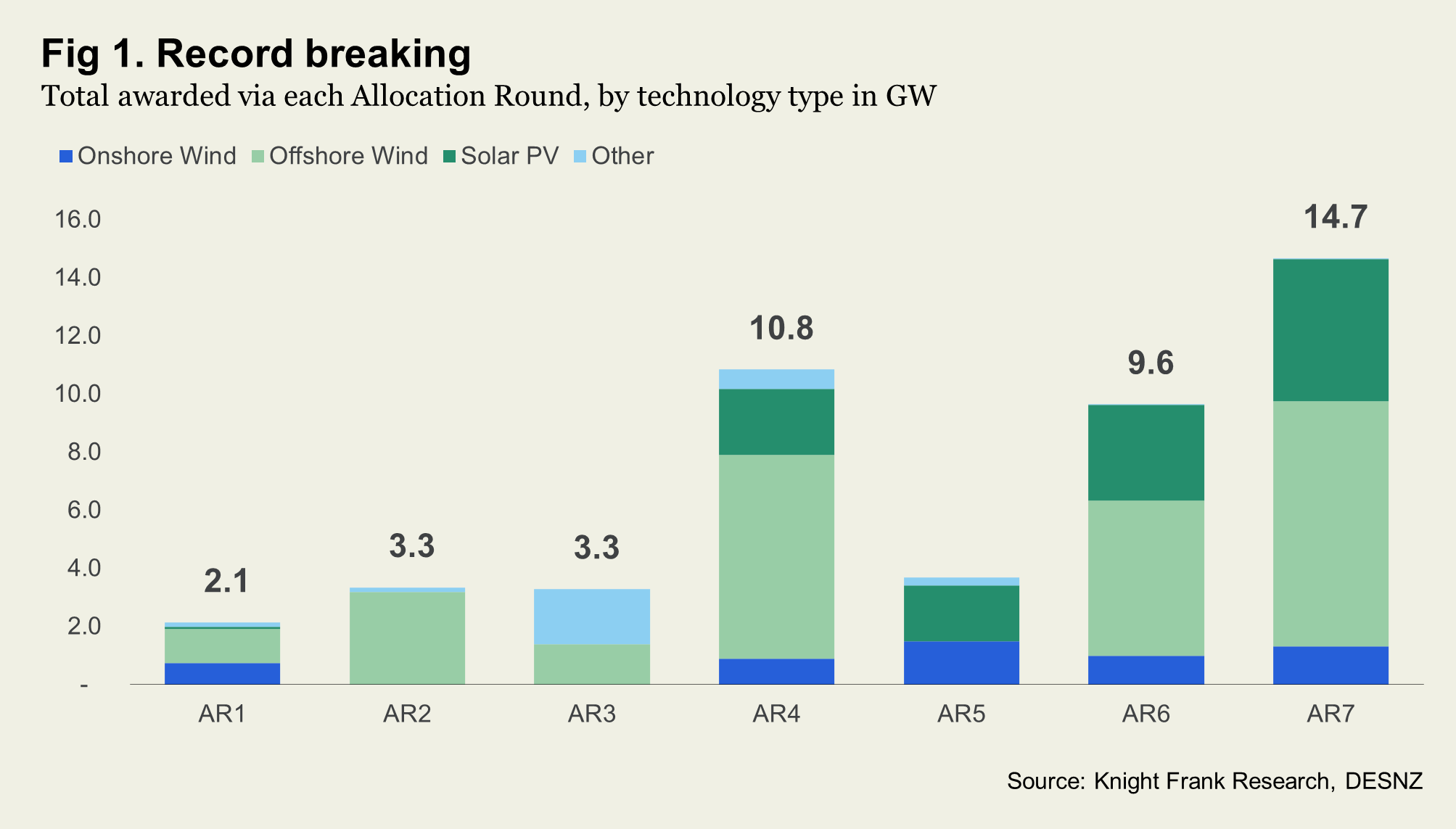

Record Renewable Auctions: Almost 15GW of capacity awarded in AR7

The latest Contracts for Difference auction delivered a record level of capacity, building momentum for UK clean power, here we look tech by tech as well as whether this will be deliverable

23 February 2026

The UK government’s Contracts for Difference (CfD) scheme Allocation Round 7 (AR7) marked a major step-change in the UK’s renewable energy ambitions, awarding a record 14.7 GW of capacity across Offshore Wind, Onshore Wind, Solar and Tidal Stream.

The scale of awards, combined with the shift to 20‑year contract term, demonstrates the government’s determination to accelerate progress towards a predominantly low‑carbon power system by 2030. However, record auction volumes mask persistent structural challenges such as lengthy grid connection queues and prolonged planning timelines which continue to threaten the pace at which these projects can reach operation.

Across all Allocation Rounds and Investment Contracts, excluding Hinckley Point Nuclear, a total of 46 GW has been awarded. AR7 delivered almost one-third of this total with:

• 8.2 GW of Offshore Wind previously announced, adding to

• 4.9 GW Solar;

• 1.3 GW Onshore Wind; and

• 21 MW Tidal Stream.

Sunny days: Solar results

AR7 awarded almost 5 GW of Solar capacity across 157 projects, bringing the cumulative total to more than 12 GW across 378 projects. However, as noted below, 14 projects with a combined 0.4 GW have since been terminated. With 21 GW already installed by Q3 2025, and a government target of 47 GW by 2030, sustained policy support will be essential to keep the UK on track for its low‑carbon electricity goals.

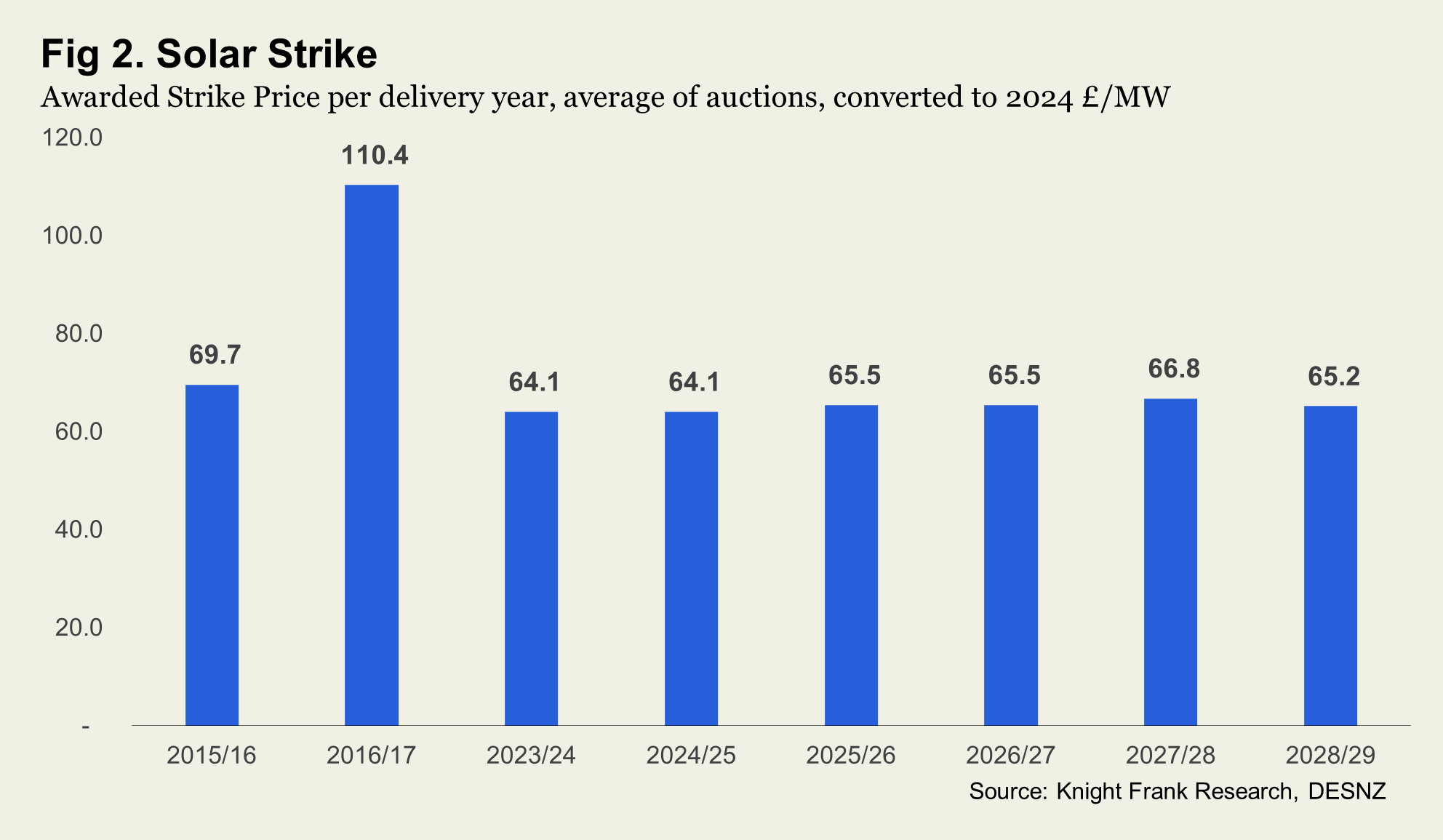

The AR7 Solar Strike Price was £65.23/MWh (2024 prices). While slightly higher than expected, it represents a 13% discount to the Administrative Strike Price (ASP), a narrower gap than the 16% average seen in earlier rounds. Figure 2 shows how Strike Prices, expressed in 2024 terms and averaged where appropriate, evolve across delivery years.

Blowing hot: Wind results

Onshore Wind secured just over 1 GW across 28 projects, taking the cumulative total to 5.3 GW across 99 projects, when accounting for the five terminated projects from previous rounds the total stands 4.9 GW. As of Q3 2025, 16 GW of Onshore Wind capacity was operational, with a government target of 29 GW by 2030.

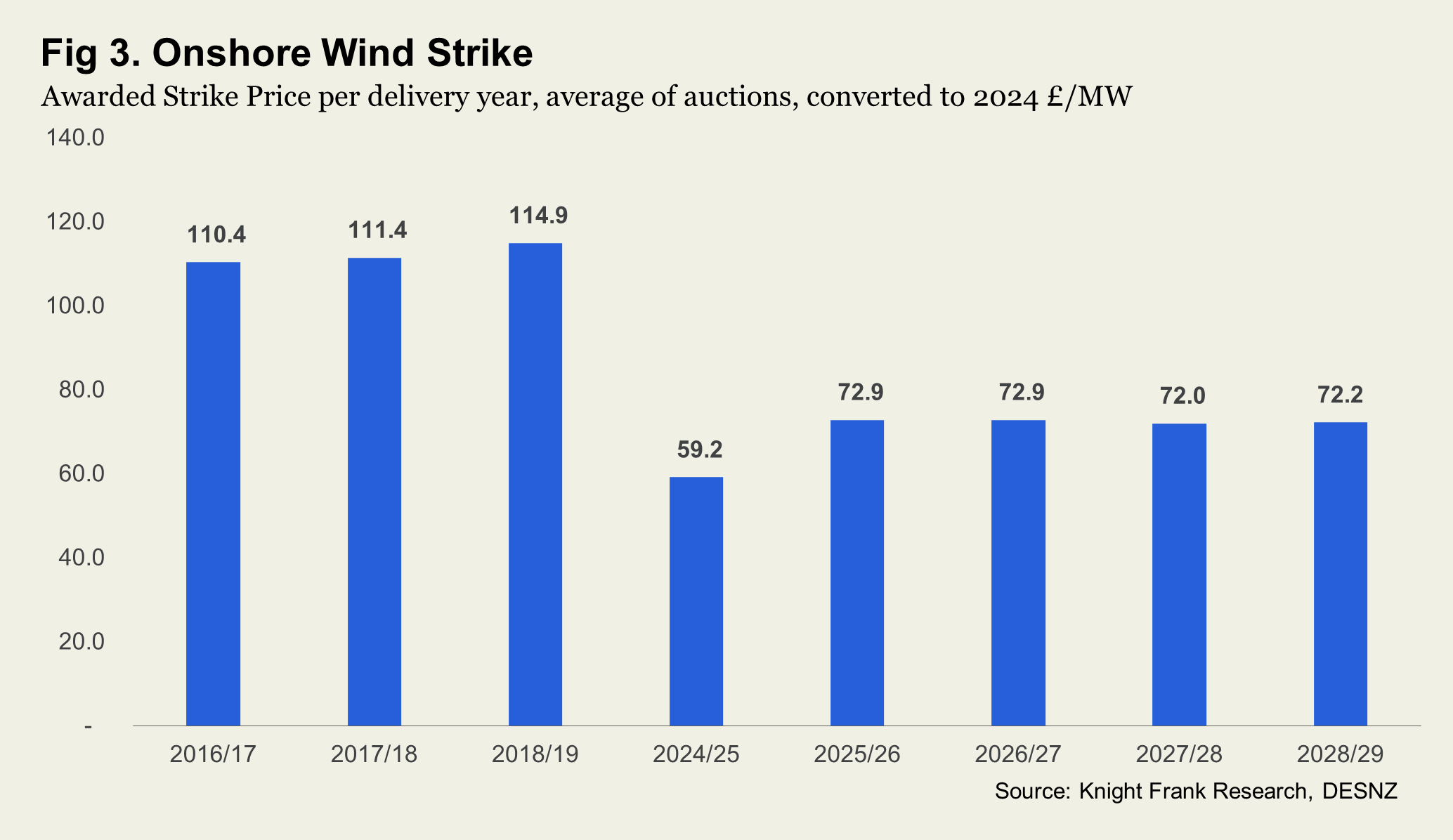

The AR7 Strike Price for Onshore Wind was £72.24/MWh (2024 prices), a 21% discount to the ASP. This is notably deeper than the typical 10% discount of previous rounds, and greater than the discounts achieved in Solar. Figure 3 shows Strike Prices, in 2024 terms and averaged across rounds where necessary, by delivery year.

For Offshore Wind, 8.2 GW awarded in AR7, removing the five terminated projects, brings the total to 27.9 GW across 76 projects, against a government target of 50 GW by 2030. By the end of Q3 2025, 17 GW was already installed. Further detail is available in our separate analysis.

Is this all deliverable?

Not every awarded project will ultimately reach operation. As noted earlier, some contracts have been terminated or left unsigned, while others are facing delays. According to the Low Carbon Contracts Company (LCCC), 13% of contracted capacity has been terminated, 14% is 'Live' either pre-or post-FIC, 44% is categorised as ‘Pre‑MDD’, and 30% as ‘Pre‑Start Date’. Figures that do not yet reflect the latest AR7 awards or Investment Contracts.

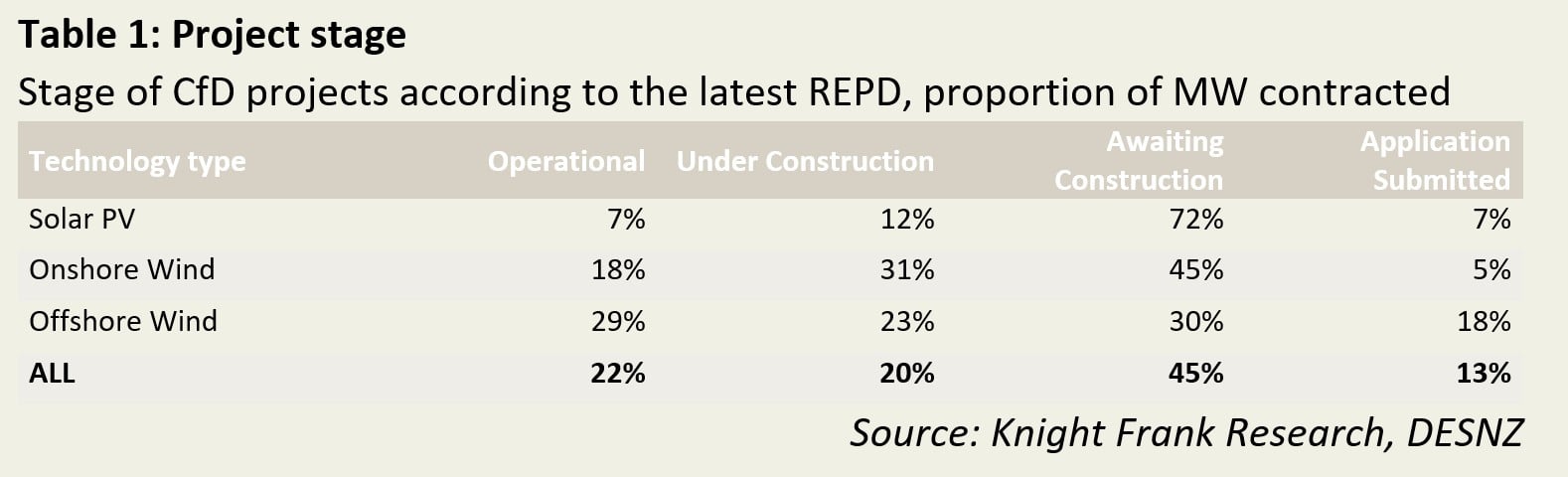

To understand delivery progress in more detail, we matched around 95% of all AR1–AR7 contracts (by capacity) to the Renewable Energy Planning Database (REPD) and found, that by MW awarded:

- 22% is operational;

- 20% is labelled as under construction;

- 45% is awaiting construction; and

- 13% is awaiting planning approvals.

Delivery timelines highlight a mixed picture. Of projects with delivery years up to and including 2024/25, 42% of capacity is operational according to the REPD. Including those under construction increases this to 92%, though the database may not fully reflect real‑time progress.

For context, Nationally Significant Infrastructure Project (NSIP) construction phases average just under two years, suggesting many projects remain some distance from operation. Compounding this, Ofgem recently highlighted ongoing connection delays, even for Gate 2 projects, with 210 projects (representing 62% of all projects qualifying) affected meaning they will have their existing connection date and / or point of connection changed.

Positive momentum but challenges persist

The scale of capacity awarded reflects a strong governmental commitment to reaching 95% low carbon electricity by 2030. However, timely delivery remains a clear challenge. Grid connections, supply chain pressures, and permitting delays all risk slowing progress. Additional measures to accelerate connections and support construction readiness will be essential to realise the full benefits of AR7.

Sign up to Knight Frank Research.