Retail Renaissance: Is the UK retail warehousing market heading towards a supply crisis?

Retail warehousing is at risk of undersupply, with record-low vacancy rates, strong occupier demand and a constrained development pipeline creating growing pressure, particularly in Greater London.

14 July 2026

3 key takeaways

Retail warehousing is in demand

Low (and declining) vacancy rates, robust (and broad-based) occupier demand, and a limited development pipeline – are these market positives or portents?

The development pipeline is limited

2.4m sq ft of retail warehouse floorspace (GIA) is in the development pipeline over an eight year timeframe – far less than the 7.5m sq ft of warehouse space absorbed in 2025 alone.

Undersupply is on the rise

A number of towns and markets are demonstrably undersupplied, especially in Greater London, yet planning and high development costs remain major constraints.

Retail warehouse supply isn't keeping up with demand

Undersupply is something that could already be levelled at the retail warehousing market – and is likely to come increasingly to the fore.

Three forces are conspiring to put pressure on the out-of-town retail property market:

- Limited supply

- Strong occupier demand

- A relatively thin development pipeline

Too much retail floorspace in the UK generally, but not enough of the ‘right’ floorspace, is the great contradictory conundrum facing the retail market. Seemingly a nice problem to have, but actually a headache with no easy cure.

Retail warehouse vacancy rates hit record lows

According to TW Associates, retail warehouse vacancy rates were just 4.8% at the end of 2025, the lowest level on record. On bulky goods parks, the rate is lower still (4.1%), while many parks across the country are at full capacity.

The headline statistics tell one story, the underlying factors another. RWH has not been immune to retail occupier fall-out and there were two major casualties in 2024 in the shape of Homebase (residual 71 stores, ca. 2.5m sq ft of floorspace) and Carpetright (174 stores, ca. 1.7m sq ft of floorspace).

The demise of two large, long-standing occupiers saw a spike in vacancy to 6.4% by the end of 2024. However, the pace at which this space has already been reabsorbed has been phenomenal and serves as proof of the depth of occupier demand for RWH space.

Where is occupier demand coming from?

The occupier base for retail warehousing is larger and more diverse than is often credited.

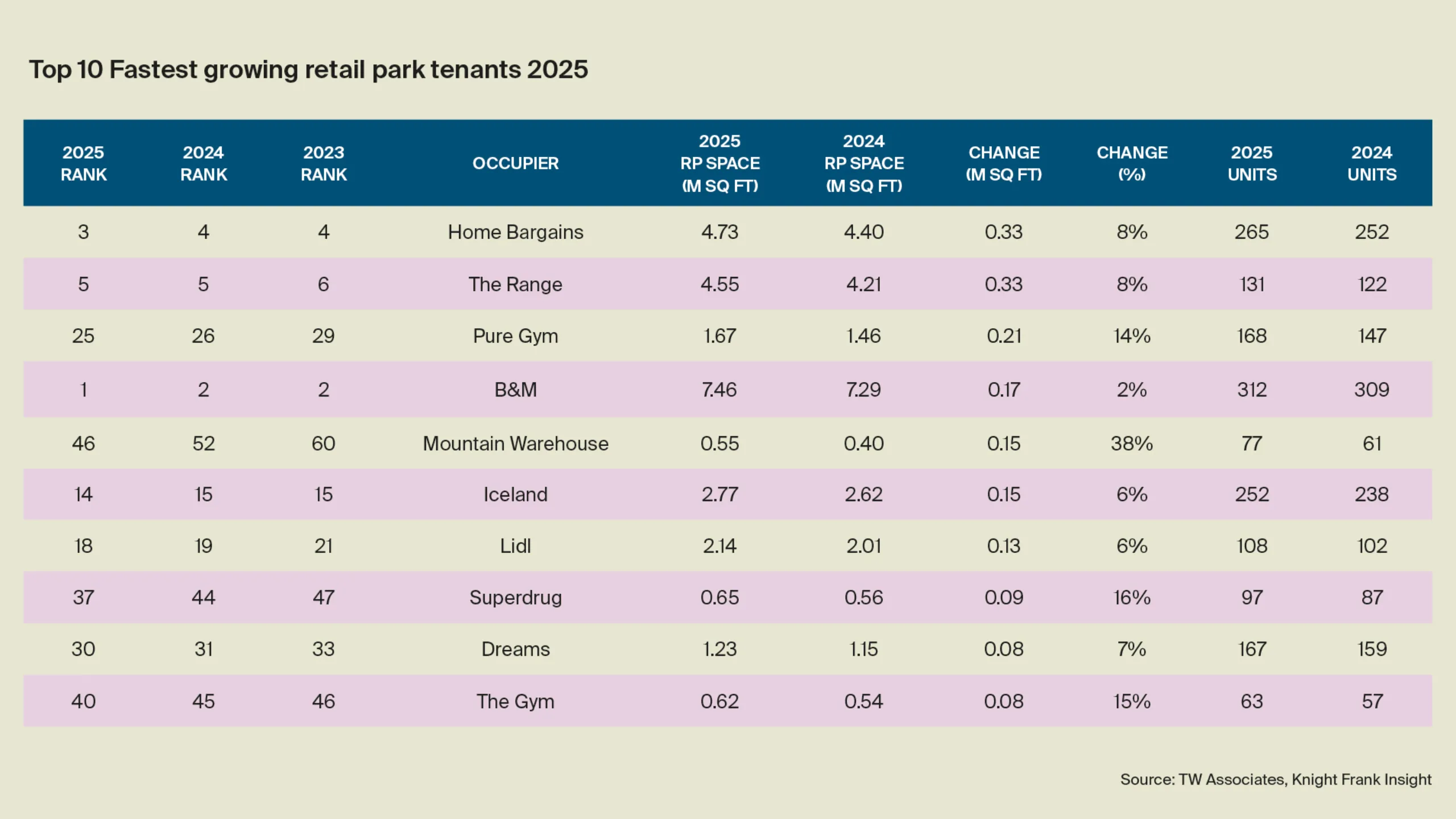

There are over 1,100 RWH tenants, of which 180 occupy more than ten units. And in 2025, these occupiers took on over 5m sq ft of retail park space and 2.5m sq ft of freestanding or solus RWH floorspace.

The ten most acquisitive retail park tenants collectively added more than 1.7m sq ft in 2025, or 3.3m sq ft since 2023. Of the top 50 largest retail park tenants, 29 expanded their RWH footprints last year, ten were broadly flat, while 11 contracted.

As clear an indicator as any of demand outstripping supply and the inevitability of further declines in vacancy rates, but also warning signs of a potential or impending supply crisis.

Greater London's retail warehousing supply struggle

Supply metrics vary by location and we're able to calculate provision relative to the size of the market it serves. This analysis supports a market reality – Greater London as a collective whole is severely undersupplied in RWH floorspace.

And what floorspace it does have is under pressure from other uses, particularly residential – the capital being one of the few locations nationally where values stack up sufficiently to warrant repurposing.

This imbalance is unlikely to tip towards retail warehousing going forward. Retail parks are acknowledged in the latest iteration of a ‘Towards a New London Plan’ report, although largely in a negative context that undervalues the role they play in London’s wider infrastructure.

A constrained retail development pipeline

The current development pipeline isn't enough to counter the risk of undersupply. TW Associates lists just 21 schemes likely to proceed before 2033.

14 of the 21 schemes are sub 100k sq ft gross internal area (GIA). Collectively, all 21 schemes cover 2.7m sq ft, if they're all delivered to current spec and plan. Which is a big ‘if’. And even if they do come to fruition as planned, they will be delivered over an eight year timeframe (2025 – 2033).

This is less space than was absorbed last year alone on retail parks (ca. 5m sq ft) and far less for all retail warehousing (ca. 7.5m sq ft). And none in Greater London, where supply is at its most scarce.

What does this mean for the retail warehousing market?

There is strong occupier demand, declining vacancy rates, impetus for rental growth, and sustained improvement across all retail warehousing real estate metrics.

But there will come a point where lack of supply becomes an issue, both for acquiring tenants looking for sites and for landlords looking to optimise their line-ups and retail mixes. We're neither predicting nor advocating a return to mass retail warehousing development.

Development may only be financially viable in certain geographies and even where the numbers do stack up, planning must also align.

Potential undersupply in an otherwise oversupplied retail market – a contradiction, but a retail warehousing market reality. If we're sleepwalking towards a supply crisis, this should be the wake-up call.

Sign up to Knight Frank Research