From Ecommerce to Reindustrialisation: Europe’s Next Logistics Cycle

22 June 2026

Key Insights

-

The next phase of the cycle will be more selective

Performance will increasingly be defined by location, connectivity and asset quality, with modern, energy-efficient assets in supply-constrained and infrastructure-rich corridors best positioned to capture outsized rental growth and investor demand. -

Ecommerce remains a core structural demand driver

Online penetration is forecast to rise from 17.1% in 2022 to over 24% by 2032 (Oxford Economics), underpinning sustained demand for modern, automation-ready logistics space. -

Urban logistics demand is strengthening, driven by intensifying competition in same- and next-day delivery

Competition in same- and next-day delivery is accelerating the need for localised inventory and last-mile networks, particularly in major metropolitan areas, reinforcing demand for infill and population-adjacent assets. -

Expansion of major ecommerce operators is reinforcing occupier demand

The rapid scaling of Asian ecommerce operators alongside Amazon’s vertically integrated logistics offering is driving competition for space, supporting greater depth and liquidity in occupier markets. -

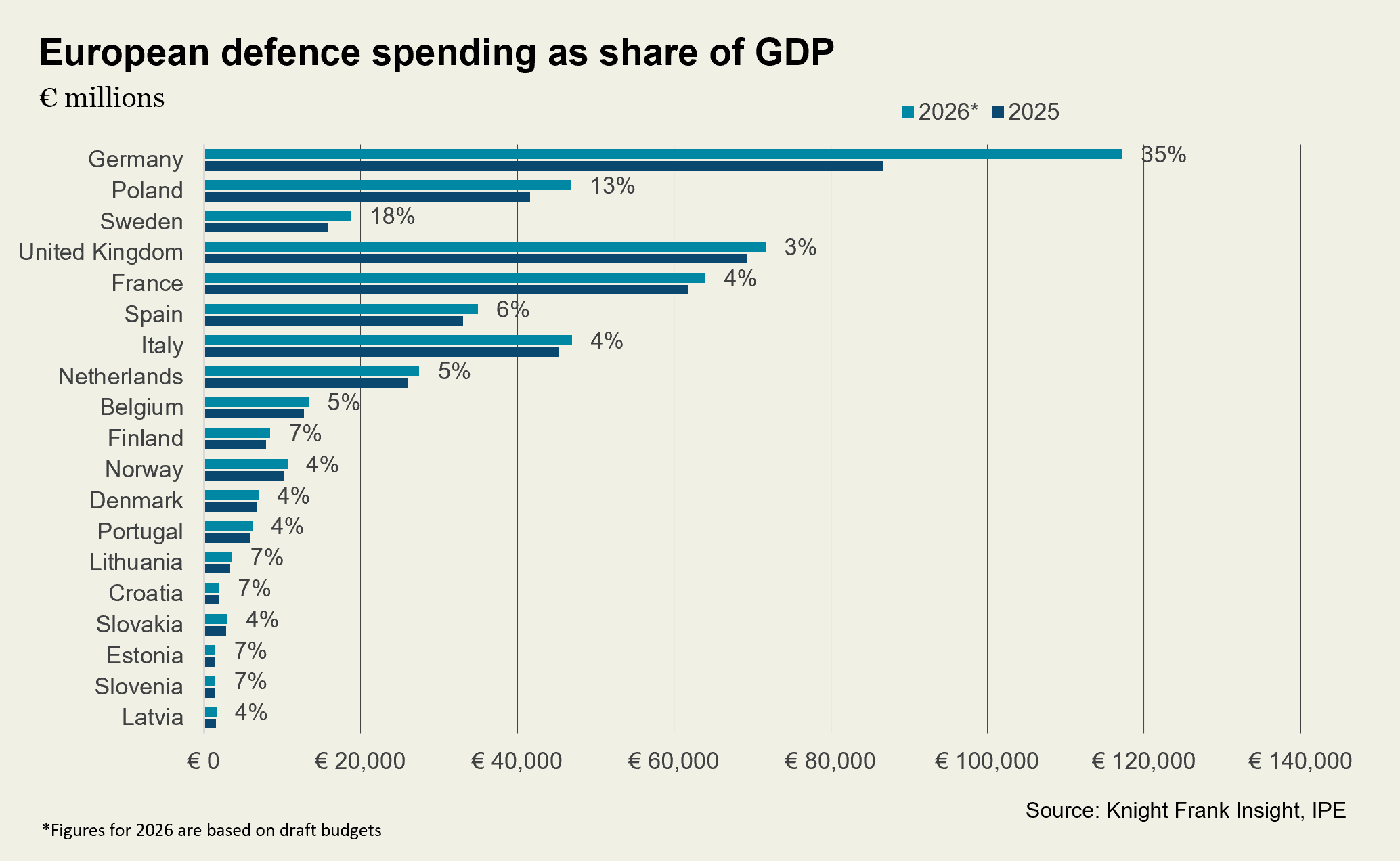

Defence spending is emerging as a selective demand driver

Rising military investment is supporting targeted demand in established manufacturing clusters (notably Germany, southern France and the West of England), with the primary impact likely to be indirect, via supply chain activity. -

Nearshoring is driving a structural reconfiguration of industrial demand

Manufacturing footprints are shifting closer to end markets (onshore rising to 48% of production from 41% over the next three years), with Central and Eastern Europe set to benefit due to structural labour and energy cost advantages.

A more selective growth cycle ahead

The investment case for European industrial and logistics real estate remains compelling, supported by a combination of structural demand drivers. Continued ecommerce expansion, rising defence spending and the reconfiguration of global supply chains are all contributing to a sustained increase in occupier demand.

However, the next phase of the cycle will be more selective. Growth is increasingly concentrated in specific locations, asset types and sectors, with performance driven by the ability to align with evolving occupier requirements. Markets that combine strong fundamentals, infrastructure investment and proximity to demand are likely to outperform, while asset quality will play an increasingly important role in shaping outcomes.

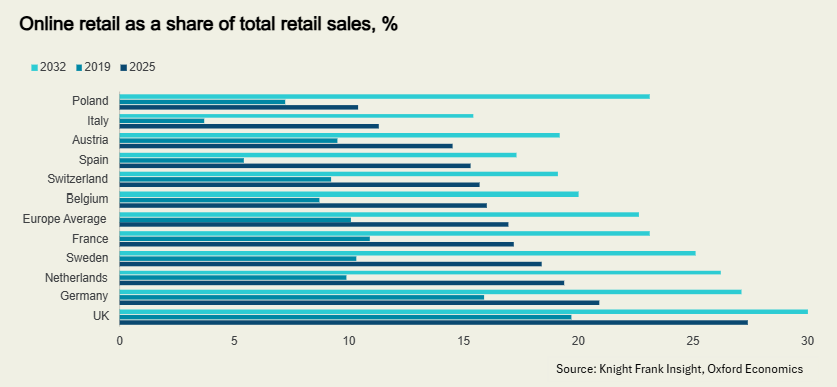

Ecommerce expansion set to continue

Europe’s ecommerce growth story still has further to run, but the next phase will be more selective. Oxford Economics forecasts online penetration to rise from 17.1% of retail sales in 2022 to more than 24% by 2032, with online sales continuing to grow at more than twice the pace of store-based retail. This should remain supportive of logistics demand, particularly as retailers and third-party logistics providers underpin take-up and occupiers prioritise modern, automation-ready Grade A space.

The market is not only expanding, but also becoming more competitive. Chinese platforms are an increasingly prominent force, not only through rising parcel volumes but also through sustained investment in European distribution networks. JD.com’s launch of its Joybuy platform across six European markets in March 2026, offering same-day delivery to over 15 million households, highlights this shift. Its “double 11” delivery pledge, whereby orders placed before 11 a.m. arrive by 11 p.m. the same day in cities such as London, Paris and Berlin, reinforces the growing importance of speed and reliability in fulfilment. As competition in same- and next-day delivery accelerates, this is driving a greater need for localised stockholding and fulfilment, strengthening demand for dense, local logistics networks.

This is already translating into demand for space. Jingdong Logistics has taken 41,180 sq m at Verdion PremierPark in Ludwigsfelde, Germany, while Shein continues to expand its footprint, including a major hub near Wrocław. Chinese online retailers are also extending their reach into Europe via third-party logistics networks. Cirro Fulfillment has recently leased 27,720 sq m at Alcalá Logistics Park in Madrid, while Cainiao has taken a 26,000 sq m facility in Rotterdam, its second in the Netherlands, and has also secured facilities in Paris, Madrid and Rokitino, Poland as it expands its European footprint.

At the same time, business models are evolving. Joybuy is transitioning towards a marketplace platform, opening to selected third-party sellers from both Europe and China while expanding its geographic reach. This brings it closer to Amazon’s operating model, intensifying competition in an already crowded market that includes Temu, Shein, TikTok Shop, AliExpress, Zalando and a range of national retailers. Meanwhile, Amazon has launched its Supply Chain Services offering, effectively providing a third-party logistics solution supported by its global infrastructure and technology platform.

Together, continued ecommerce expansion and intensifying competition in same- and next-day delivery support the case for the sector over the next five to ten years, particularly in markets where online penetration still has headroom and local enablers are improving. Over the next five to seven years, growth is expected to be strongest in markets such as Poland, Sweden and Spain, underpinned by rising incomes, increasing mobile commerce adoption and improving logistics infrastructure. Larger markets such as Germany and the Netherlands also retain significant upside given their scale. The result is a more competitive and increasingly localised European ecommerce market, but one that continues to point to a clear opportunity for logistics real estate.

Defence manufacturing: a selective driver of demand

Rising defence budgets are beginning to shape a new, if uneven, source of demand for European industrial real estate. Spending is increasing across the region, with notable growth in Germany, Sweden and Poland. This is likely to translate into occupier demand in established manufacturing hubs, particularly across Bavaria and western Germany, southern France and the West of England, where existing industrial ecosystems can support expansion.

The opportunity, however, is highly concentrated. Germany stands out, supported by a €100 billion special fund and reforms enabling sustained increases in military investment. Munich is becoming an increasingly important hub, with Bavaria actively developing a civil-military innovation ecosystem, including new facilities in Erding backed by significant state funding.

Southern France represents another core cluster, anchored by major production, assembly and testing facilities across naval systems, combat aircraft, helicopters and guided missiles, alongside access to Europe’s largest naval base. In the UK, the West of England, particularly around Bristol and the Port of Avonmouth, is well positioned given the presence of major defence contractors including BAE Systems, Rolls-Royce, MBDA and Babcock. In contrast, countries without a significant domestic manufacturing base are likely to rely on procurement from allies, limiting direct real estate impact.

For investors, tapping into this structural tailwind of demand can be challenging. Much of defence manufacturing is concentrated in secure, owner-occupied facilities tied to government contracts. However, demand is likely to emerge indirectly through the supply chain, with increased activity among second- and third-tier suppliers supporting take-up in more conventional industrial assets. As such, the opportunity is less about primary facilities and more about the broader ecosystem of engineering, manufacturing and logistics space that underpins them.

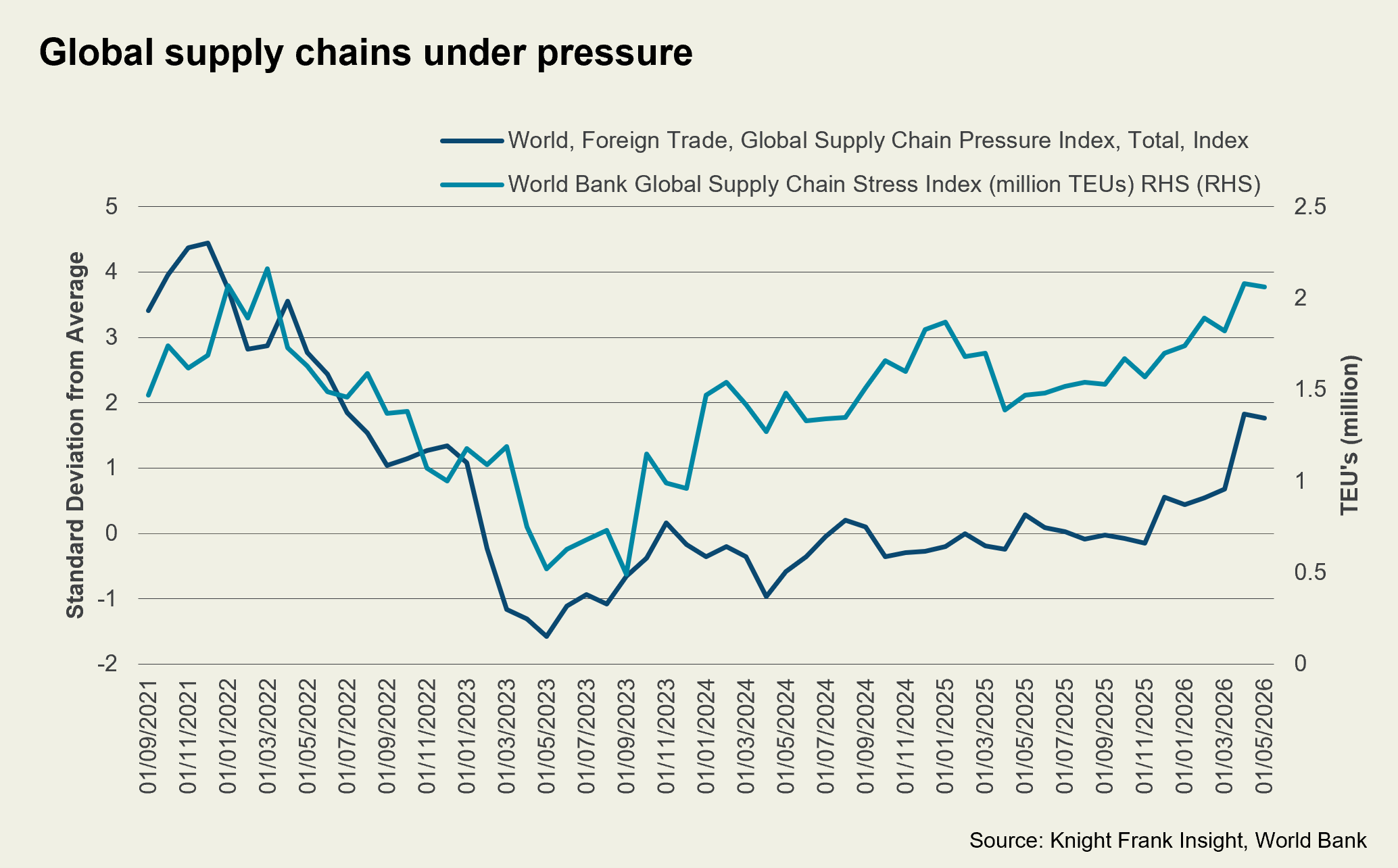

Supply chain disruptions reinforce the case for nearshoring/onshoring

Global supply chains remain under pressure, with recent disruption levels approaching those seen during the pandemic. Shipping capacity tied up in delays and reroutings reached around 2.06 million TEUs in May 2026, close to the 2022 peak, reflecting ongoing geopolitical tensions and operational constraints across key trade corridors. This persistent volatility is reinforcing a shift in corporate strategy towards resilience, with clear implications for industrial demand.

As a result, supply chains are being structurally reconfigured. Companies are holding more inventory, diversifying sourcing strategies and adopting more complex, multi-node networks. At the same time, production is increasingly being positioned closer to end markets to improve responsiveness and reduce exposure to disruption.

Nearshoring is central to this ongoing transition. Capgemini data suggests onshore manufacturing will rise to 48% (from 41%) and nearshore to 24% (from 22%), while offshore declines to 28% (from 37%) over the next three years. Alongside this, firms are continuing to reduce reliance on China through “China plus one” strategies, duplicating or relocating production closer to European markets.

This is already visible in occupier behaviour. Siemens has moved elements of production from Asia to Eastern Europe to reduce lead times, while Bosch has expanded manufacturing across Hungary and the wider region. In the automotive sector, OEMs including BMW, Volkswagen and Stellantis are encouraging suppliers to replace China-based inputs, accelerating supply chain localisation. Intra-European nearshoring is also evident, with Miele relocating production from Germany to Poland and Michelin rebalancing operations from the UK to Romania and Poland. At the same time, non-European capital is targeting the region, illustrated by EVE Energy’s c.€1 billion battery plant investment in Debrecen.

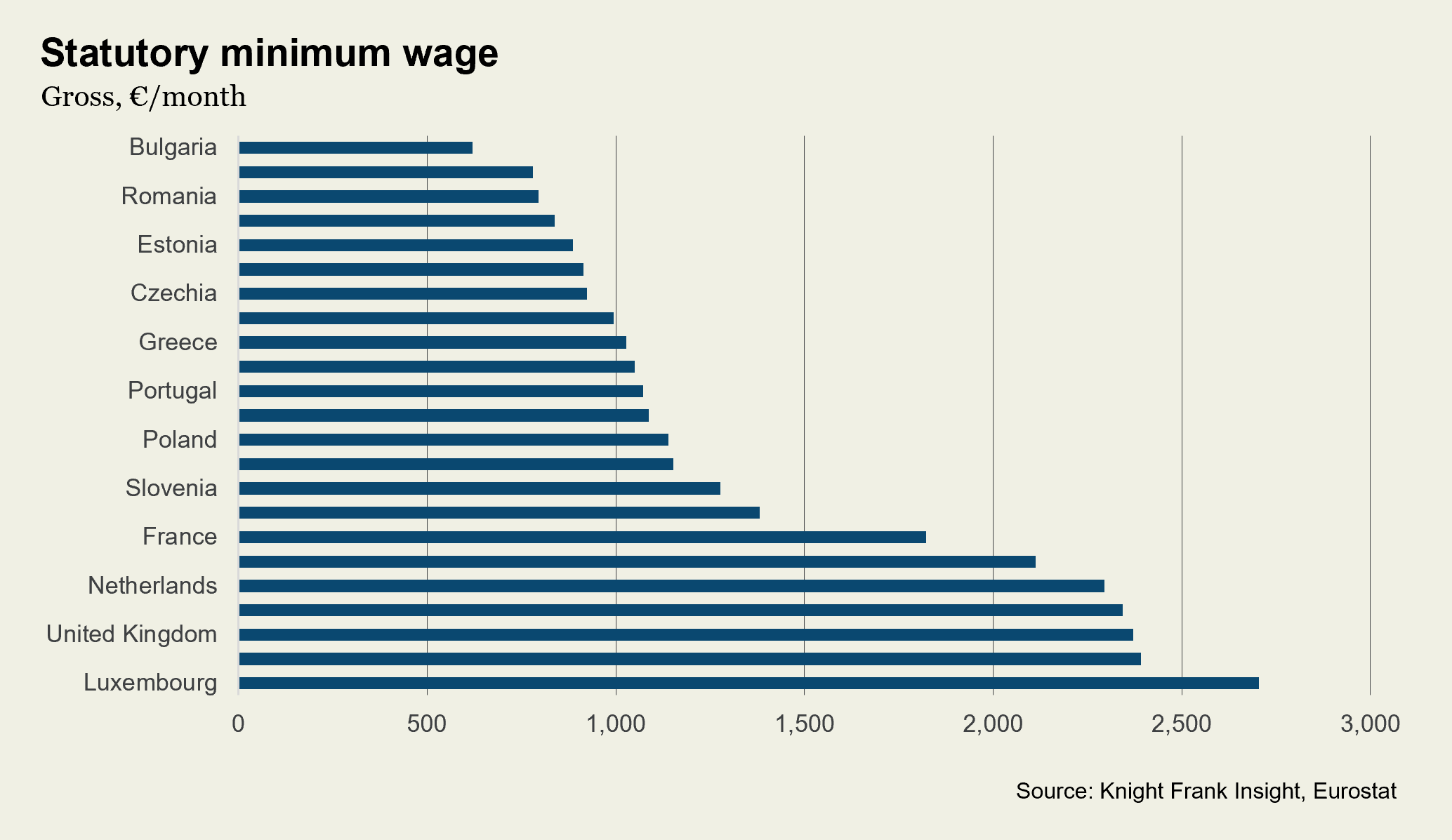

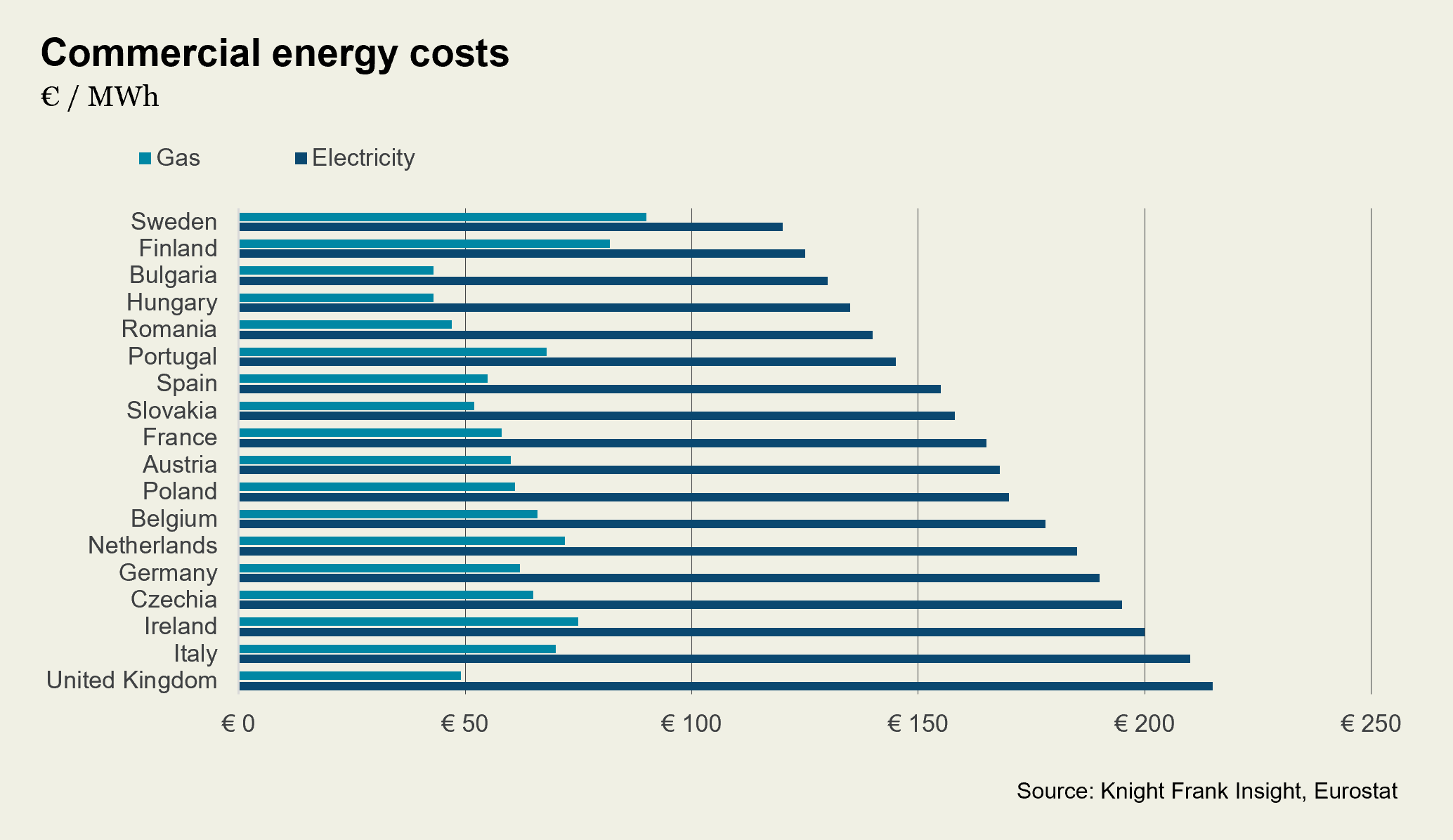

Cost arbitrage remains a key driver determining location for production. The charts highlight a clear differential in both energy and labour costs across Europe. Electricity prices in core Western European markets such as the UK, Germany and Italy typically range between €180–€220/MWh, compared with €120–€150/MWh across much of Central and Eastern Europe. A similar pattern is evident in labour costs, with minimum wages in markets such as Bulgaria, Romania and Hungary typically below €1,000 per month, versus more than €2,000 in markets including Germany, the Netherlands and the UK.

This differential continues to underpin location decisions, particularly for manufacturers seeking to balance resilience with operating efficiency. As a result, Central and Eastern Europe remains the primary beneficiary. Markets such as Poland, the Czech Republic and Hungary combine structural cost advantages with improving infrastructure and strong integration into Western European supply chains, with Poland standing out given its dual role as both a manufacturing base and a large consumer market.

Elsewhere, the Western Balkans represent a second, earlier-stage opportunity, offering lower production costs and favourable transit times to Western European markets, while Spain is gaining relevance, emerging as a beneficiary of both demographic growth and improving logistics infrastructure. Core Western European markets, notably Germany and the Netherlands, continue to anchor distribution networks, with key corridors such as the Benelux–Germany axis benefiting from increased inventory localisation, which is supporting rental growth, particularly around key port and airport hubs.

Despite these strong structural tailwinds, risks are becoming more pronounced. Transport and energy prices remain volatile, and power availability is becoming an increasingly important constraint, particularly as automation intensifies. These pressures are likely to accelerate the polarisation of the market, with demand focusing on modern, energy-efficient assets while older stock faces a growing risk of obsolescence.

Sign up to Knight Frank Research.