Property Market Under Pressure as Bond Market Clash Looms

Higher borrowing costs, driven by a spike in energy prices and concerns around the policy agenda of a new government, are feeding through to mortgages and could cool demand in the housing market further.

14 May 2026

A showdown between a soft-left Labour government and the bond market is brewing.

Prime Minister Keir Starmer has avoided any confrontation since his party won the general election in July 2024 by taking a technocratic and centrist approach.

But one outcome of a Labour leadership contest is a government to the political left of the current administration, a prospect that is unnerving the investors that lend the government money.

The ten-year yield on UK government debt has been trading above 5% for most of this week, which is the highest it has been since the global financial crisis in 2008.

This is partly due to inflation concerns linked to the Middle East conflict. Energy price shocks leave the UK particularly exposed to higher inflation.

But the recent spike in borrowing costs also reflects the growing likelihood of a new government, in particular concerns around its spending agenda, borrowing plans and any associated inflationary impact. The ten-year yield on US government debt has also climbed since the Iran war began but, for comparison, is trading below 4.5%.

The key issue for the property market is what a new Chancellor would mean for inflation. Handing out further public sector pay awards, for example, would be seen as driving it higher.

Higher inflation expectations mean higher swap rates, which is the instrument lenders use to price fixed-rate mortgages. If borrowing costs continue to rise, it will dampen prices and, to a lesser extent, transaction volumes. It’s a calculation that buyers and sellers face if they are deciding whether to act now or this autumn.

Hard-Headed Reality

We have seen the gap between political ideology and the hard-headed reality of debt markets this week.

Paula Barker, an MP backing Andy Burnham for the Labour leadership, said that “markets will have to fall in line.” It follows previous comments by Burnham that the government had to “get beyond this thing of being in hock to the bond market.”

“Team Burnham really need to circulate some lines to stop this nonsense from supporters,” said James Nation on X, a former special advisor to Rishi Sunak at the Treasury.

Barker’s statement is the equivalent of a homeowner asking their mortgage lender to fall in line.

The prospect of political upheaval, looser fiscal discipline and higher inflation was a “toxic mix” for financial markets, said Pepperstone analyst Michael Brown.

“The simple way to avoid being ‘in hock’ to bond markets is to further consolidate the overall fiscal position, cutting public spending and demonstrating a degree of fiscal restraint, while also implementing growth-friendly policies such as tax cuts (in due course), and investment incentives,” he said.

“The UK will never struggle to sell its debt, or refinance obligations that are coming due. The issue is what yield investors demand in return.”

Weaker Demand

Meanwhile, we saw another example this week of how demand in the housing market is getting weaker.

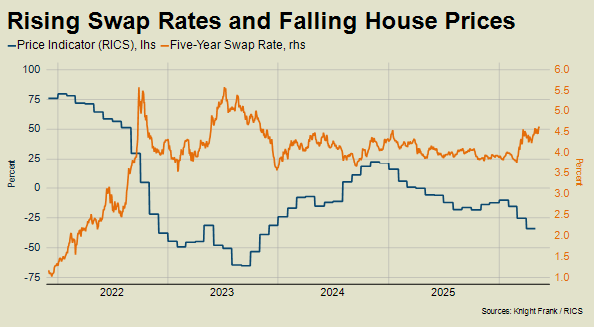

The latest RICS UK Residential Market Survey concluded that “muted conditions are likely to persist over the coming months”. A net balance of -34% of respondents said house prices were falling, which is the most pessimistic outlook since November 2023, when buyers and sellers were still recovering from a period of double-digit inflation – see chart below.

For now, demand is being supported to some extent by buyers with mortgage offers that predate the conflict, but downwards pressure on prices will increase as those offers lapse in coming months. This may explain the mixed signals being sent by the latest Halifax and Nationwide house price data.

We recently downgraded our house price forecasts for all UK markets as a result of the jump in borrowing costs but also the prospect of another tax-raising Budget as the government grapples with the economic fallout from the conflict in the Gulf.

Uncertainty surrounds not only what the Chancellor might say this autumn but also their identity.

Could their plans include scrapping stamp duty? That was one proposal in a policy pamphlet issued by the soft-left Tribune Group this week, which proposes replacing it with a land value tax.

It’s very unlikely, but the merits of taxing the property rather than the transaction are being noted across the political spectrum. The Conservative Party have also pledged to scrap stamp duty, presumably on a carefully choreographed timeline that will avoid freezing the housing market.

Any Chancellor would also face the challenge of a short-term drop in tax revenue.

“I’m skeptical about a full scale move to a land value tax,” said James Nation. “It would take years to introduce, and the Labour Party will only have two ahead of the next General Election. Plus, in the near term, they need additional revenue to top up public spending”.

Sign up to Knight Frank Research.