Labour’s local election reckoning

Making sense of the latest trends in property and economics from around the globe

08 May 2026

Long-term government borrowing costs hit a 28-year high earlier this week on concerns that Prime Minister Keir Starmer will face a leadership challenge should Labour fare poorly in this week's local elections. So far, Starmer's worst-case scenario is playing out.

At the time of writing, Labour is on track for record losses. Reform is the main beneficiary, but as the Times's Patrick Maguire writes: the party "is losing to everyone, everywhere."

"At best, Labour MPs are being taught a hard lesson about the fantastical unpopularity of their leader," he adds. "At worst, they are witnessing — and frankly are complicit in — Labour’s demise as a national party."

Investors are concerned that any incoming leader would be less disciplined with the public purse. The yield on the 30-year government bond climbed to 5.77% on Tuesday, its highest level since 1998. It had eased back to 5.63% as of yesterday. Long-term government borrowing costs feed into mortgage pricing and development finance.

Political volatility

UK house prices dipped 0.1% in April, pegging the annual growth rate at 0.4%, Halifax reported this morning. That's another show of resilience given recent increases in mortgage rates and the knock to consumer sentiment from the conflict in the Middle East.

The outlook for borrowing costs is particularly uncertain given the UK's domestic political volatility and the day-to-day swings in US policy on Iran. The latter appears to be inching towards a resolution, but we've been here before.

A reminder: last month we updated our forecasts for house prices and rents. We expect UK house price growth of 1.5% this year, followed by 3% next year and 4% in 2028. That compares with our September expectation that prices would grow by 3% in 2026 and 4% the following year.

Prices in prime central London are forecast to drop by 2% this year, compared with our September expectation that they would be flat. Similarly, we think prices in prime outer London will be flat in 2026, down from our previous forecast of 2% growth.

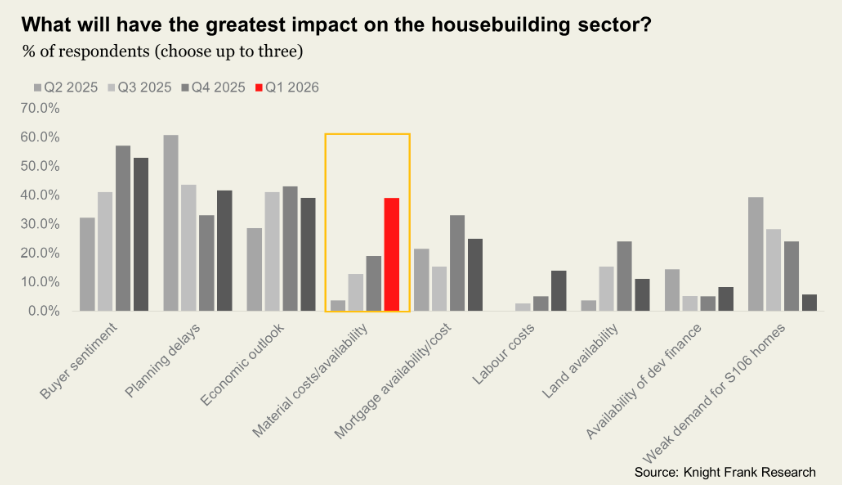

A material impact

The cost and availability of key materials moved sharply up the agenda in our survey of volume and SME housebuilders, published last week. Almost 40% of respondents cited materials costs and availability as a key factor likely to affect the sector over the next quarter, up from less than 20% previously (see chart).

It's taken a few weeks, but the disruption in the Strait of Hormuz is now having a material impact on build costs. Around 69% of the respondents to the latest S&P Global Construction PMI reported a rise in their input costs in April, up from 48% in March. That points to the fastest overall rate of cost inflation since June 2022 or, if you set aside the pandemic, the fastest rate in three decades of data collection. Many firms noted that suppliers were passing through higher transportation costs, while subcontractors increased their average prices charged by the most in three years.

Another survey from The Royal Institution of Chartered Surveyors showed that construction activity shrank during Q1 2026 at the fastest rate since Q2 2020, when sites were closed during the Covid-19 lockdown.

"Rising material costs, a tougher credit environment and increased pressure on margins are already leading some developers to slow construction activity," said RICS Chief Economist Simon Rubinsohn.

The increase in energy prices will be felt hardest for materials that are energy intensive to produce, such as bricks, concrete, cement and aluminium.

A cautious outlook

Conditions for UK residential developers were relatively stable at the turn of the year. Land values held steady in the final quarter of 2025 and mortgage rates eased through the early weeks of 2026, reinforcing a prevailing view that the market was close to its bottom. In London, sentiment also benefited from confirmation of policy measures designed to improve development viability.

That optimism proved short-lived, of course. Urban brownfield and prime central London residential development land values declined in Q1 2026 as geopolitical instability, higher borrowing costs and an easing, yet still challenging, planning and regulatory environment weighed on demand, according to our Residential Development Land Index. Both fell by 2.5%, leaving annual declines at 1.1% for prime central London and 2% for urban brownfield land.

Greenfield land values remained flat, reflecting more resilient conditions for volume housebuilders in suburban markets, where lower-density schemes, simpler build requirements and steadier underlying demand have supported viability relative to higher-risk urban developments. Values dipped 0.7% on an annual basis.

Trading updates from listed housebuilders continue to point to a cautious outlook. Several have revised down volume expectations and land acquisition targets, citing global uncertainty and slower sales rates. Many are focusing on existing pipelines rather than expanding landbanks, which will reduce competition in the market for those who are still active.

There are, nevertheless, pockets of resilience. Even in the absence of demand-side support, sales early in the year held up, supported in some cases by demand from build to rent operators and partnership models. Near-term performance, however, remains sensitive to changes in buyer sentiment and mortgage market volatility.

In other news...

IMF warns new AI models risk ‘systemic’ shock to finance (FT), Billionaire Duke of Westminster to Sell £700 Million of US Real Estate Assets (Bloomberg), Persimmon Sticks to Guidance, Joins Chorus Warning on Costs (Bloomberg), Graduate jobs fall by a third as more employers embrace AI (Times), and finally, UK retail space shrinks ‘for the first time since the 1940s’ (Times).

Sign up to Knight Frank Research.