From calm conditions to renewed uncertainty

Land values ease, pockets of resilience for new build demand, but near term outlook cloudy

30 April 2026

Market conditions were relatively stable at the turn of the year. Land values held steady in the final quarter of 2025 and mortgage rates eased through the early weeks of 2026, reinforcing a prevailing view that the market was close to its bottom. In London, sentiment also benefited from confirmation of policy measures designed to improve development viability.

That optimism proved short-lived.

The outbreak of conflict in the Middle East at the end of February marked a swift return to uncertainty. Mortgage rates spiked, consumer confidence weakened and the risk of higher build and materials costs moved back into focus.

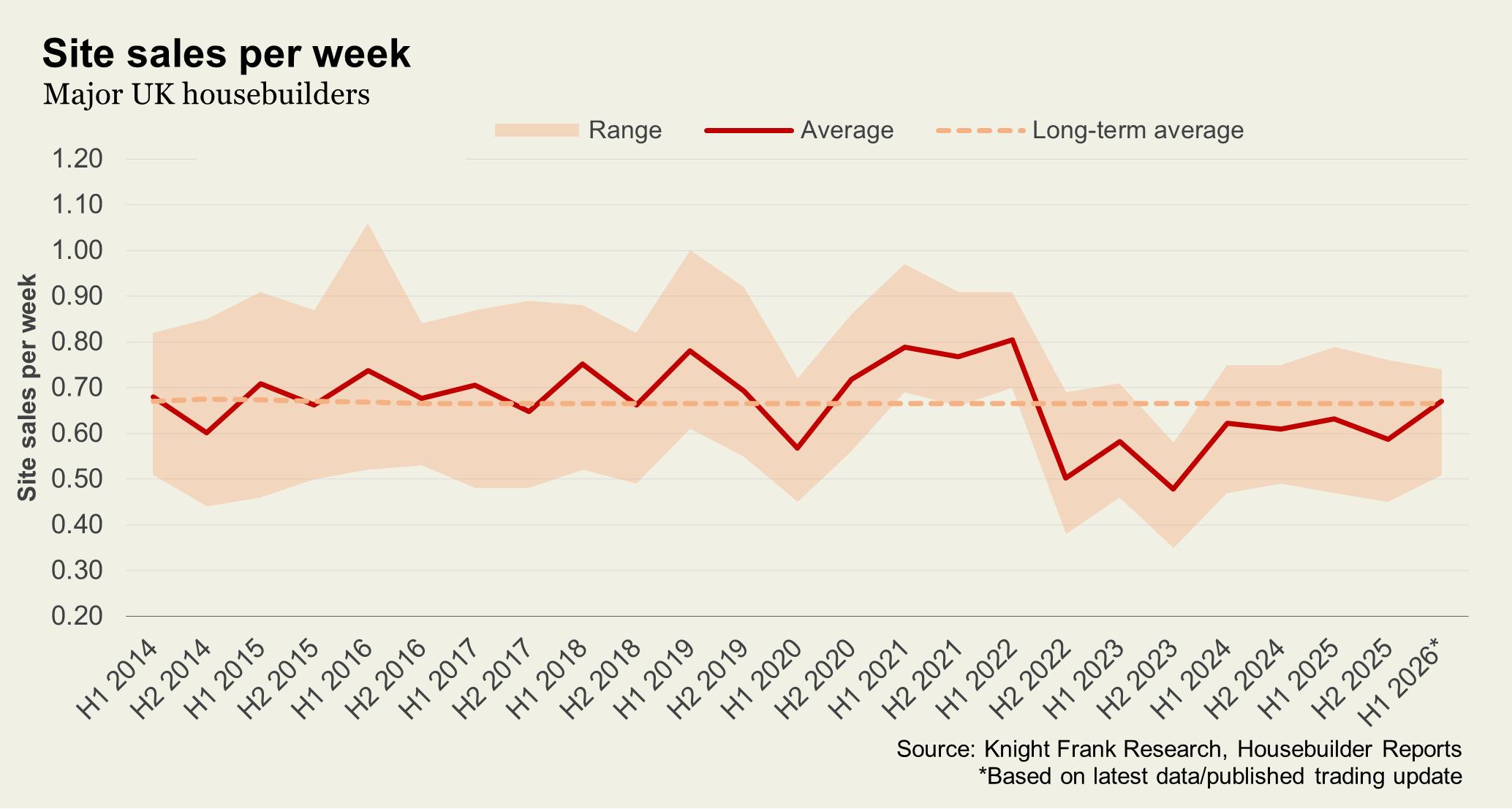

Against this backdrop, developers remain cautious. Demand continues to focus on “oven ready” sites with full planning consent, where schemes can move quickly and limit exposure to planning or regulatory delay. Supply of such opportunities remains constrained, however, contributing to subdued transaction volumes.

This has, in turn, put pressure on land values which softened across most segments in the first quarter. Urban brownfield and prime central London development land both recorded quarterly falls of 2.5%. Greenfield land values were more resilient, remaining flat over the quarter and down 0.7% year-on-year, reflecting comparatively stronger conditions for volume housebuilders in suburban markets.

Balance sheet takes priority

Trading updates from listed housebuilders continue to point to a cautious outlook. Several have revised down volume expectations and land acquisition targets, citing global uncertainty and slower sales rates. Many are focusing on existing pipelines rather than expanding landbanks, which will reduce competition in the market for those who are still active.

There are, nevertheless, pockets of resilience. Even in the absence of demand-side support, sales early in the year held up, supported in some cases by demand from build to rent operators and partnership models. Near-term performance, however, remains sensitive to changes in buyer sentiment and mortgage market volatility.

Costs and confidence shape the outlook

Mortgage rates eased through April following signs that a deal could be reached to reopen the Strait of Hormuz, with leading fixed rates falling back to just over 4.5%, well below the 5%+ deals seen at the height of the crisis, but still above the more abundant sub-4% rates available earlier in the year.

It might suggest that a turnaround could begin swiftly on the back of more positive news, but a return to conditions that prevailed before the conflict will likely take months. Sentiment will recover gradually and mortgage rates should begin easing again, but only to a point. Oil prices are still well above the $70 pre-war level and are unlikely to recede to that level in the short term, which will prevent inflation from declining to levels forecast before the conflict.

Near-term indicators point to continued caution. Just 8% of our survey respondents said they expect reservation volumes to improve over 2026, while 44% anticipate further weakening and the same proportion expect no change. Nearly half expect start volumes to decline over the next three months.

This caution extends to land values. Close to half of respondents expect prices to fall again next quarter, with minimal expectation of any upward movement. Developers remain highly price-sensitive, with appetite for new acquisitions closely tied to further land price adjustments, improved financing conditions and easing labour constraints.

Taken together, the signals point to a market that had started to stabilise before the Iran conflict, with expectations of a gradual recovery. Developers were beginning to look ahead to delivering in supply-constrained markets in 2027 and 2028. Now, however, the near-term outlook is one defined by caution and tight viability.

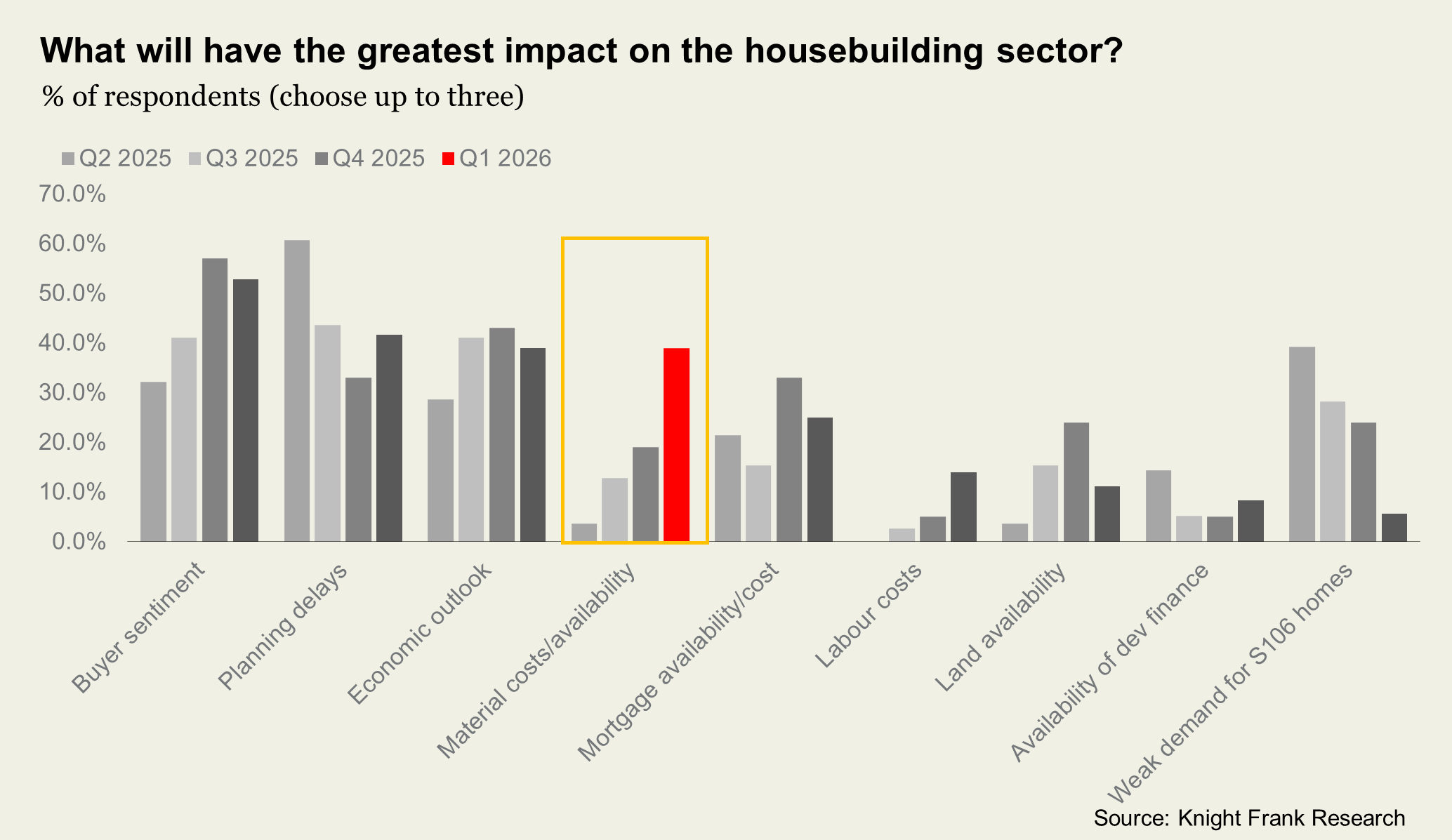

Chart of the month

Concern around materials costs has increased. According to our quarterly survey of small and volume housebuilders, 39% of respondents cited materials costs and availability as a key factor likely to affect the sector in the next quarter, up sharply from less than 20% previously.

Much still depends on the length of the conflict, the scope of any enduring disruption to energy supplies and any subsequent impact on inflation. The increase in energy prices already seen due to the Iran war mean this will be felt hardest for materials that are energy intensive to produce, such as bricks, concrete, cement and aluminium.

Sign up to Knight Frank Research.