Europe’s prime housing markets: mixed momentum ahead of rate decision

European prime residential property markets are showing varied momentum ahead of the European Central Bank’s next rate decision on June 11.

21 May 2026

In some markets, buyers are adopting a more cautious approach, not due to affordability constraints, but timing considerations, as they assess how prices and borrowing costs may evolve. Elsewhere, demand remains more resilient, supported by relatively favourable financing conditions and continued confidence in price growth.

A less predictable outlook for rates

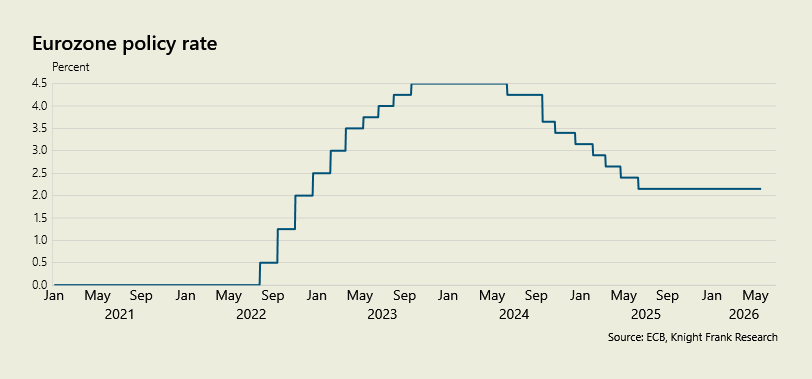

The ECB’s benchmark rate currently stands at 2.15%, unchanged for the past year, but the outlook for its June decision has become less clear.

Oil prices have not surged as sharply as feared, and there is no clear spillover into broader inflation yet, reducing the urgency to tighten.

While short-term inflation may tick up, medium and long-term expectations remain anchored, and wage growth is contained, lowering the risk of persistent inflation.

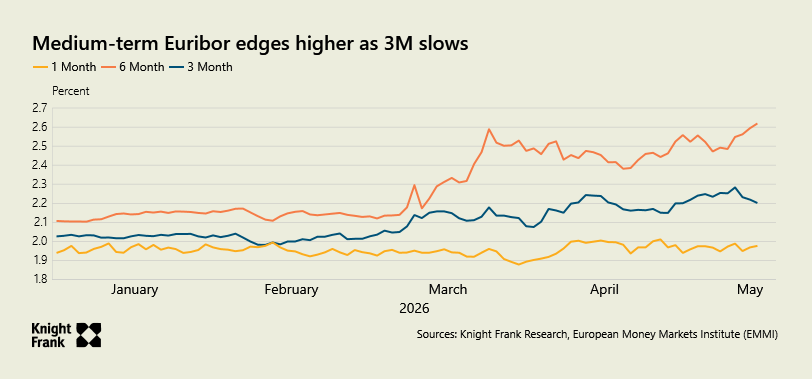

“It’s usually quite clear, but the June decision looks less certain. Part of me thinks the ECB doesn’t need to move yet,” said John Busby, European real estate finance broker at Traverse International Finance, which helps international cross-border buyers secure financing for prime residential and commercial properties. “The one-month Euribor at 1.98% isn’t signalling an immediate increase, while the three-month Euribor at 2.20% could reflect expectations of a hike at the next meeting in July.”

Some still expect tightening to start next month. Markets are pricing in three increases from June, while Bloomberg polled economists anticipate quarter point rises in June and September.

If rates rise, existing differences between markets may become more pronounced, with higher borrowing costs weighing more heavily in some locations than others.

Diverging conditions across markets

The eurozone continues to reflect a range of local market conditions. Southern housing markets, including Spain and Portugal, have maintained relatively strong momentum, supported by significantly lower borrowing costs, with 20-year fixed rates as low as 2.5%, compared with around 3.5–4% in France and slightly lower in Germany.

“We are seeing differing conditions across Europe. I’m currently on the French Riviera, and while I’m not overly concerned about rates rising, the market there is more sensitive,” said Busby. “Agents say activity has slowed since the Iran conflict began; not due to affordability, but uncertainty, with buyers pausing to see if pricing adjusts.”

Financing conditions remain an important factor. While variable mortgage rates across Europe track Euribor, fixed rates are largely shaped by local government bond yields. In some markets, particularly in Iberia, this has supported relatively competitive fixed-rate pricing.

Iberia features prominently in growth forecasts

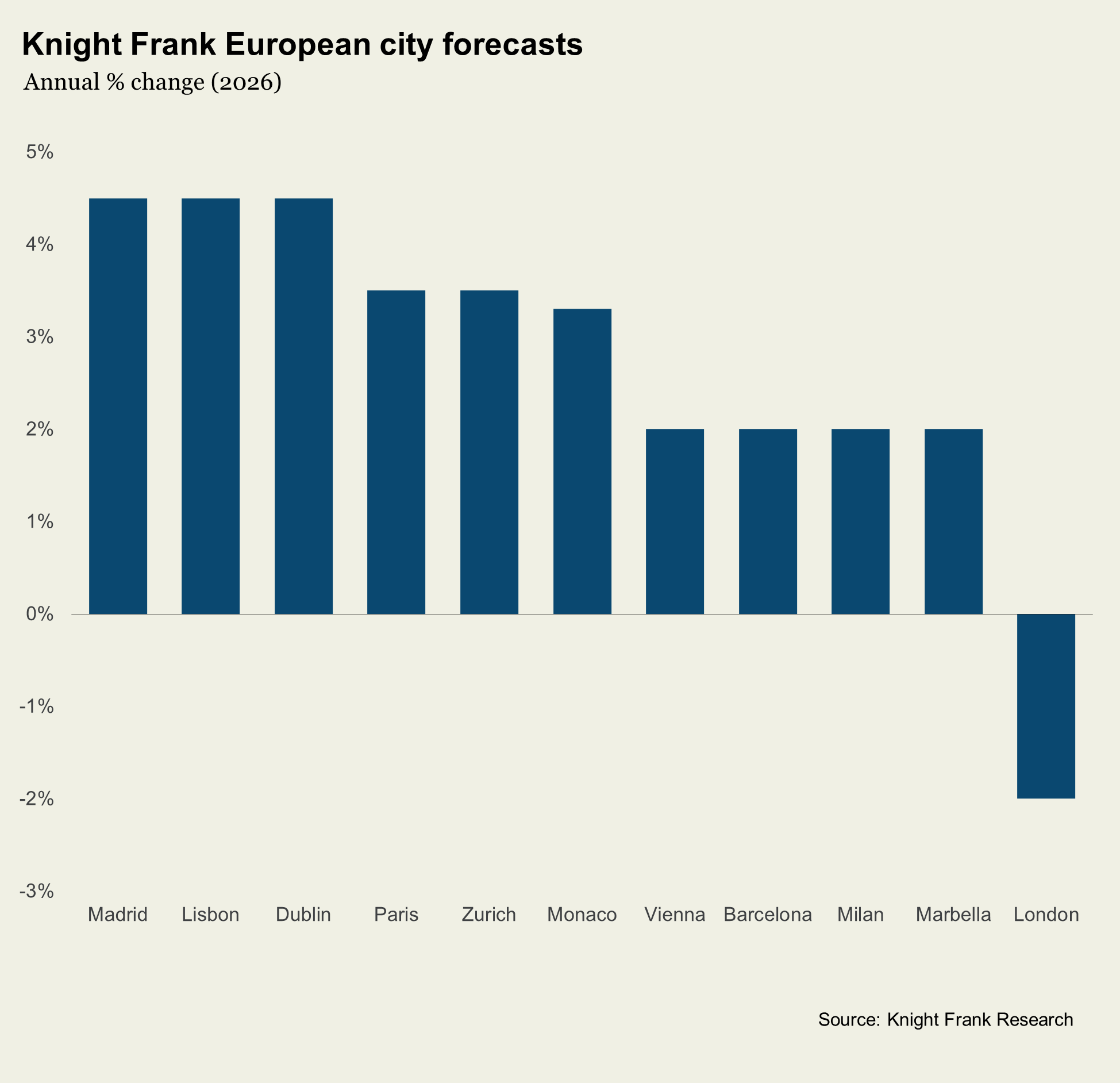

Madrid and Lisbon are top of our prime city price forecasts, with both expected to see 4.5% growth this year.

Strong fundamentals, lower finance costs, deepening international demand and an increasingly sophisticated product offering are supporting this momentum.

Importantly, this performance has persisted despite a shift in policy stance. Spain has ended its Golden Visa and a proposed 100% tax on non EU buyers has yet to materialise, helping steady sentiment. Portugal has removed real estate as a qualifying investment for its Golden Visa programme and phased out the Non-Habitual Resident (NHR) regime, meaning new arrivals no longer benefit from heavily discounted or tax-free treatment on overseas pensions.

Lisbon appears to be entering a second phase of growth, with rising prices pushing some demand into surrounding locations such as Cascais to the west and Comporta to the south.

“Markets such as Lisbon and Madrid are being driven by structural international demand linked to lifestyle, climate, safety, remote working trends and broader wealth migration,” said Sofia Baptista, corporate director at Lisbon-headquartered luxury real estate consultancy Quintela + Penalva. “We are seeing what could be described as a growing ‘lifestyle premium’. Across Europe, lifestyle-led destinations, particularly Mediterranean markets, have generally been outperforming more traditional financial hubs.”

Robust international demand, led by buyers from Northern Europe, the US and Latin America, together with limited prime supply, is supporting price growth across parts of Iberia’s luxury residential markets.

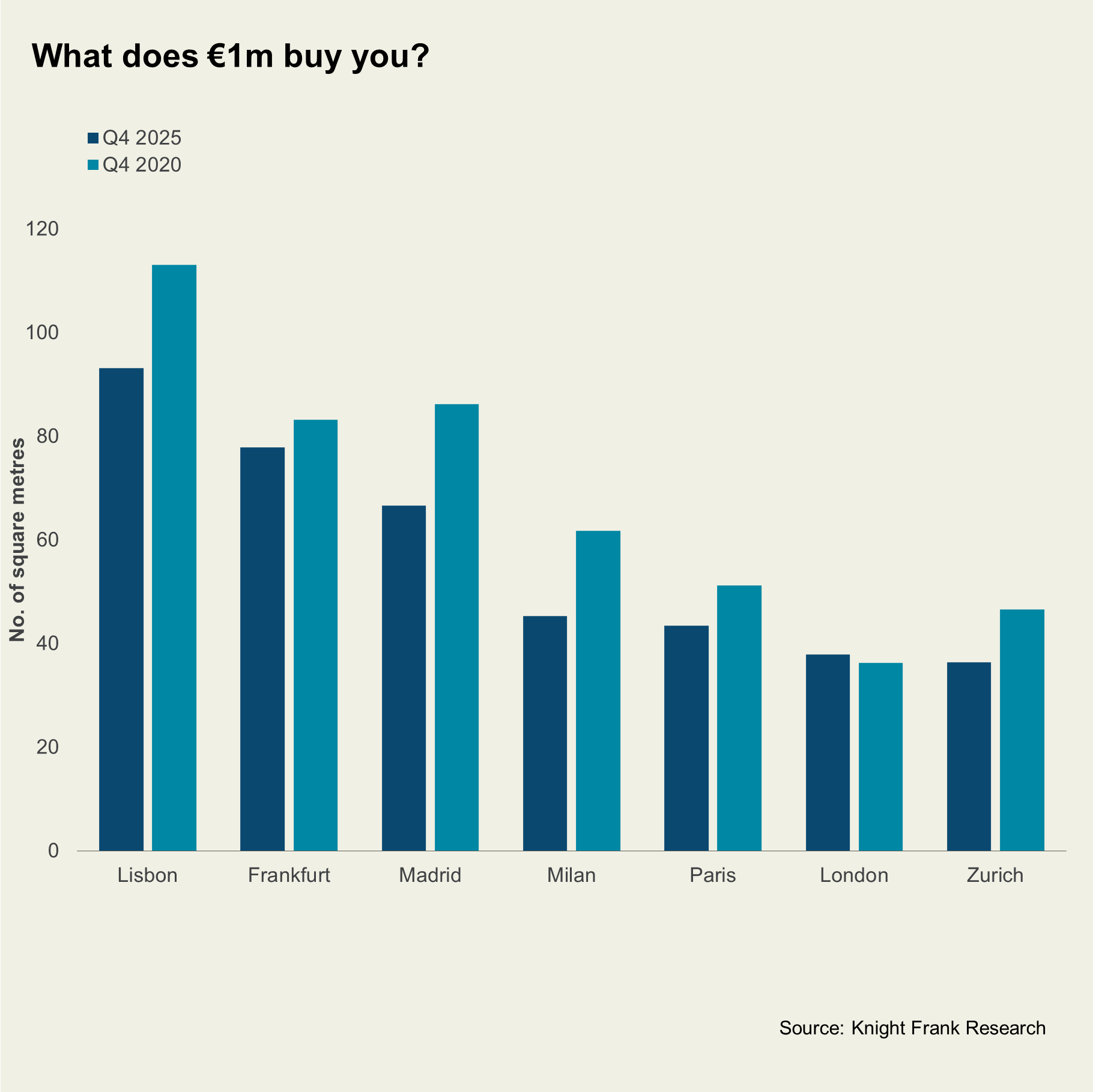

Despite this, relative value persists, especially in Lisbon, where €1 million buys around 93 sq m (just over 1,000 sq ft) of prime residential accommodation, Knight Frank data shows, exceeding most European capitals.

Sign up to Knight Frank Research.