Domestic MEES and Record Wind Auction

Welcome to the first Sustainable Property Insights of 2026. We are kicking off the year with an update on all things MEES (for the domestic private rented sector at least) and look at the latest government moves in the renewable energy space, including the results of the Contracts for Difference auction on offshore wind and changes to existing renewable schemes.

05 February 2026

Warm Homes Plan: the new EPC rules for the private rented sector

The UK government’s Warm Homes Plan set aside £15 billion to accelerate home upgrades across the UK, but one of the biggest shifts for the property sector is the confirmation of new minimum standards for private rented homes. These standards will be tied to the forthcoming reform of domestic EPCs, meaning landlords will soon be working to a new assessment framework.

All private rented properties will need to meet a primary standard based on the new fabric performance metric, broadly aligned to today’s EPC C, alongside a second metric - smart-readiness or heating-system metric - of the landlords choosing. In practice, it creates more than one route to compliance, rather than a one size fits all approach.

The timeline is now clear. All landlords must meet the new standards by 1 October 2030. Any property already rated EPC C or above under the current methodology before October 2029 will be treated as compliant for the remaining life of that certificate. Homes below C at that date will require a new EPC based on the updated metrics to support accurate retrofit planning.

Costs are to be capped at £10,000 per property, down from the £15,000 originally proposed, and will cover eligible work from October 2025, including the new EPC itself. Government estimates put the average upgrade cost at around £5,400 with potential annual bill savings of £210. Low-interest loans will support those needing to undertake works, although the detailed calculation rules are still being consulted on.

The wider EPC reform was partially confirmed with four new headline domestic metrics and a shift to requiring EPCs at the point of marketing. For non-domestic EPCs the headline metric will be unchanged and for both types the 10-year validity will stay in place. For a deeper look, read the full update.

Any way the wind blows

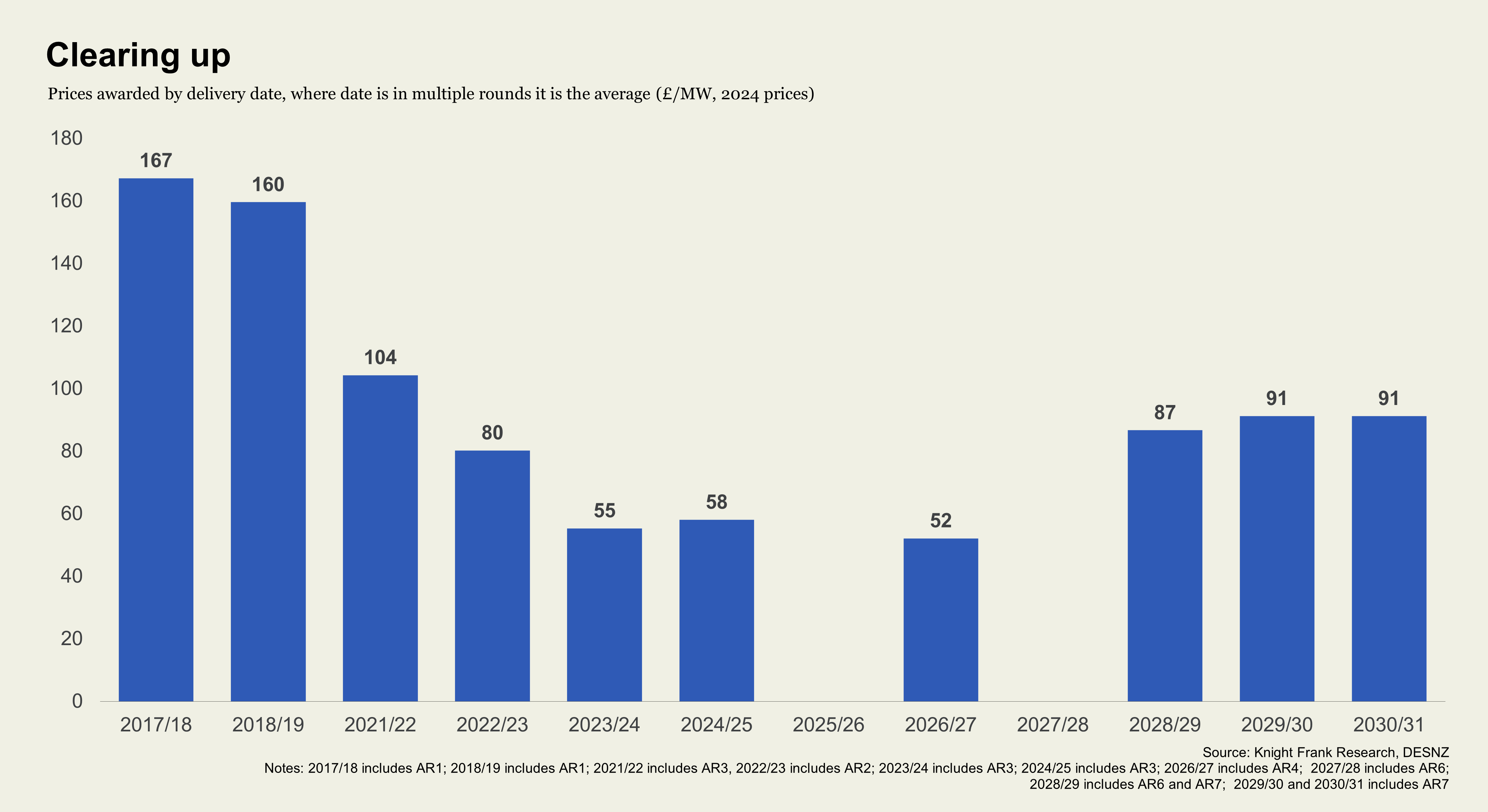

Musical fans may recognise the lyrics from a favoured show of mine, but more pertinently it refers to the latest results from the UK government's Contracts for Difference (CfD) auction for offshore wind (other results expected in the coming days). The CfD process supports renewable build‑out by contracting with the government for some or all generation for 20 years, up from 15 years in previous auctions.

AR7, the seventh round, set a record for offshore wind. A total of 8.2 gigawatts (GW) across 10 projects received allocations, with a strike price of £91/MWh in 2024 prices, the one Scottish project was set at £89/MWh. This was higher than industry expectations, and only 19% below the Administrative Strike Price, compared with an average discount of 24% to date.

The government has set a target of 43 to 50 GW of offshore wind by 2030. With 16.6 GW installed by Q3 2025, according to DESNZ statistics, and around 15 GW under or awaiting construction with contracted capacity, plus some uncontracted projects, estimates suggest (The Guardian and Bloomberg) the UK will need around 7 or 8 GW of new capacity in the next auction. This is widely viewed as the last realistic opportunity for projects to be delivered in time for 2030.

Momentum continued last week, with the UK signing a pact with European nations to drive forward an unprecedented fleet of joint offshore wind projects, taking advantage of Europe's shared North Sea resource. The Hamburg Declaration, as it was dubbed, commits to delivering 100 GW through joint clean‑energy initiatives.

Ian Wood, Head of Infrastructure at Knight Frank Capital Advisory, notes "UK investment in wind energy generated a net benefit of more than £100 billion to consumers between 2010 and 2023, according to a UCL study. It was therefore encouraging to see the Secretary of State increase the AR7 budget during the auction. Achieving the right balance between strike prices and capacity remains critical to keep the UK on track for its Clean Power 2030 mission.”

Index shift

The UK government has confirmed shift from RPI to CPI indexation for the Renewables Obligation (RO)scheme, as well as Feed in Tariffs (FIT) across all nations, taking effect 1 April 2026. This follows two consultations launched in late 2025 and sits alongside the decision to transfer 75% of domestic RO funding to the Exchequer for the Spending Review period to reduce consumer bills.

The consultations explored two options:

- a permanent switch to CPI; or

- a temporary freeze of the RO buy out price at its 2025 26 level with gradual realignment to CPI.

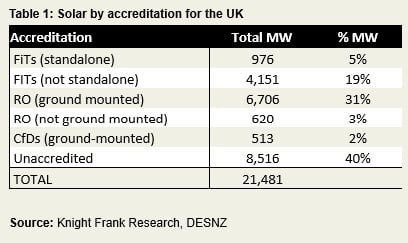

Government feedback shows investors and generators expressed near unanimous concern that any change to indexation is retrospective and undermines policy predictability. Despite this, the government plans to proceed with option 1, the CPI switch, citing consistency with other renewables schemes such as CfDs and the Capacity Market. Over the past five years CPI has averaged 127 basis points below RPI, implying lower long term support values for accredited assets. For solar, around 58% of UK capacity remains RO accredited or on FITs, as at November 2025, see the Table below.

Indexation may tighten financial headroom for projects, with cost bases, such as debt servicing and O&M, linked more closely to RPI. The government noted that they received limited evidence of material impact and argued that long term fixed rate debt has already benefited from recent high inflation. While the decision avoids the additional uncertainty of a buy out freeze, it still represents a negative signal for investor confidence within a scheme designed around long term revenue stability. Bluefield Solar Income fund confirmed around a 2% reduction in their Net Asset Value (NAV) (Proactive Investors) due to the changes.

Before 1 April 2026, the government must make affirmative statutory instruments, after which Ofgem will publish the finalised RO buyout price and mutualisation levels.

What to watch in 2026

- With Minimum Energy Efficiency Standards (MEES) confirmed for the private domestic rental sector, we continue the five year wait for the non-domestic sector changes.

- On regulation: The Ongoing European Sustainability Omnibus (Hogan Lovells) and UK Sustainability Reporting Standards likely to be finalised.

- Interest in infrastructure as asset class for real estate owners and investors continues to grow, as shown by our Active Capital 2026 research.

- The ongoing Connections Reform with Gate 2 contracts likely to be signed in the first half of 2026 and further rounds to open for those meeting qualifications and notably for solar in some regions.

- The remaining results of the Contract for Difference Auction Round 7 - Offshore wind already announced but other tech to follow in the coming days.

- The Strategic Spatial Energy Plan - billed as a 'blueprint' for the future of energy infrastructure - where generation, storage and grid upgrades are required. This will provide more clarity and long-term direction for the sector.

£100 billion - Stat of the Month

The National Wealth Fund published a new Strategic Plan with the ambition to drive £100 billion of investment, create/support 200,000 jobs and save 500 million tonnes of CO2e emissions.

What else I am reading

The European Central Bank published a paper that indicates banks with higher exposure to transition risk face "significantly higher borrowing costs" in the repo market, the ECB also issued its first-ever fine to a bank failing to identify climate risk (Green Central Banking), RICS launch new ESG and sustainability in commercial property valuation, UK EV record year (SMMT), US NE states push for emergency wholesale electricity auction (Bloomberg) that would compel technology companies to effectively fund new power plants, a report from the Energy Systems Catapult exploring ways in which AI solutions are already helping to cut emissions, improve performance, and curb costs across the energy sector, and Europe’s record renewables year (Ember).

Sign up to Knight Frank Research.