Mortgage Costs to Fall as Market Prices in Faster Cuts

Cooling inflation, weak jobs data and stronger-than-expected signals from the Bank of England have boosted rate cut expectations. The main risk for the housing market now is political.

Cooling inflation, weak jobs data and stronger-than-expected signals from the Bank of England have boosted rate cut expectations. The main risk for the housing market now is political.

At the start of February, we called a spike in borrowing costs “reversible”, which it proved to be.

Three days later, the Bank of England gave stronger-than-expected signals around a rate cut and inflation returning to its 2% target, which sent swap rates lower.

Swap prices, which are based on future rate expectations, are used to price fixed-rate mortgages.

Last Monday, we said poor jobs data and declining inflation could drive those expectations even lower.

On Tuesday, the government announced that unemployment had climbed to 5.2%, its highest level in almost five years. Meanwhile, on Wednesday, inflation fell largely as expected.

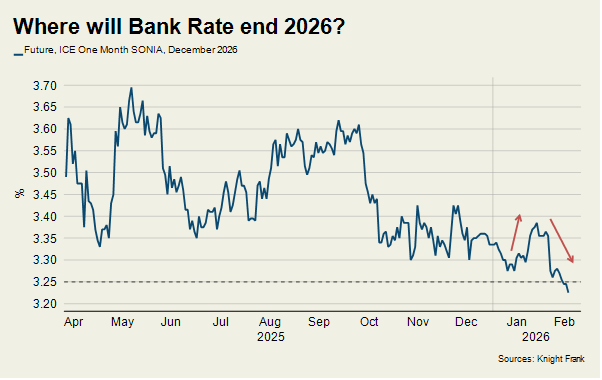

The result is that financial markets began pricing in two cuts this year, which would take Bank Rate to 3.25%, as the chart shows.

It means a cut next month feels like a certainty, said Michael Brown, an analyst at financial broker Pepperstone.

“My base case remains not only that the MPC will deliver a 25bp cut at the next meeting in March, but that such a move will be followed by further cuts as the year progresses, taking Bank Rate to a neutral level of around 3% by the end of summer,” he said.

I discussed what other factors are moving UK mortgage rates with Michael on a recent episode of the Housing Unpacked podcast.

Despite the weaker outlook for the jobs market, mortgage lenders will end February in a better place than they started it. Lower rates will underpin demand in the housing market at a time when political volatility may increasingly cut through with buyers and sellers, as we explored last week.

Even small movements on financial markets have had an instant impact on mortgages.

“Lenders have an appetite to do as much business as possible at the moment” said Simon Gammon, head of Knight Frank Finance. “As soon as swap rates move, they are re-pricing, which is happening regularly at the moment.”

As mortgage rates have moved and deadlines to lock in deals have been tight, application backlogs of have been common, which is a positive signal for underlying demand.

Two-year fixed-rate mortgages were just over 3.5% last week while five-year fixes were closer to 3.75%. The next psychological threshold will be when rates are regularly closer to 3% than 4%.

However, while the picture has improved over the last fortnight, it could still change. The key question now is whether a poorer-than-expected by-election result for Labour this week kickstarts a politically volatile chapter for the UK.

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.