John Lewis and the hard maths of building in UK cities

Making sense of the latest trends in property and economics from around the globe

27 February 2026

Earlier this week, the John Lewis Partnership announced it was withdrawing from its build-to-rent (BTR) business, stating it was conceived in "a very different financial environment: one with more stable investment returns, lower borrowing costs and more affordable costs to build homes."

The decision speaks less to the fundamentals of BTR and more to the broader economics of urban housing development, where higher debt costs, elevated construction prices and onerous regulations have reshaped viability across the board. John Lewis isn't the first to exit and won't be the last; the ONS lumps developers and contractors into one 'construction' category, which recorded the highest number of insolvencies of any sector in the 12 months to November.

The firm is a household name and a long-term investor, and it wanted to bring density to well-connected sites in urban locations – exactly what the government wants. Yet, since the business was launched in 2020, construction costs have surged more than 35%, Gateway 2 was introduced, as were regulations on second staircases, and the company has had a challenging time in the planning process. Back then, Dame Sharon White wanted 40% of group profits to come from non-retail sectors by 2030. Her successor, Jason Tarry, has opted to refocus on the traditional retail business.

Uncertainties of development

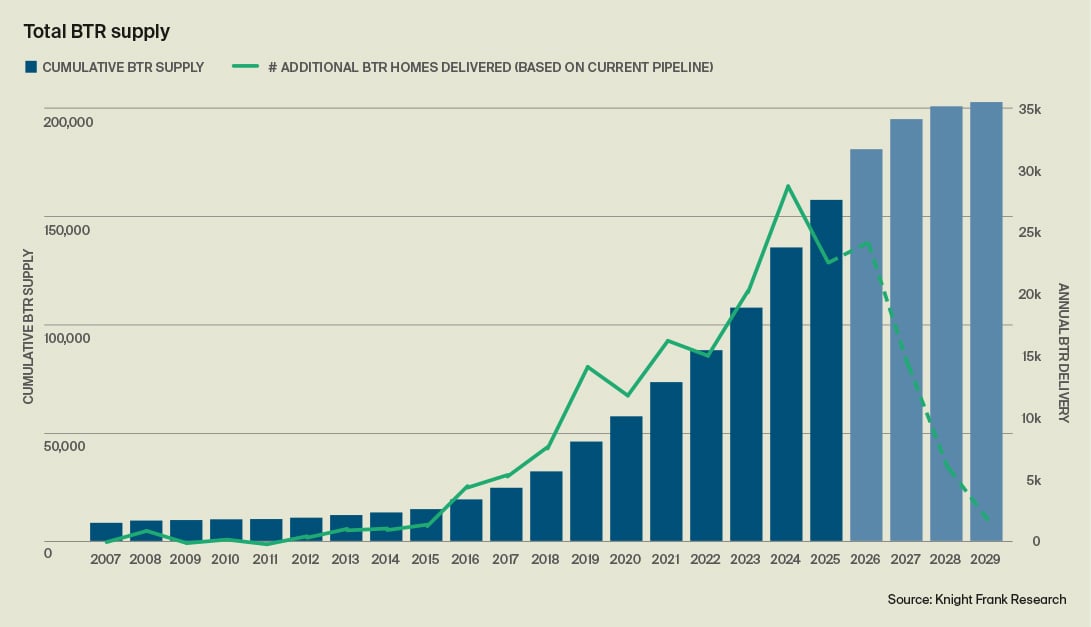

Despite the challenging backdrop, investors continue to seek out footholds in the BTR sector. Annual investment hit £4.7 billion last year, according to Knight Frank data. That's the second-best year on record and 23% higher than the long-term ten-year average.

Operational transactions are expected to gain market share this year as some of the early aggregators near the end of their fund lives and others rationalise non-core assets. These deals also allow investors to gain exposure without navigating the uncertainties of development.

On that front, we are seeing green shoots. There has been some progress at the Building Safety Regulator (BSR), which recently reported that it halved legacy cases in the 12 weeks to December 2025. Meanwhile, viability should improve marginally as borrowing costs ease.

Recent changes to the National Planning Policy Framework – which include the introduction of a “default yes” for developments near train stations and on brownfield land, as well as encouragement for higher-density housing – signal a strong commitment from Government to push forward with planning reform. Recognition of Living Sectors and giving them significant weight in the planning balance is particularly welcome and should clear the way for more positive decisions, which will unlock much-needed housing.

We expect just shy of 24,000 new BTR homes will complete in 2026 based on estimated completion dates for schemes currently under construction. This would represent a slight uptick on last year’s figure. However, a large proportion of these schemes will have been funded in a less challenging development environment through 2023 and 2024. The outlook for new starts, in contrast, remains subdued (see chart).

An ideal environment

Europe is a relative laggard in the race for AI dominance when compared to the US and parts of Asia. Last year, the EU introduced an “AI Continent Action Plan” built around compute, data, skills, lighter regulation and faster AI adoption in an attempt to keep AI companies in Europe and attract global players. Individual nations also offer their own incentives, visas and hubs.

This newsletter tracks the various holes and inconsistencies in UK government policy, but this is an area that is going relatively well. Yesterday, OpenAI said it would make London its largest research hub outside the United States, citing Britain's technology ecosystem as an ideal environment in which to invest and develop new artificial intelligence systems.

Granted, this is largely about Britain's long-running strengths rather than any specific policies; Mark Chen, OpenAI's research chief, says the UK's mix of talent, leading universities and scientific institutions gives it leverage in a sector governments worldwide view as strategically important.

However, there has also been a sensible, targeted policy push – for those interested, I recommend 'New Frontier', Jennifer Townsend's weekly science and innovation update. This week's edition included details of UK Research and Innovation's debut AI strategy, which commits £1.6 billion over the next four years, with an explicit focus on expanding doctoral and fellowship routes co-designed with business to build the talent pipeline.

More uncertain

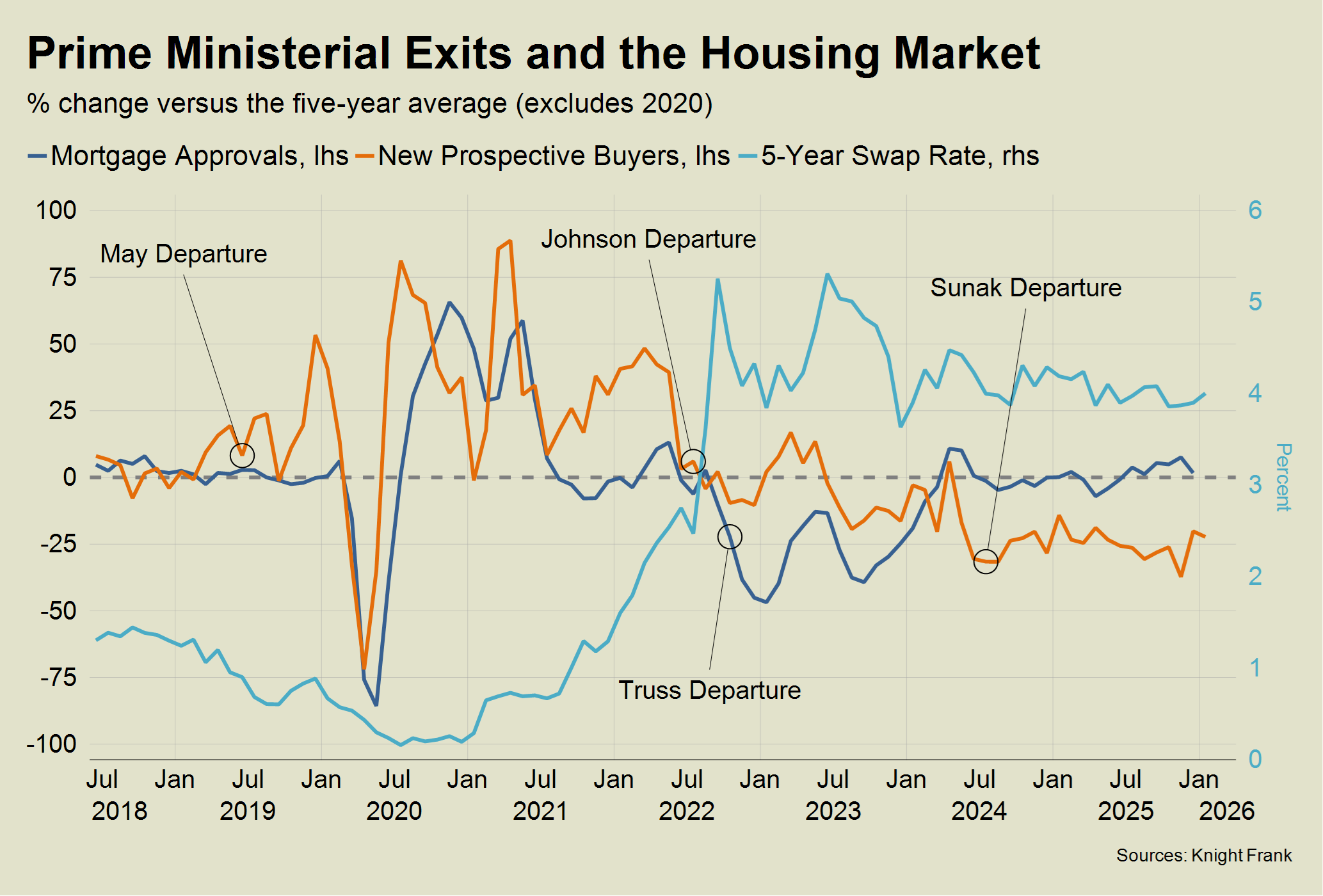

Earlier this month, Tom Bill created the chart below to look at how the housing market coped during the last four prime ministerial departures. This was shortly after the "coup that never was." The answer was not very well, at least in the short term.

"A worse-than-expected result at the Gorton and Denton by-election next week, more revelations about government appointments or a poor set of local election results in May are three possible triggers for" Keir Starmer's exit, Tom wrote. "The only uncertain thing is the timing."

Well, overnight Labour lost the Gorton and Denton by-election, formally one of its safest seats. Labour won just over half the vote in 2024, but secured a quarter this time, with the victorious Green Party surging to 40%.

John Curtice, Britain's most respected pollster, said the result was "very poor" for Labour and means the "future of British politics looks more uncertain than at any stage" since the end of World War Two – per Reuters.

In other news...

London Running Short of Offices Is Great News for the City (Bloomberg).

Sign up to Knight Frank Research.