UK BTR market update Q4 2025

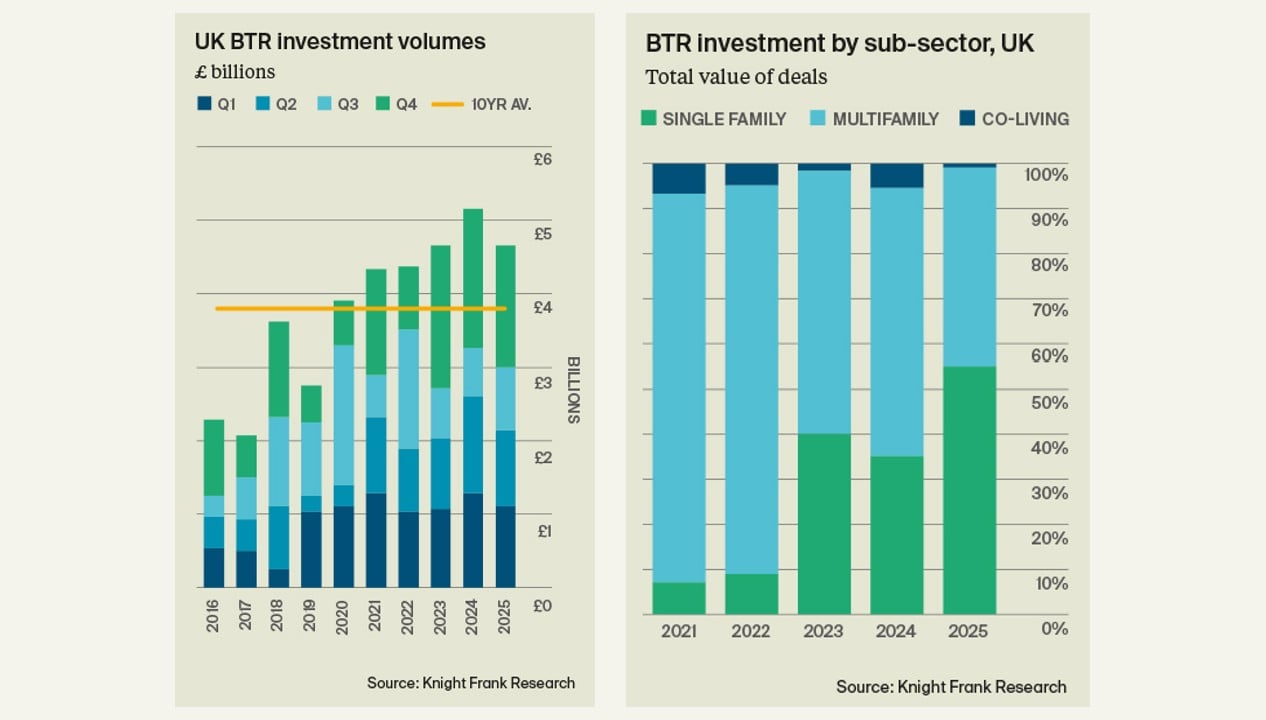

A strong final quarter pushed annual investment in 2025 past the £4.7 billion mark, down on the record-breaking 2024 but ahead of long-term trends.

22 January 2026

Late surge amid a softer year

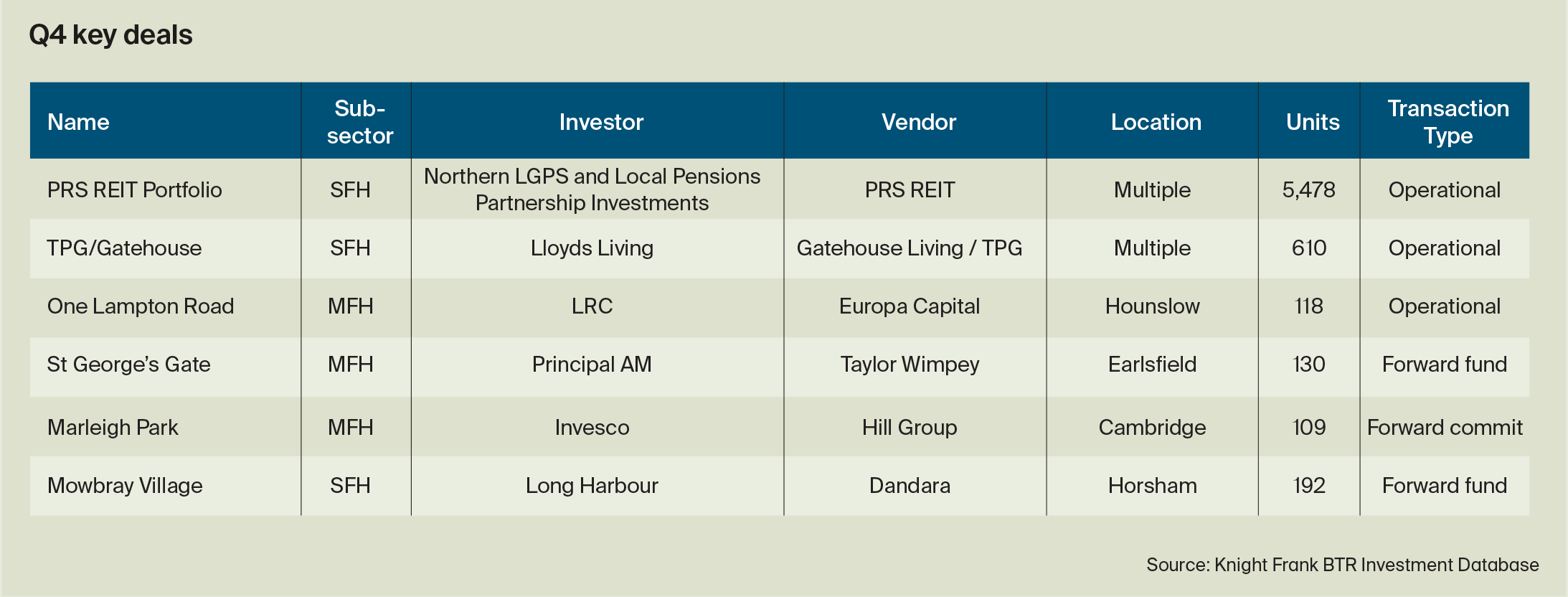

Some £1.7 billion was invested in the final three months of 2025, marking a strong end to a year which has been shaped by ongoing macroeconomic challenges that have weighed on investment activity across all real estate sectors. Investors navigated a year of still elevated debt costs, ongoing material and labour-cost inflation, and regulatory hurdles, which have limited development opportunities, particularly in the multifamily and co-living markets. In this environment, annual investment of £4.7 billion – the second best year on record and 23% higher than the long-term ten- year average – affirms BTR’s relative resilience while also not hiding the challenging backdrop. The fourth quarter was, once again, a bumper period for investment as investors sought to complete transactions ahead of year- end – Northern LGPS and Local Pensions Partnership Investments’ £629 million acquisition of a housing portfolio from PRS REIT was the standout deal. In four of the last five years, Q4 has seen the greatest share of annual investment. That said, total spend over the course of the year was 9% lower than the record £5.1 billion invested in 2024 and marked the cessation of five consecutive years of rising investment volumes into the sector.

Diversification gathers pace

While multifamily housing (MFH) remains the cornerstone of the market, with more than £2 billion invested in 2025, single family (SFH) assets again performed strongly, accounting for 55% of investment and overtaking MFH for the first time on an annual basis. In total, a record £2.6 billion was invested acquiring or funding houses for rent in 2025 across 44 deals, as established players expanded their portfolios and new capital entered the market. We expect 2026 will see investors continue to pursue investment across both houses and apartments as part of a diversified UK residential investment strategy.

Macro resilience

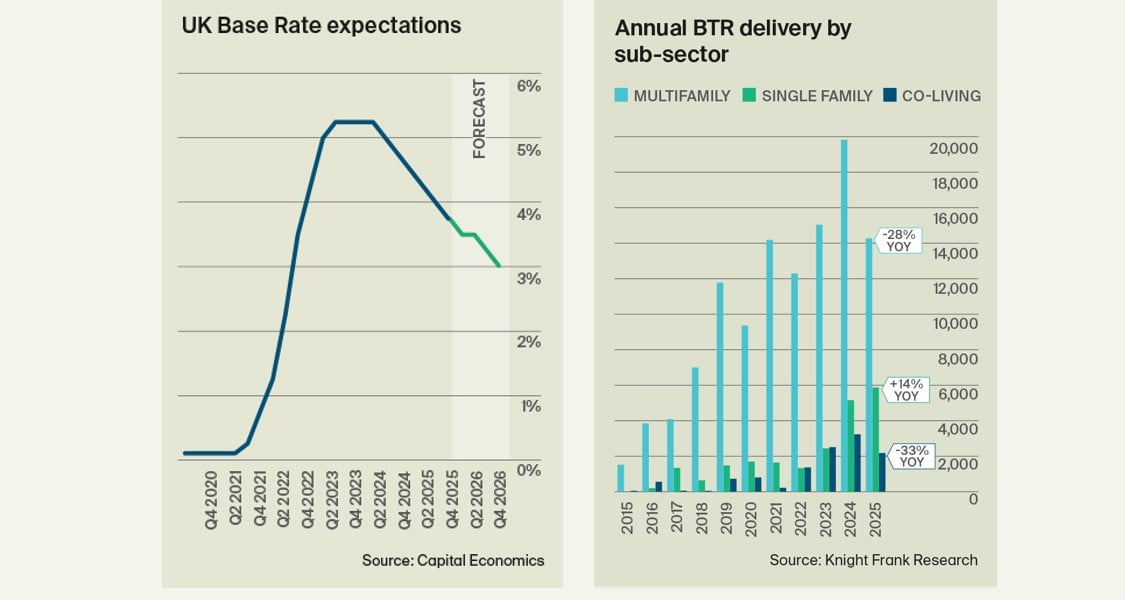

In December, the Bank of England (BoE) cut its benchmark interest rate by a quarter point to 3.75%, as rising unemployment and the UK’s stagnating economy eased concerns about inflation. Further base rate cuts are expected in 2026, which will improve the pricing of debt available to investors. However, market opinion remains divided on the pace of easing, reflecting both the fragility of the recovery and dissent on the Monetary Policy Committee about the wisdom of the monetary loosening. Capital Economics expects three cuts in 2026 while financial markets are pricing in one to two.

What’s in store for 2026?

Investor demand in 2026 is likely to focus on assets that align with the deepest pools of occupier demand, particularly in the mid market. To do this, investors will have to navigate the development opportunities arising from planning reforms, alongside ongoing challenges around building safety requirements and continued pressures around construction viability. There has been some progress here with the Building Safety Regulator (BSR) reporting that it halved legacy cases in the 12 weeks to December 2025, but there is further to go. Operational transactions are also expected to gain market share as some of the early aggregators near the end of their fund lives and others rationalise non-core assets. Investor appetite for co-living will also rise as the viability gap narrows. The Renters’ Rights Act will also shape the year having received Royal Assent at the end of October.

While operators and investors have been preparing for its implementation, the ability of tenants to challenge rent increases at a Property Tribunal, alongside the removal of rent review clauses, will require a period of adjustment and may lead to moderately higher management costs in the short term. In Scotland, the passing of the Housing (Scotland) Act into law on 6 November 2025 – which provides much needed clarity on rent control exemptions for BTR – has materially improved investment conditions and should support renewed interest in the sector.

Delivery slows but SFH gains share

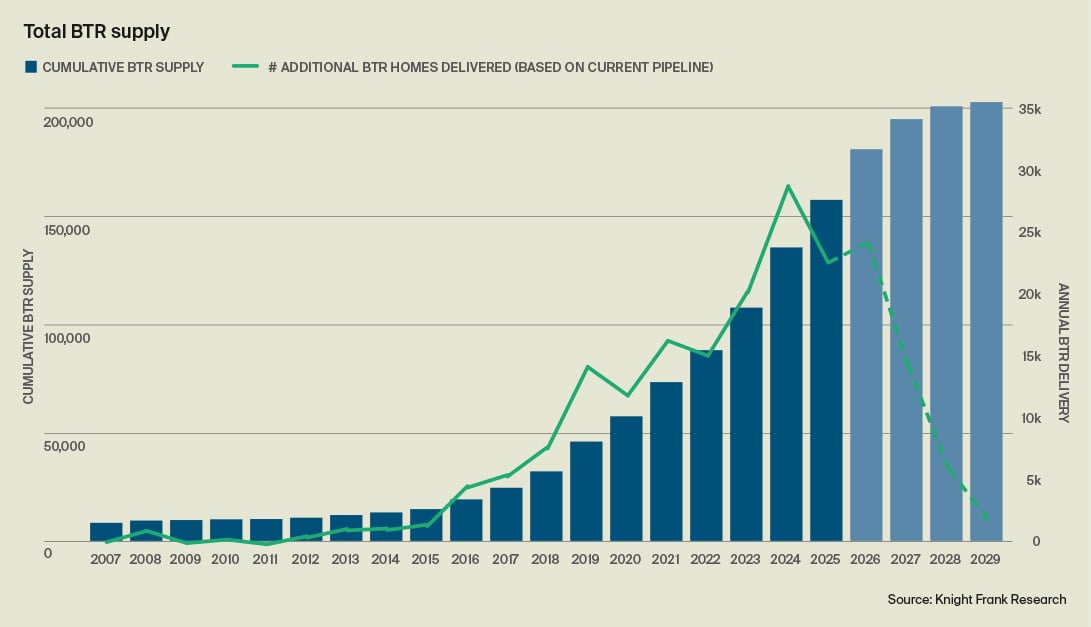

The UK’s BTR stock now stands at 158,205 complete homes, 16% higher than at the end of 2024. There are a further 51,755 homes under construction meaning the sector should rise to more than 200,000 operational homes within the next few years. In 2025, more than 22,000 new BTR homes were completed, around a fifth lower than the record 28,000 completions the previous year. Single-family housing accounted for 25% of total BTR delivery in 2025, up 14% year-on-year and the highest share on record, a reflection of rising levels of investment. In contrast, delivery of multifamily and co-living schemes declined by 28% and 33% respectively, with persistent viability and regulatory challenges limiting high-density urban development.

Building block(er)s

We expect just shy of 24,000 new BTR homes will complete in 2026 based on estimated completion dates for schemes currently under construction. This would represent a slight uptick on last year’s figure. However, a large proportion of these schemes will have been funded in a less challenging development environment through 2023 and 2024. The outlook for new starts, in contrast, remains subdued. While the BTR pipeline includes a substantial 116,000 consented homes, the ability to translate approvals into viable schemes is the next step. Unlocking this backlog will be essential to sustaining construction activity and presents an opportunity for investors seeking to deploy capital into de risked, consented projects. Recent changes to the National Planning Policy Framework – which include the introduction of a “default yes” for developments near train stations and on brownfield land, as well as encouragement for higher density housing – signal a strong commitment from Government to push forward with planning reform. Recognition of Living Sectors and giving them significant weight in the planning balance is particularly welcome and should clear the way for more positive decisions which will unlock much-needed housing.

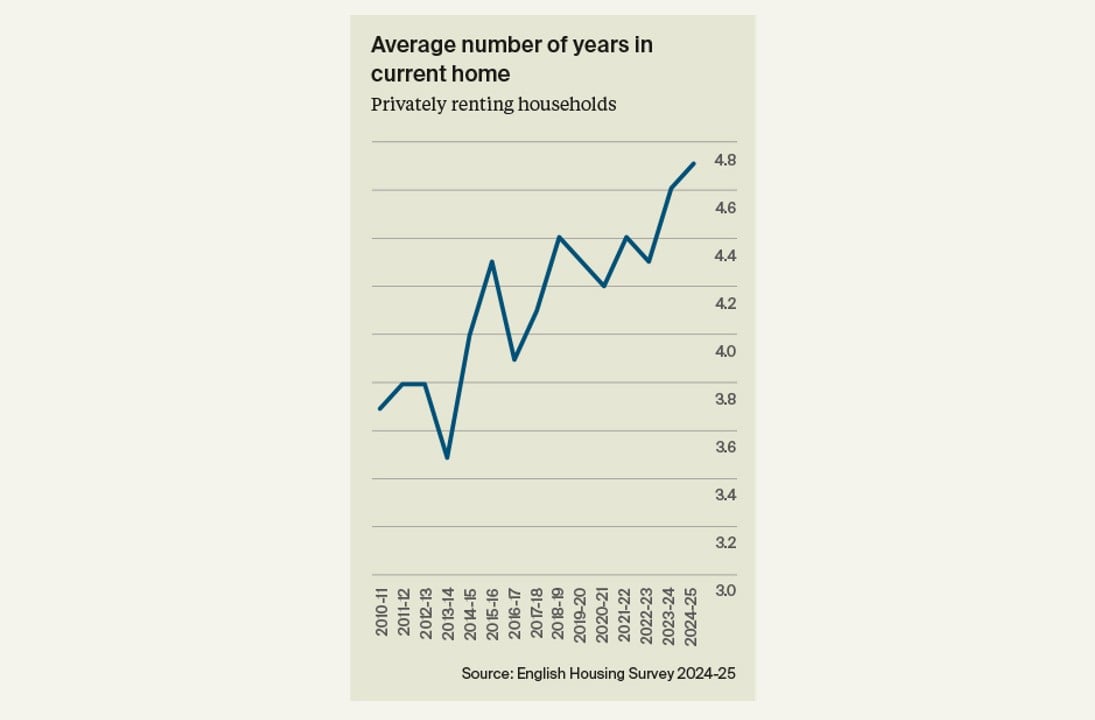

Locking in demand

Upward pressure on rental values over the last few years – particularly for new lets – has encouraged privately renting households to remain in their homes for longer, constraining turnover and exacerbating supply pressures. The latest data from the English Housing Survey shows that the average length of a tenancy for PRS households has increased to 4.7 years, up from 3.5 years in 2014, highlighting a structural shift towards longer term renting. Demand is further underpinned by affordability constraints, with 42% of private renters not expecting to buy a home and 48% of PRS households holding no savings, limiting their ability to accumulate a deposit. As the average age of first time buyers continues to rise, the time spent in the rental sector is lengthening, reinforcing sustained demand for rental homes and creating a stickier tenant base for BTR.

Download the PDF here

Research

We like questions, if you've got one about our research, or would like some property advice, we would love to hear from you.

BTR

Valuation, Capital Advisory and Planning

Recent Living Sectors Research

Prime residential

The Residence Report

The global perspective on luxury residential development

08 September 2025

Towards a New London Plan

16 July 2025

Build-to-rent and Multifamily

Build to Rent Resident Experience Index

Our Build to Rent Resident Experience Index measures the lived-experience for residents in BTR schemes, and identifies what “best-in-class” looks like.

11 September 2024

Land & Development

Co-Living Report

Our Co-Living report outlines the opportunity for funders and developers to capitalise on the solid near-term and projected long-term demographic trends underpinning the rapid growth of the sector, as well as providing a detailed analysis of the development pipeline.

03 July 2024

Land & Development

Affordable Housing Report

In this report, we assess the state of the UK affordable housing sector. A slowdown in housing delivery comes against the backdrop of a long-term need for more housing of all tenures, but particularly for affordable housing.

20 June 2024

Land & Development

Biodiversity Net Gain Guide

Biodiversity Net Gain (BNG) is an initiative that requires every new development in England to have a measurable increase in biodiversity compared to the pre-development baseline (before the development took place).

22 April 2024

Land & Development

South East Residential Development Review

Knight Frank's review of the key development and investment themes in the South East land market

29 November 2023

Land & Development

Focus on: Hammersmith & Fulham

This report provides a detailed analysis of the residential market in Hammersmith & Fulham. The report examines market dynamics, demand and the development pipeline.

27 June 2023

Sign up to Knight Frank Research.