Connection reform update: a new pipeline announced

In early December, NESO confirmed the latest stage of connections reform with the outcome of the first Gate 2 criteria. A new ‘queue’ has now been formed.

In early December, NESO confirmed the latest stage of connections reform with the outcome of the first Gate 2 criteria. A new ‘queue’ has now been formed.

NESO’s Gate 2 outcome marks a structural shift in grid access, reducing oversubscription and defining a phased pipeline to 2035. While solar and onshore wind have some capacity remaining, battery projects were significantly cut and remain over target capacity ranges.

NESO confirmed the successful applicants as part of the ongoing grid reform process. Overall, 283 GW of generation and storage capacity and 99 GW of transmission-connected demand were successful and will be split into Phase 1 – connected by 2030 – and Phase 2 – connected by 2035, dubbed the new pipeline. Prior to the this, the connections queue was four-times the required capacity, reaching 722 GW, with many ‘zombie’ project clogging up the queue preventing deployment of viable schemes.

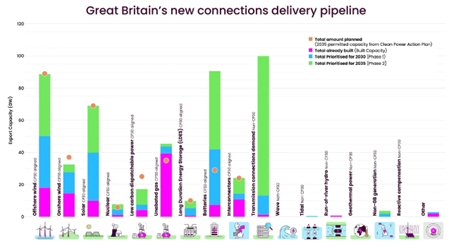

The below chart demonstrates the capacity by technology type, split by Phase 1 and 2, mapped against the Clean Power 2030 Action Plan targets. The key takeaway being that most of the CP30 capacity is met by 2035 across all technologies, except for batteries which are ‘significantly oversupplied’.

Another application window will open in late 2026. This will, however, be limited by technology type and location, as discussed below, as well as those which have become ‘protected’ under Gate 2 criteria. The specific criteria for Gate 2 is:

And for protection status:

Source: NESO

Solar: Almost 30 GW has received Phase 1 status and will be prioritised by 2030, with a further c.30 GW for 2035. As pointed to by NESO, some zones have capacity. For Phase 1, most zones are undersupplied due to a lack of ‘ready’ projects, yet for Phase 2 some are oversupplied, with Northern England, South Wales & Severn, and South West England most notable.

Onshore Wind: Around 12 GW have received Phase 1 status and will be prioritised by 2030, with a further c.5 GW for 2035. There is oversupply in Scotland and undersupply across England & Wales, as anticipated. The next application window will allow for ‘ready’ projects in England & Wales but only ‘protected’ projects in Scotland.

Battery: As mentioned, there is significant oversupply of capacity for batteries, with only those protected – a total of 83 GW – receiving Gate 2 status, an overshoot by c.60 GW. The CP30 targets are for just shy of 30 GW. The next window will not be open to new battery projects, except for those receiving protections since the last window. In addition, there has been a move to cut hybrid battery storage alongside proposed solar farms to curtail overcapacity.

Furthermore, on transmission demand, NESO estimates that around 13 GW can connect before 2030, with a further 86 GW slated for connection between 2030 and 2035. There has been a notable uptick in demand connection requests which has ‘exceeded even the most ambitious forecasts’. The Ofgem Demand Connections Update highlighted that contracted demand capacity jumped from 41 GW in November 2024 (17 GW transmission, 24 GW distribution) to 125 GW in June 2025 (97 GW transmission, 29 GW distribution), with data centre projects driving a significant share of this increase.

In the three months to mid-July (latest data available on the Renewable Energy Planning Database: REPD), some 1.6 GW of solar, 920 MW of onshore wind and almost 6.5 GW of battery projects were granted planning permission. Over six months, to around the time the queue was paused, some 3.8 GW of PV, 2.3 GW of onshore wind and 15.2 GW of batteries have been granted permission. The results of the latest Contracts for Difference – Allocation Round 7 – have yet to be announced but also feature in protections.

Also in December, Ofgem began consulting on the next steps of ‘Connections End-to-end Review’. This includes proposals for companies being required to meet connection dates in connection agreements – There should be proportionate requirements on network companies and NESO to meet agreed customer connection dates in connection agreements, commensurate with those on developers to meet project milestones."

The consultation will run until the end of February 2026 with outcome expected in summer 2026.

Almost a year on from pausing the connections queue, momentum is building. However, there is more to come. Without progression, projects can still be ‘kicked out of the queue’, as well as potential charges for not meeting deadlines, which come into force in January 2026. In addition, clarity is required on behind the meter projects, such as rooftop PV.

These must also be seen in the broader context. The Government, for example, increased the threshold for Transmission Impact Assessment (TIA) from 1 MW to 5 MW, reducing barriers for smaller solar projects regarding scrutiny of grid queues. Importantly, there is more to come with the publication of the Strategic Spatial Energy Plan expected in Q2 2026, adding to the overarching momentum of renewables in the UK.

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.