Green shoots: spotlight on renewable energy

With renewed momentum and autumn approaching in the UK I focus on renewable energy, highlighting not only the growth in deployment but activity in transactions of both ready-to-build and operational sites.

11 September 2025

Going green

With demand for electricity set to grow by 3.3% this year and 3.7% next year, there is a need to build capacity across geographies. Renewable energy is seen as supporting this growth, while also enabling the transition to cleaner energy. In fact, renewables are set to overtake coal as the world's largest source of electricity this year or next, according to the latest report from The International Energy Agency (IEA). Despite the One Big Beautiful Bill removing tax breaks for wind and solar in the US, other countries have continued to spur investment. For example, PV generation grew 45% over the past 18 months in China, as developers got ahead of phasing out of incentives and India installed a record 25 GW in 2024.

In the UK, solar power capacity and generation is surging. By mid-August this year, the generation from solar surpassed the entirety of 2024, thanks to a growth in capacity and favourable weather (2025 is 'almost certainly' the UK's hottest summer on record). According to official figures, capacity has grown by 6 GW across renewables in the past 18 month period led by almost 3 GW of solar - although industry estimates are higher, according to the FT. The direction of policy is a doubling down on clean energy growth through the UK Modern Industrial Strategy, Clean Power 30 Action Plan, Solar Roadmap, Onshore Wind Strategy and Connections Reform, the list goes on. All of this in support of the pledge for electricity to be 95% low carbon by 2030, up from two-thirds in 2024.

The public is behind this drive. Eight in ten adults support renewable energy expansion in the UK, according to a YouGov survey. Support is highest among Lib Dem and Labour voters (93% and 91%) but still broad-based with 60% of Reform voters also supporting. Although perception, as noted previously by the Climate Barometer, is that there is lower support and this gap has been widening. There is some way to go to close that to ensure the roll out continues at pace to enable a transition to low-carbon energy.

A piece of the pie

The policy backdrop supporting cleaner energy, and importantly more of it, is to drive the electrification of buildings, transport and industry. This not only shifts existing energy demand towards electricity but meets growing new demand for electricity from the use of air conditioning. The IEA has already highlighted the increasing number and extent of extreme heatwaves globally (with 2024 the hottest on record), as well as the growth in data centres and the advent of AI. Therefore we need deployment to increase at a rapid clip with targets to more than double solar by 2030 and treble offshore wind. The investment market for renewables has been growing with this context.

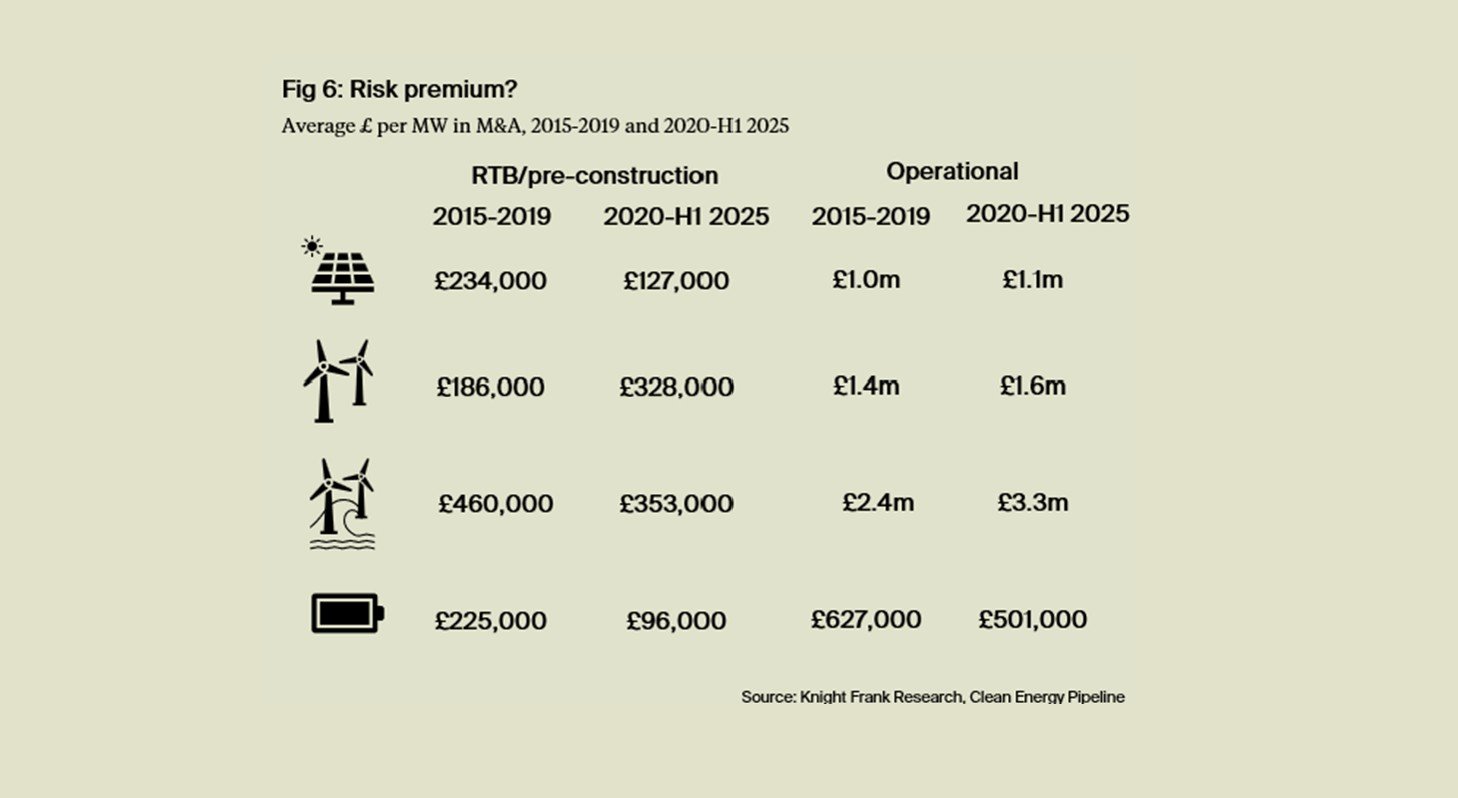

A record £4.4 billion of mergers & acquisitions transactions for ready-to-build (RTB) and operational solar, onshore wind and battery energy storage solutions (BESS) was achieved in 2024, according to our new report with data from Clean Energy Pipeline. While the record capacity of more than 6 GW was achieved in 2023, the mix of technologies pushed 2024 to reach higher volumes with under 5 GW of capacity transacted. However, 2025 may prove a record in capacity transacted with 4.4. GW reached already in the first half of the year. Whilst BESS has overtaken solar for the first time to be the dominate technology, given the lower average relative values, particularly in the ready-to-build stage assets, see below, overall investment volumes remain below £1 billion.

The report delves into the perceived risk premium and resultant £ per MW by technology type and whether the asset was ready-to-build (RTB) or operational. Over the past five years the risk premium and cost gap has widened driven by a fall in the average RTB values, with the exception of onshore wind. This reflects the higher risks particularly from construction costs and delays. Solar has the greatest differential on a £ per MW basis, with the average for 2015-19 being £234,000 for RTB compared to £1 million for those operational (4.4 times). That gap has widened to £127,000 and £1.1million, respectively, (8.8 times) for the 2020-H1 2025 period. See the report for more analysis.

Shining on solar

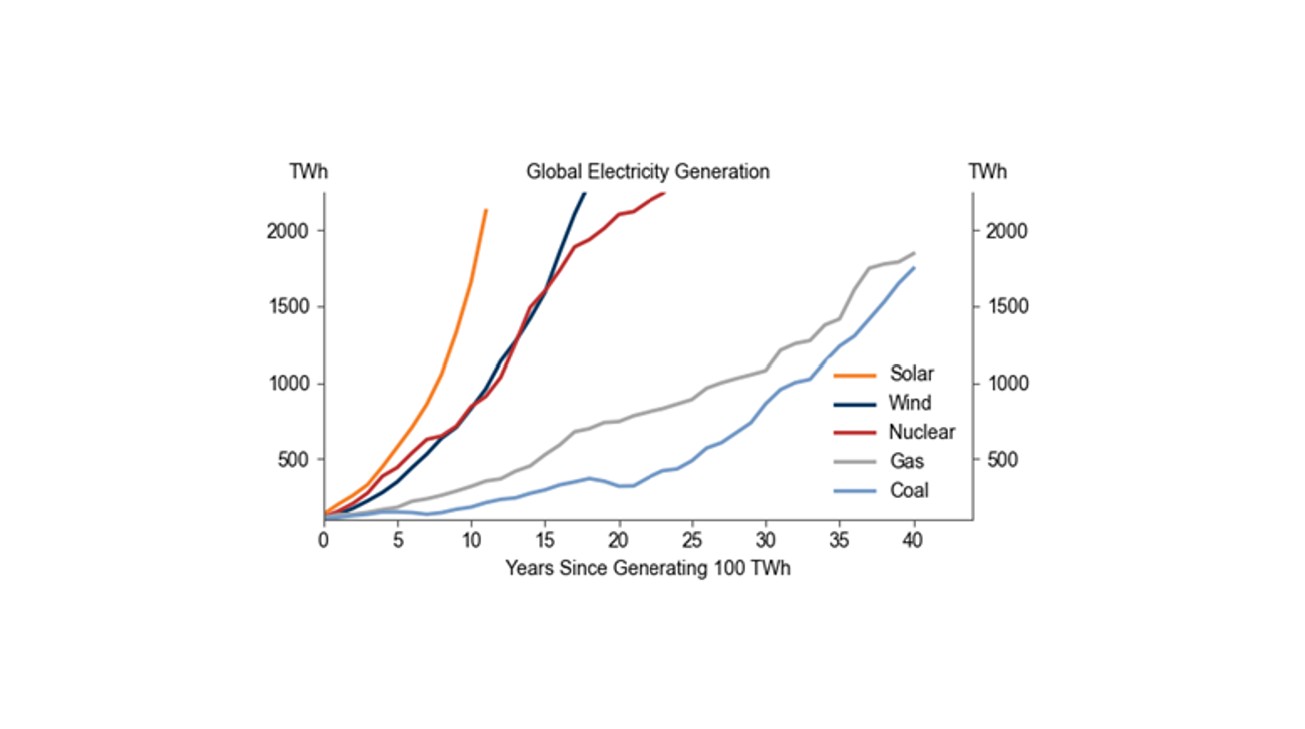

The growth in solar electricity generation has far outpaced any other source, reaching 2,000 TWh from 100 TWh in under 10 years, as shown by Goldman Sach research. By comparison, see chart, wind and nuclear took around 15 years with gas and coal over 40.

They point to three reasons for this:

• First, with costs dropping by 20% as cumulative production doubles, some 90% in the past decade- which has reduced investment costs faster for solar panels than for any other investment good;

• Second, and I believe very importantly, solar's marginal fuel costs are zero; and

• Third, modular solar panels allow decentralised power production, which can contribute to energy security and tends to have solid public support.

There have also been recent studies indicating that the lifetime of solar may be more than initially thought, with panels in Switzerland still producing reliable electricity after 30 years.

In our report, we look at blockers on a utility-scale level but for commercial landlords and residential homeowners many remain. The UK Solar Roadmap (see our summary here) is seeking to address some of these, such as helping to simplify and formalise landlord/tenant and lease agreements with solar involved, which will help to unlock the valuation impact more clearly.

While on-site or private wire arrangements are prioritised in the energy procurement hierarchy, for some it may not be possible and as such we are seeing a growing demand for corporate power purchase agreements (CPPAs) as we explore in our Renewable report. From three publicly announced CPPAs in 2019, to 18 in 2024 and eight thus far in 2025 - this is seen as an opportunity to secure long-term renewable power, which meets the additionality element for zero-carbon requirements. As the government look to expand and formalise this market we could see greater activity.

What else I am reading

Is not including solar in the new London Plan a missed opportunity? We explore in Planning a sustainable London as well as the complete Towards a New London Plan report. The UK's National Wealth Fund to invest upto £200 million in battery storage, and could reforming electricity pricing make heat pumps more attractive? China has deployed record levels of solar, and big on electrifying the economy and transport with EVs accounting for around half of new car sales in 2024. The shift and support has enabled industrial and manufacturing growth with BYD is now the largest EV manufacturer globally.

Sign up to Knight Frank Research.