Déjà Vu: Trump, ESG backlash and MEES plus what does the Clean Power 30 Action Plan entail?

In this edition, I explore the evolving role of ESG under the Trump 2.0 presidency, highlighting its resilience despite political shifts, examine investor attitudes and regulatory trends, including the potential cost to upgrade the residential private rental stock of England & Wales, and finally break down the UK’s Clean Power 30 Action Plan and its implications for grid connections and renewable investments.

13 February 2025

ESG under Trump 2.0

One of Donald Trump’s first actions in his second term as president was to pull the US out of the Paris Climate Agreement. The move has put ESG firmly in the spotlight. It has also highlighted just how big a 'marketing problem’ ESG has, particularly among populists, who often see it as placing morals above returns in the business world, rather than as a framework for value preservation, creation and risk management. The recognition of the latter means that it is embedded into many strategies; therefore, its importance is unlikely to wane.

At its core, ESG is about identifying, measuring, and mitigating risk, therefore ESG remains highly relevant, regardless of noise surrounding major financial institutions having exited Net Zero initiatives, or executive orders signed.

It's important to remember that during the first Trump presidency, ESG considerations actually grew, despite the first Paris Agreement withdrawal. A good example being the Taskforce for Climate-related Financial Disclosures (TCFD) which was introduced in 2015. The number of organisations supporting the TCFD recommendations grew to more than 1,500 supporters by the end of Trump’s first term and almost reached 5,000 by 2023 when it was disbanded and embedded into international standards.

Despite around 20 US states adopting 'anti-ESG' regulation, corporate sentiment remains strong, with 48% of global business leaders (54% in the US) citing climate change as the primary risk driving operational disruptions in the coming decade. The World Economic Forum echoes this, ranking extreme weather as the top 10-year global risk for the second year running. For real estate it is more acute. According to the latest INREV Investment Intentions survey, 81% see climate change impacting investments in global real estate.

Outside of the US, the UK has reaffirmed ambitious emissions targets, many mayors in US cities remain steadfast and Ursula von der Leyen stated that Europe would "stay the course, and keep working with all nations that want to protect nature and stop global warming."

In recognition, the commitment to more sustainable buildings continues to grow. In London, for example, annual take-up for offices with top-tier BREEAM and EPC ratings has increased by 87.2% since March 2020. In contrast, demand for lower-rated offices has seen a 35.2% decrease over that same time. The RICS 2024 Sustainability report highlighted that interest in sustainable built assets among investors and occupiers across the global rose for the fourth consecutive year and a new report shows that energy use intensity (EUI) has fallen in offices across the US by 20% over the past five years, with those in the EU seeing an 18% drop.

For real estate, there is a clear trend towards recognising the fundamentals of ESG and embedding it into decisions and investors are driving this. The same INREV survey found that 68% consider net-zero carbon commitments when investing into non-listed funds. Our own Living Sector Survey found that 81% of respondents stated that a push towards ESG within assets is driven by investors, higher than the 75% citing regulation and 59% citing residents. Our NextGen Living report notes that "as more investors consider ESG a key criteria in underwriting investment, the demand for, and consequently the liquidity of, buildings with green ratings is likely to increase. Green-rated buildings are more likely to be future-proofed against potential legislative changes, as well as being future-proofed against shifts in resident sentiment and preferences."

We will delve into investor attitudes, drivers and applications of ESG in the coming months.

More on Living Sectors and the cost of efficiency

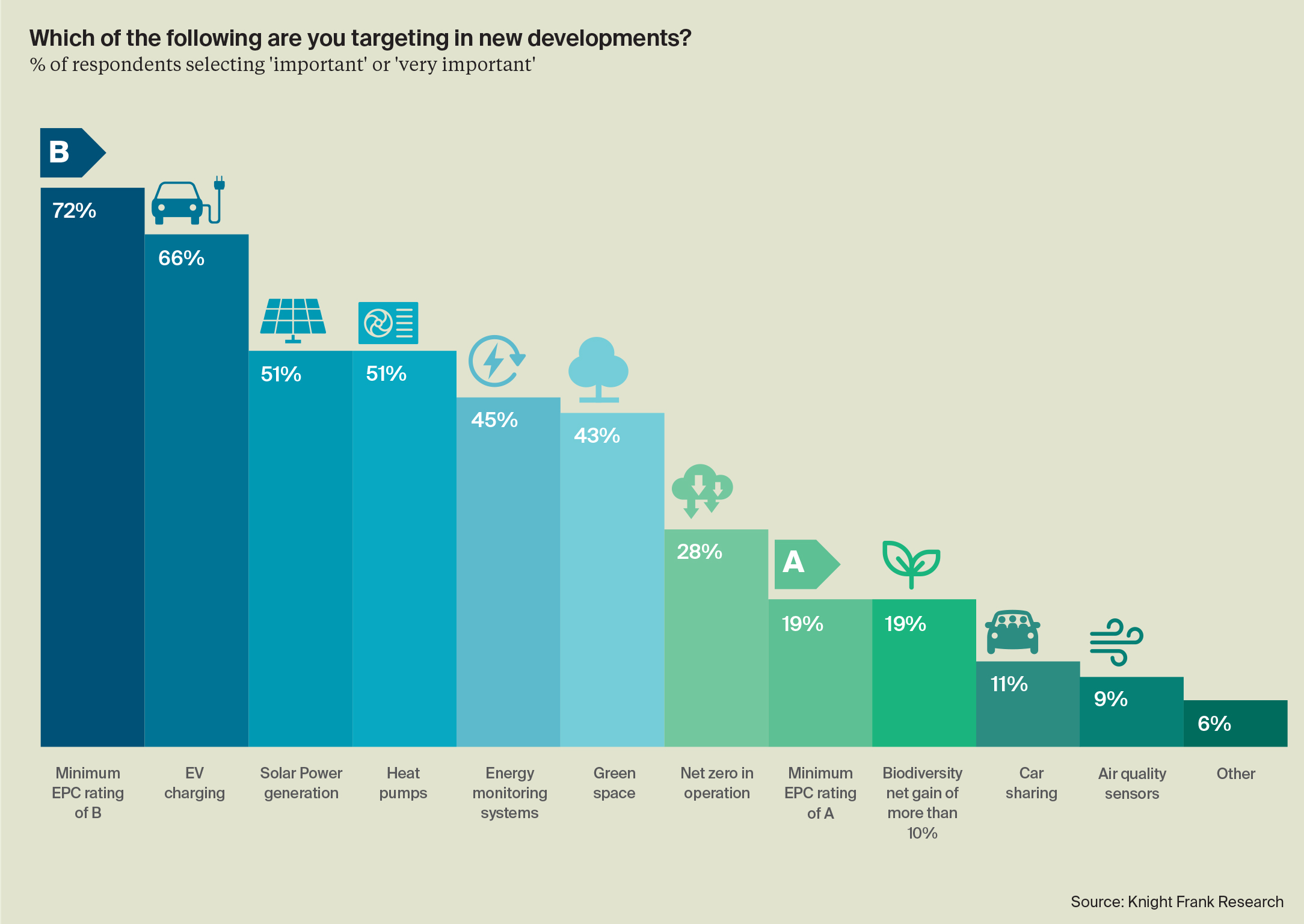

Energy Performance Certificates (EPCs) are a crucial factor for property investors, with 72% of Living Sectors investors targeting a minimum of EPC B in new development, and 19% aiming for a minimum A. This isn’t just about regulatory compliance–it’s about future-proofing assets, reducing operational costs, and remaining attractive to residents.

This ambition would put them in the top 5% of the private rented sector (PRS) for EPCs, where some 60% of homes in England & Wales currently have an EPC D-rating or below. This is particularly relevant in the context of proposed minimum energy efficiency standards, which will require every rented home in England & Wales to achieve an EPC rating of C or above by 2030. Landlords who fall below the threshold will have to make a choice between upgrading existing homes to the new standard or exiting the sector.

Upgrading these homes would cost an estimated £21.6 billion, according to our latest analysis, but the environmental payback would be significant - it could cut overall UK emissions by 1%, or the emissions for the entire residential real estate sector by 5%.

The numbers, as crunched by Johan Hagstrom of Knight Frank Analytics, compared the EPC certificates of more than 31,000 upgraded PRS homes and found that improving from EPC D to C would cost, as of January 2025, on average, £5,841 per unit—though this varies by size, age and the property’s existing efficiency rating.

We sense-checked what this would look like across the owner-occupier sector too, the estimated price tag is steeper–with an estimated £90.6 billion investment required or an average of £9,275 per property – but could reduce the UK’s emissions by 4% (20% of residential emissions). To enable widescale decarbonisation, clear and consistent government policies are needed, balancing cost, feasibility, and long-term gains.

Reforming connections in the Clean Power 30 Action Plan

The UK government’s Clean Power 30 (CP30) Action Plan aims to reform the country’s energy grid, targeting 95% renewable electricity by 2030. This initiative seeks to address major challenges, including long wait times for grid connections and infrastructure bottlenecks that have delayed property developments.

A key change is the overhaul of the connection system. Moving away from a “first come, first served” approach, the new framework will prioritise projects based on strategic needs. This reform is expected to free up 500GW of capacity, accelerating investment in renewables and electrification.

To facilitate this, new grid connection applications were temporarily paused from 29th January as the National Energy System Operator (NESO) and Ofgem restructured the process. Quotas by technology type and distribution zone are also being introduced for 2030 and 2035, as we dive into in more detail here.

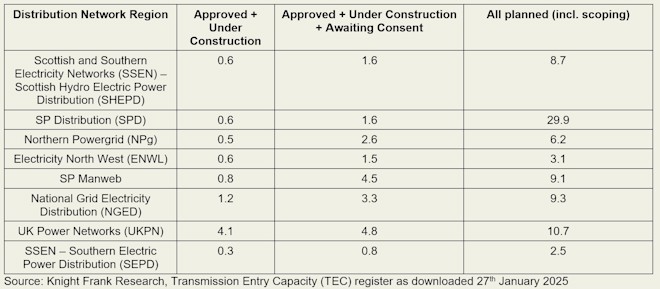

For real estate stakeholders, this shift means potential project delays or cancellations. Quotas for connections are already oversubscribed. According to NESO, some 40% of the GWs currently in the queue will, in theory, be removed. Looking at the current Transmission Entry Capacity (TEC) register and for approved or ‘under construction/commissioned’ consents, suggests that 2030 quotas have not been met – except for the UK Power Networks (UKPN) distribution and National Grid Electricity Distribution (NGED) zones where the battery energy storage systems (BESS) are currently 4x and 1.2x the respective quotas. When including those 'awaiting consents', almost all zones exceed the stated quotas for BESS (see Table below).

David Goatman and Charlie Smith have been working closely with both developers and landowners to navigate the implications. “The impact is already evident,” David says. “Some developers are facing a sharp decrease in their pipeline, largely associated with grid connection offers beyond 2030.”

“At the same time, the market has seen a surge in Ready-to-Build opportunities as developers look to exit certain projects.” Chris Jones has been helping some developers change from a BESS import/export connection into a demand import connection to power data centre development.

In response, trade group Solar Energy UK penned an open letter and NESO has since proposed a new Progression Commitment Fee to support the future connections queue. Ofgem is due to update on prioritisation and queue reform in the first half of this year. In tandem, they have ‘unleashed’ an offshore wind revolution by unlocking up to £30 billion in investment.

Table 1: Battery Energy Storage System (BESS) Capacity vs. 2030 Quotas by Distribution Zone

Ratio of listed BESS capacity (approved, under construction, or in planning) relative to the 2030 quota

Nicola Ryan's stat of the month – 17.6 GW

Despite ESG uncertainty, the UK’s clean energy push stays strong. Solar capacity hit 17.6 GW—up 7.5% (1.2 GW) in 2024—with 1.7M+ installations powering homes and businesses, according to new data from the Department of Energy Security and Net Zero (DESNZ). As grid reforms and policy shifts shake up investment, solar remains a key player in the race to 95% renewable electricity by 2030.

What else I am reading

Claire Williams Future gazes with the UK logistics sector, including considerations around energy and green leases, Labour removes environmental groups power to delay, the City of London approves new sustainability guidance, property insurance pay-outs related to weather to reach £1.2 billion, banks improving clean energy financing ratios and the UK Net Zero Council relaunched.

Sign up to Knight Frank Research.