Bringing the energy: A COP & UK Budget special

Another year, another COP and possibly the most trailed UK Budget of all time.

28 November 2025

Here, I unpick the announcements with a focus on energy and the International Energy Agency (IEA) World Energy Outlook (WEO), plus a quick look at a sector in focus: Data Centres.

The budget is done

It felt like a long-time coming. Much trailed and characterised by the accidental release from the OBR . The November Budget delivered by Chancellor Rachel Reeves offered mixed signals for the green economy, despite the fact it grew three-times the rate of the broader economy in 2024. Key measures focused on energy costs, supply, and EV adoption.

Domestic electricity prices in the UK, among the highest in the developed world, will fall as levies are removed, cutting bills by around £150 (c.16%) and easing (with other measures) inflation by 0.4% in 2026. The Warm Homes Plan gains an extra £1.5 billion, which alongside continued Boiler Upgrade Scheme have been growth (redemptions were up 42% in the year to October 2025 compared to previous 12 months).

For businesses energy prices were not directly addressed in the Budget. However, with 20–25% of industrial electricity costs are taxes and levies, recent confirmation of increased discounts for energy-intensive industries via the Network Charging Cost Compensation and consultation on the British Industrial Competitiveness Scheme is positive yet not universal. These measures, alongside the development of the corporate power purchase agreement market (such as Knight Frank’s own announcement (Clean Energy Pipeline)), aim to boost competitiveness and investment.

On the supply side, the Budget reaffirmed investment in Sizewell C, the first small modular reactor in Wales, and the National Wealth Fund, plus £14 million for low-carbon tech in Scotland. In addition there was the nod to planning reforms, and grid connections reform where the government pledged to go further with, among other things “reducing the time to power by exploring self-build for high voltage grid infrastructure and more flexible connections where possible.”

Conversely, for electrified transport the messages were mixed. The 3p pay-per-mile tax on EV drivers seems inconsistent with the zero-emissions mandate and EV grants designed to accelerate adoption. While intended to offset lost fuel duty, the timing feels counterintuitive. Battery EVs accounted for 22.4% of new car registrations YTD, according to SMMT, yet this is still short of the 28% ZEV target. Lower energy costs and renewable reforms may soften the impact.

With barriers like purchase price, range anxiety, and charging options, the announcements on grants and charging infrastructure growth provide tailwinds. Real estate owners should plan for integrated EV charging, as electrification remains inevitable.

What hasn’t been seen is clarity on minimum energy efficiency standards and retrofit incentives remains elusive, leaving uncertainty for real estate investors. A more in-depth analysis can be found here, with a broader take for commercial real estate from Knight Frank experts here and here for residential.

Power up?

In the world of sustainability, outside of UK politics, COP is often a key feature. This year’s COP30 was 10 years since the landmark Paris Agreement but closed with little fanfare, marked by notable absences and a shift in the climate narrative. The final text reflects this: despite earlier pledges (Dubai) to transition away from fossil fuels and strong support during negotiations (more than 80 nations and ‘scores of leading corporates and business groups representing more than 100,000 firms’ (BusinessGreen)), a roadmap on how was absent from the agreed text.

So how is the energy transition tracking? We look at the IEA’s World Energy Outlook for this and how it may evolve under three scenarios which represent possible trajectories not forecasts:

- current policies (a cautious perspective) - CPS,

- stated policies (includes those put forward not yet adopted) - STEPS, and

- a net-zero pathway.

The key takeaways for me:

- We need more energy: Total energy demand is projected to increase by 11–15% by 2035 (under CPS and STEPS) and by 19–32% by 2050. However, the shift towards electrification puts electricity demand up ~40%. This highlights the efficiency gains from electrification with electricity demand growing twice as fast as overall energy demand in the past decade, a trend set to continue

- Expectations for demand are rising year-on-year: Driven by requirements for air conditioning, advanced manufacturing, e-mobility, digital economy, AI, and electrified heating. The STEPS scenarios show that expected 2035 and 2050 demand has increased 1% compared to last year.

Renewables with be critical to meet rising demand: In STEPS, renewables meet electricity growth; in CPS, shortfalls occur in the US but not in Europe or China. - Renewables now supply one-third of electricity (up from one-fifth a decade ago) and are projected to reach 50–55% by 2035.

- Solar is driving this: Solar is now the cheapest energy source to deploy to meet the growing demand, and one of the fastest as Semafor discuss. Analysts suggest STEPS underestimates deployment, especially in developing nations

- Momentum building: 2025 saw record renewable capacity added and, for the first time, exceeded coal generation, according to energy think thank Ember.

- Challenges remain: Grid flexibility and management is critical to avoid growing curtailment risk (Bloomberg) (and rising negative pricing phenomenon with some European countries logging >500 hours in 2025, SolarVision). Solutions include batteries, digital twins (The Economist), nuclear growth, and diversified supply chains, the IEA notes “One country leads refining for 19 of 20 strategic minerals.”

Despite COP30’s diluted final pledge, many nations remain committed. The pre-COP “Belem 4x” pledge to quadruple sustainable fuel production (supported by another IEA report), a “coalition of the willing” (The Guardian) to develop a roadmap, and a collection of countries including the UK, committing to the Global Clean Power Alliance Supply Chain Mission.

AI and data centres and sustainability

The world generates over 400 million terabytes of data daily, driving what the IEA calls “explosive growth in electricity demand for data centres and AI.” While these account for under 10% of global electricity growth, the share is higher in the US due to the concentration of data centres. This rapid rise in demand has not been matched by an equal uplift in supply, pushing energy prices higher (see this piece from Bloomberg).

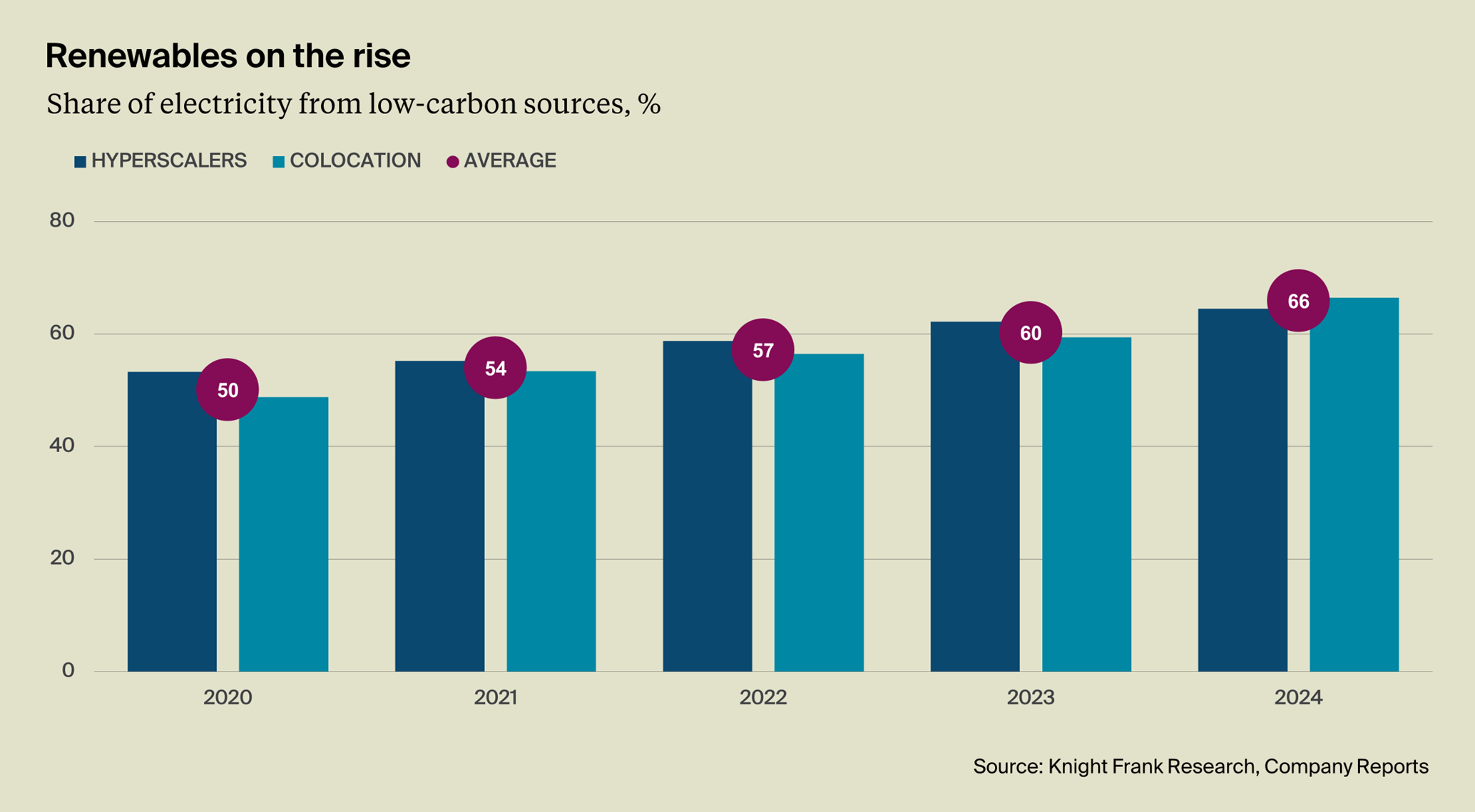

There is also the broader conversation around data centres, which are often cast as fossil-fuel intensive. However, the sector is rising to the challenge. Where capacity nearly doubled from 25.6GW to 50GW between 2020 and 2024, Scope 1 and 2 emissions rose only 24%, showing carbon intensity improvements, according to Knight Frank’s recently released Data Centres: Taking Stock of Sustainability report.

Supporting this is a greater use of renewables and efficiency gains. The report highlights how low-carbon sources supplied 66% of sector electricity in 2024 (up from 50% in 2020, see figure below). This is being delivered through PPAs and co-location with renewables, now standard practice, as highlighted in our 2025 Global Data Centres Report, alongside innovations like microgrids, modular reactors, and hydrogen fuel cells. Efficiency metrics also improved: annualised average Power Usage Effectiveness (PUE) fell from 1.39 to 1.33. Advances in cooling, AI-driven load management, and modular design underpin these gains.

Looking at the wider narrative, some analysts suggest that AI could deliver net emissions reductions. Research from the Grantham Research Institute and Systemiq on Climate Change and the Environment models how this could be the case through five impact areas: transforming systems, boosting resource efficiency, enabling behavioural change, modelling climate, and managing resilience.

However, the challenges remain: grid bottlenecks, water stress in key markets, and the need for next-gen cooling technologies. The sector is required to balance growth with sustainability while enabling the digital economy and broader decarbonisation.

Resilience and adaptation

The other key focus in Belem was physical climate resilience and adaptation, the final text agreed to triple adaptation finance by 2035. For the energy sector this is becoming a critical focus. Whilst reliable supply needs to expand, the rising frequency and intensity of weather incidents bring new risks to existing and new infrastructure. A new IEA dataset shows “that recent annual operational disruptions to critical energy infrastructure affected energy supplies to more than 200 million households around the world."

Closer to home, in October the Royal Meteorological Society (RMS) released its State of the Climate for the UK Energy Sector 2024-25 warning that weather events are having an “increasingly significant” impact on electricity generation, demand, and infrastructure. A key consideration in overall system readiness and resilience is required. In recognition of this, DESNZ announced an Energy Resilience Strategy to be published in 2026.

Stat of the month - US$54.4 billion

According to CDP, companies that implemented emission reduction initiatives in 2024 collectively reported $54.4 billion in annual cost savings, primarily from energy efficiency and low-carbon generation.

What else I am reading

Knight Frank’s UK ESG Report 2025, The RICS Sustainability Report (see my thoughts here), The seventh biennial Global Sustainable Investment Review from the Global Sustainable Investment Alliance, UK solar rooftop installations hit record high, according to MCS, the government announced over 250 school set to receive solar panels (BusinessGreen), and the 23 that already have as well as air-to-air heat pump grants to allow for cooling tech as well as heating.

Sign up to Knight Frank Research.