Are the risk-free rates still risk free?

The ‘risk-free rate’ no longer feels as secure as it once did.

The ‘risk-free rate’ no longer feels as secure as it once did.

Rising fiscal deficits, political uncertainty and higher inflation in many European markets have dented confidence in government bonds, with investors now demanding greater compensation to hold government debt. In contrast, commercial real estate has delivered steadier, more resilient returns over the past decade, and with fundamentals improving and early signs of recovery emerging, its appeal is strengthening further.

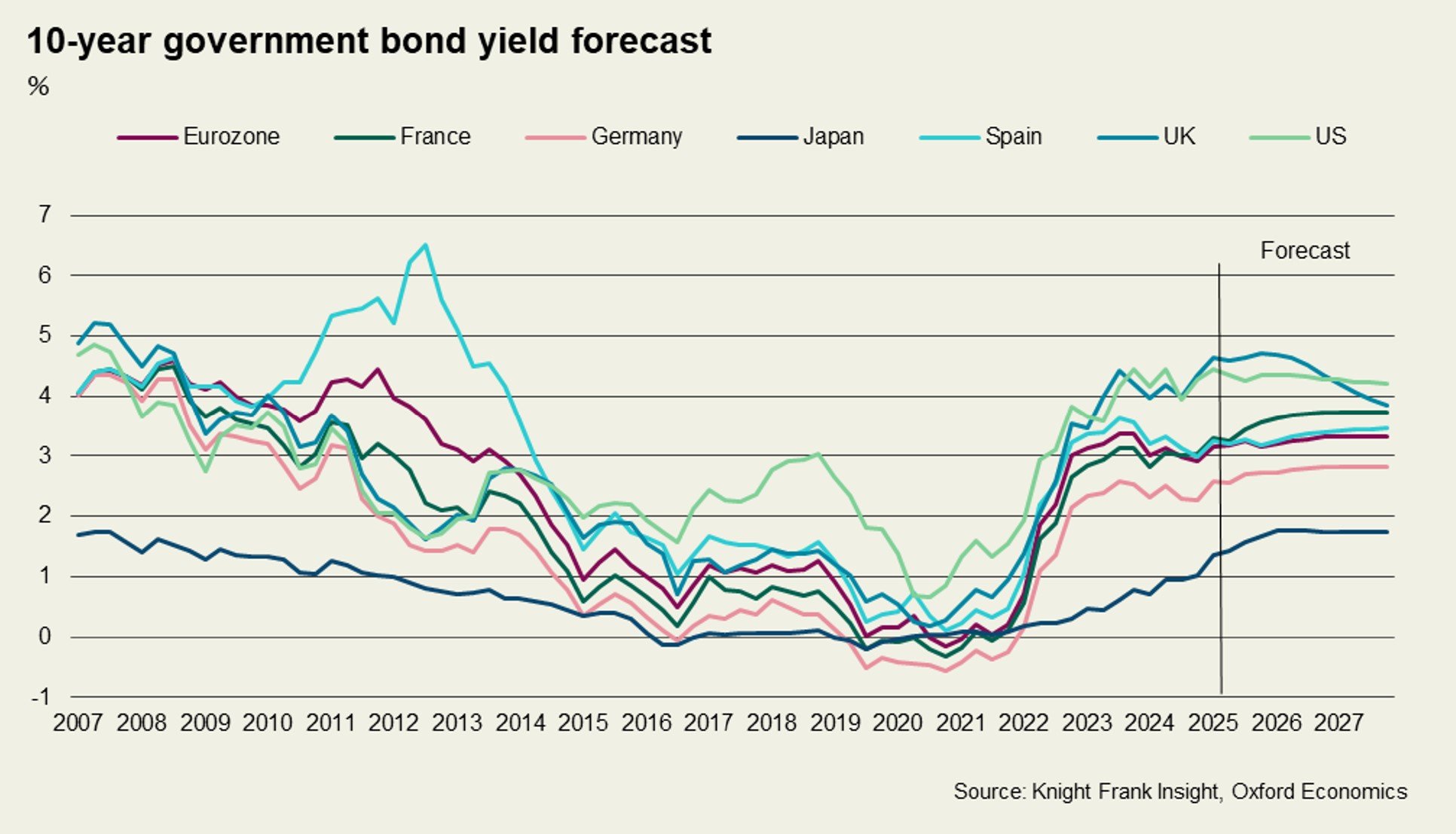

Recent market conditions have shown that government bonds are not immune to volatility. The French 10-year government bond yield this year hit its highest level since 2011 amid political instability, widening the spread with the German Bund.

Oxford Economics forecasts suggest that by end-2027, yields on 10-year government bonds in major Eurozone economies could rise further, while UK gilt yields may decline to just under 4.0%, still above the Eurozone average. For long-term investors, this challenges the perception of a truly ‘risk-free’ asset: the guarantee may apply to repayment at maturity, but not to price stability along the way.

Over the past decade (Q2 2015-Q2 2025), European commercial real estate (Europe all sector) has delivered resilient returns, achieving a 6.37% compound annual growth rate (CAGR). This significantly outperforms Eurozone Government Bonds (1.5%) and Eurozone REITs (3.07%).

In a market where the traditional ‘risk-free’ status of bonds is increasingly in question, these qualities highlight the growing appeal of European commercial real estate - combining durable income, inflation resilience, and low correlation to broader markets, it offers a reliable source of stability and long-term value.

Although less liquid than government bonds, it enhances portfolio diversification and serves as a stabilising force within a balanced investment strategy. Prime assets in particular provide:

As such, we expect demand for real estate to continue to accelerate in 2026.

Explore more content from European Outlook

Be the first to receive global insights and our latest properties.

Sorry!

An unexpected error has occurred.

Please try again later.