Trump 2.0 and ESG in property, Living Sectors investor sentiment and COP time

This month we look at what a Trump presidency may mean for ESG and property more broadly. We’ll also cover relevant news from COP and discuss some emerging trends for ESG in Europe.

14 February 2025

Trump and ESG

It was billed as a 'knife edge' election, but the reality was a decisive victory for Donald Trump, securing him a return to office for a second term. After four years of Democrat leadership and one of the biggest climate policies ever in the IRA (Inflation Reduction Act), what does Trump mean for sustainability and property?

Trump made no secret on his campaign of his view that “climate change is a hoax” and has promised to end what he calls Washington’s “green new scam”. While that suggests sustainability will be low on policy priorities, as Bloomberg noted "a victorious Trump can’t fully halt the country’s green shift," and "campaign rhetoric aside, it’s clear that the sweeping 2022 climate law known as the Inflation Reduction Act has been built to withstand political attacks."

It's worth noting that 90% of capital unlocked by the IRA has flowed into Republican congressional districts and they may be reluctant to forgo these - even in a Republican controlled House and Senate. Yet the shape of incentives and subsidies may shift - we will watch this space and any uncertainty could dent immediate investment.

Investors themselves have also been one of the driving forces behind greening buildings in recent years, amid a desire to future-proof assets for the long term, and that is unlikely to change. In previous newsletters we noted a Bloomberg article which highlighted the move of investors to green buildings around the world, with an ex-Managing Director at Goldman Sachs betting his career on it. The article mentions that despite some anti-ESG rhetoric, “investors in the US are actually showing more willingness to allocate capital to greening buildings than their counterparts in Europe”.

Time will tell but market incentives may still be futureproofing in the long term - even if it's not specified as ESG or sustainability.

In the 2024 outlook newsletter I also noted that during Trump’s previous tenure, despite the climate rhetoric, the private sector drove the agenda forward. The Taskforce for Climate-related Financial Disclosure launched in 2017 and saw supporters rise to 1,000 by 2020 – it reached almost 5,000 before disbanding at COP28 due to their remit being fulfilled. And this has propelled greater action, which is unlikely to abate due to the global push for transparency and reporting.

ESG driving European real estate

European real estate owners are concerned about the challenge that ESG poses for the sector. The 2025 Emerging Trends in Real Estate Europe report by ULI and PwC found that ESG is one of the most significant challenges for the sector. Some 70% of the 1,100+ respondents were concerned about environmental issues, with 72% flagging this as an issue for the next five years. Many admitted that they were struggling to keep competing environmental concerns at the top of the agenda.

Overall asset obsolescence concerns are on the rise with 56% citing it as an issue, up from 38% in 2023, according to the ULI/PwC survey. Increased regulation is the top issue with 74% concerned, up from 51% in 2023 – the two are inherently linked as we point to in Part 1. Yet, it is also an opportunity to create value, drive performance and decarbonise as we explore in Part 2. For more detail on the trends, read the report here.

For the living sectors, the greatest driver is investors. Some 69% of respondents to our recently released European Living Sectors Investor Survey, stated that investors are ‘important’ or ‘very important’ in dictating the approach to ESG. That’s more influence than regulatory change (65%), or tenants (52%). Accordingly, 38% are looking to include solar power in new developments with 31% targeting a minimum EPC A.

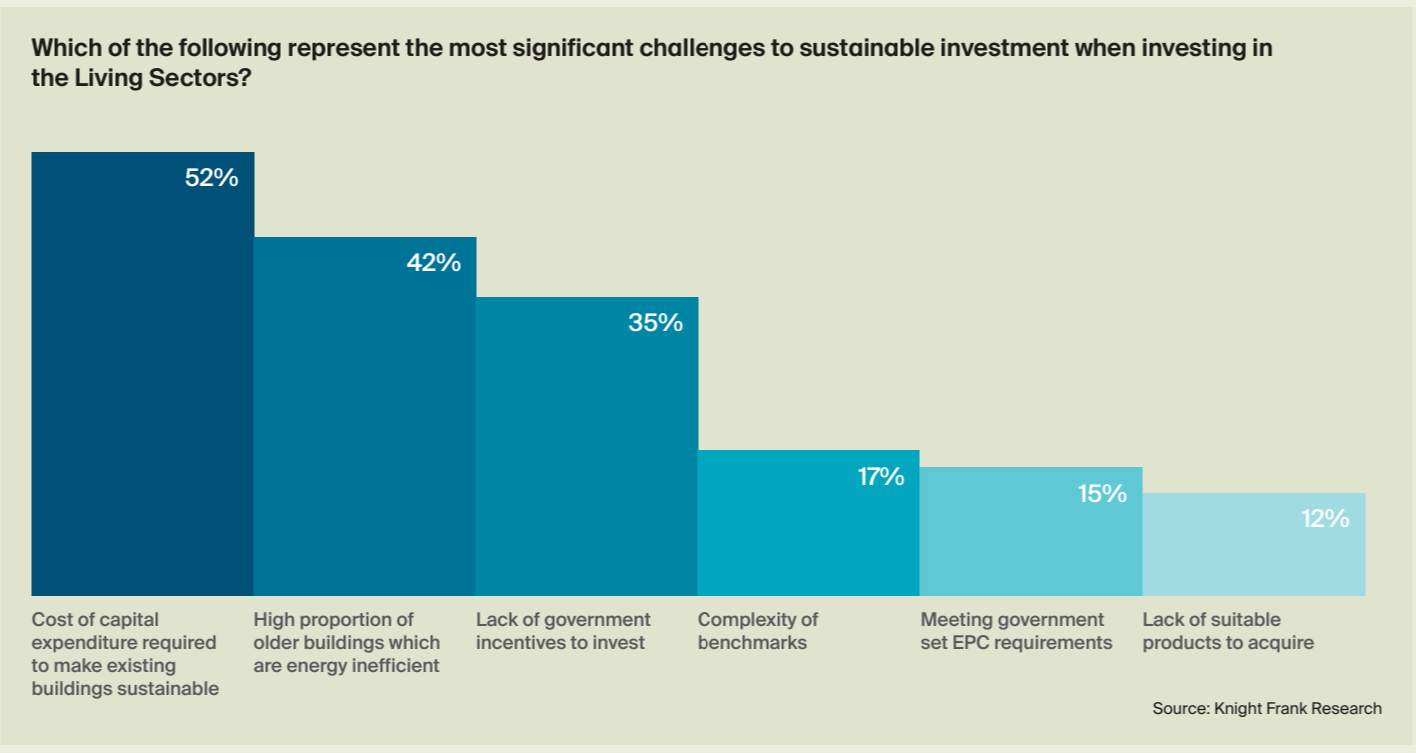

Financial barriers to efficiency

Despite the drive, there remain challenges. When asked what represented the most significant challenges to sustainable investment in the Living Sectors, more than half (52%) highlighted the cost of capital required to make existing buildings sustainable. Related to that, some 42% of respondents flagged the high proportion of older buildings that are energy inefficient.

This rings true with the ULI/PwC report where overall capex requirements were cited as a top concern by 69%. But it's not just the cost of improving building efficiency and performance. There is a cost of inaction for building resilience. As discussed in Part 1 of our Meeting the Commercial Retrofit Challenge report, the physical risks to buildings can increase day to day operational expenditure with almost two-thirds of respondents to the ULI/PWC survey expecting an increase in insurance costs over the next five years.

Could a new financing model be implemented to move this forward? In the UK, the Green Finance Institute, working in partnership with Lloyds Banking Group and NatWest Group, this month published a report outlining the potential for a fresh green finance mechanism – property-linked finance. The report notes an estimated investment of £360bn is needed to decarbonise the UK’s commercial and residential buildings by 2050 – an investment that cannot be met by the public purse alone.

Let's COP to it

The past month has seen two COPs - COP16 the biannual Biodiversity summit in Columbia and its big sister, COP29, in Baku. COP16 saw the International Advisory Panel on Biodiversity Credits, established by the UK and France, launch a framework for “high-integrity” biodiversity credit markets. The framework ruled out the possibility of a global offsetting exchange, meaning that conservation efforts must directly address and restore biodiversity impacts in the areas where they occur.

Much discussion in COP16 focused around bringing private finance into nature. The idea of financing nature is something we have spoken about previously in the context of UHNWIs looking to invest in nature and nature-based solutions (most recently here and here) and also for landowners. A clearer framework could help to develop this market further, alongside the uptake in the Taskforce for Nature Related Financial Disclosures.

In an early success for COP29, nations agreed rules governing international carbon credit quality standards which may lead to a UN-backed global carbon market. The full comments from Yalchin Rafiyev, COP29 Lead Negotiator, are here. Arguably, much has centred on how the US election results will influence the global cooperation and movement towards the Paris goals - we will look more at the outcome of COP29 in December.

18 out of 20 - Nicola Ryan's stat of the month

18 of Europe's 20 largest banks are not on track to meet the International Energy Agency's recommended $10 to $1 ratio of green investment to fossil fuel investment by 2030, according to ShareAction's report Mind the Strategy Gap. With rising stakeholder pressure, we could see this gap turn into an increase in sustainable funding for commercial real estate.

What else I am reading

Making green lease clauses standard and remove 'green' wording and Keir Starmer pledges to reduce UK emissions by 81% by 2035 from 1990 baseline (up from 78% previously targeted).

Sign up to Knight Frank Research.