Obsolescence reframed as an opportunity

This is a bonus newsletter, departing from the usual monthly cadence, to mark the release of the second in our three-part series, Meeting the Commercial Retrofit Challenge. In addition, we would like to welcome you to take part in our annual ESG survey.

25 October 2024

Bigger picture benefits

The risk of building obsolescence is accelerating. As a result, the need to define asset and portfolio strategies, including decarbonisation and amenity plans, is growing. This needs to be coupled with a thorough understanding of economic and location factors (see our UK Cities DNA research) to assess obsolescence risks beyond sustainability.

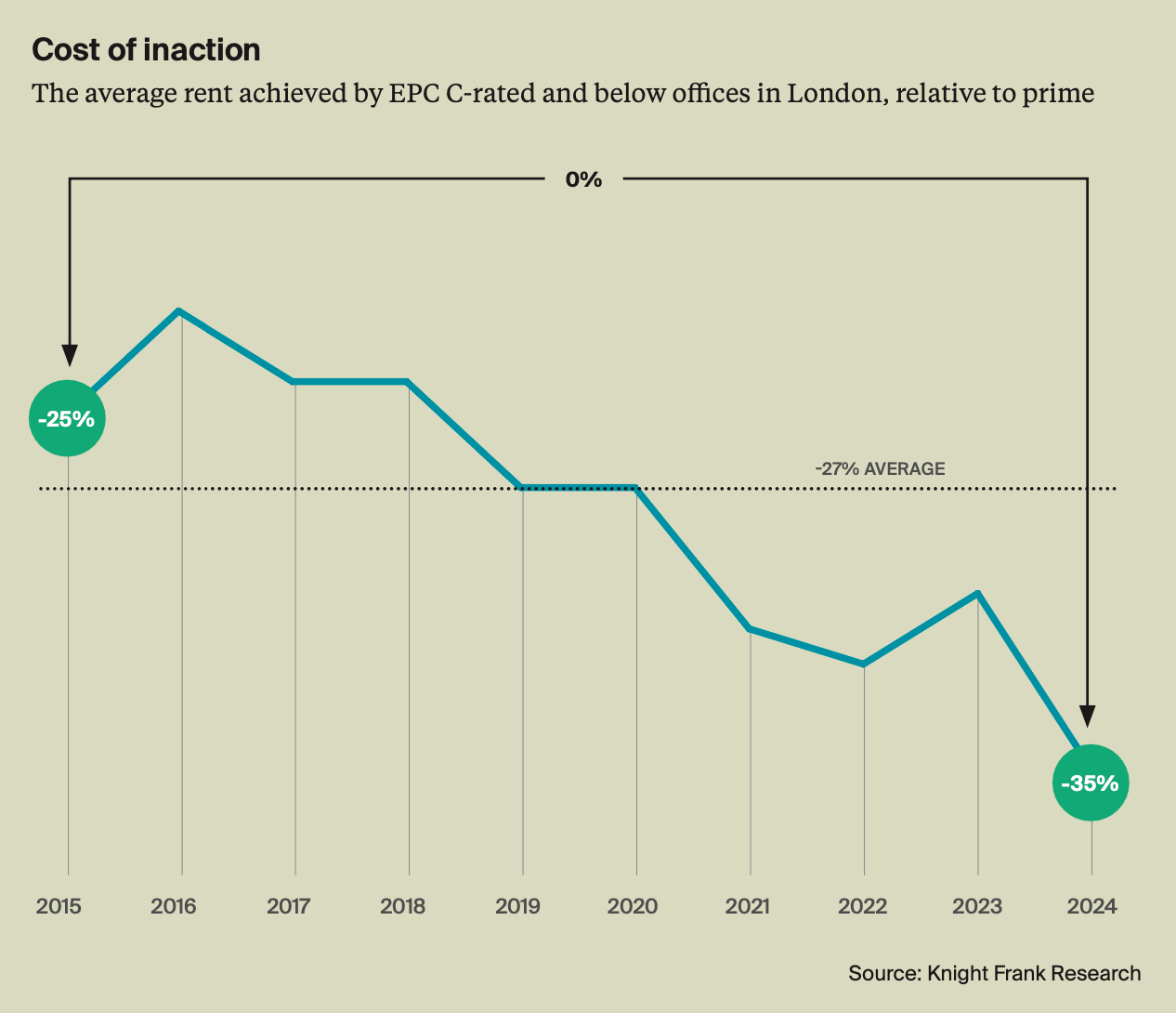

Whilst it may seem obvious that improving a building will lead to higher rents, its important to also weigh it against the cost of inaction. The gap in rents achieved relative to prime in EPC C-rated and below offices is widening and, most recently, is over 30% (see below). Whilst it must be noted that prime rental levels include new-builds, there is a clear bifurcation in the market but retrofitting and refurbishing can look to close this.

We have crunched the numbers across 130 retrofitted and refurbished offices which have moved from an EPC C-rating and below to an EPC B-rating and above across the UK and analysed rents pre- and post-renovation. On average, the retrofitted and refurbished offices saw the rental gap relative to prime close by 18%. This relative uplift varied by location, level of intervention, the number of pre-and post-leases, and market-specific factors (such as supply). A detailed understanding of these nuances, including market context and future pipeline and occupier requirements, is critical to assessing value.

The type of amenity, not how many, appears to influence the relative rental uplift. Outdoor space offers the greatest differential, our sample indicates, with 70% of those with an above average uplift having such amenities, compared to around 40% of those with below average. In Part 1, we highlighted the prevalence of outdoor amenities in buildings with BREEAM Outstanding certifications, which may be linked. Knowing which amenities may yield the greatest rental effect will enable assessment of the net lettable area vs. amenity consideration, as well as certification strategies.

But rent is a small piece of the puzzle. There are exit yields, where higher sustainability credentials can lead to longer lease terms and lower void periods, all potentially lowering the risk premium. In London, for example, the offices that were retrofitted and refurbished between 2020 and 2024 and achieved BREEAM Outstanding or Excellent certification, or an EPC A-rating, were pre-let six months before completion on average.

Checks and balances

The cost to upgrade will depend on numerous factors: location, size, interventions required, and amenity provision, and asset-specific assessment are all critical. Having an indication of the variance and baseline will help to narrow potential strategies.

To illustrate potential levels, we present hypotheticals in the report. For those doing the future potential minimum to merely achieve an EPC B rating, our modelled asset-level scenarios of a current EPC D-rated office building in London applying the four most common improvements put this cost at £113 psf. When including a very high level of amenity, such as terraces and fitness/wellbeing facilities, this rises to an average of £268 psf, see the report for more detail on this scenario.

The cost of implementing change needs to be weighed up against the cost of inaction and not just in rent as mentioned earlier. New research from the GIC finds that physical risks from climate change could cost the real estate industry well over $500 billion by 2050.

We highlight the physical risks as a channel of obsolescence with consequences not only for the functionality of an asset but also for insurance costs and availability. The resilience of buildings has been highlighted by an increase in extreme weather over the past few years – notably in the past month in the US with Hurricane Helen causing an estimated $30.5 billion to $47.5 billion in damage (about a third insured), and Milton, shortly afterwards, causing another $30 billion to $50 billion in insured losses. We highlighted the trend as one to watch for 2024, and these serve as reminders to incorporate resilience into any asset plan.

A one-size-fits-all approach is unworkable. Property owners and investors must conduct detailed, asset-level analyses, considering local market conditions (including the locational DNA to ensure long-term viability and reduce oversupply risk), occupier demands, variations in costs and benefits and how each strategy will vary within these elements. It is important to assess all options, including the possible avenues and level of renovation, to find the optimal solution. There will be more on this in Part 3 of the series and in the UK Cities DNA piece.

Ultimately, obsolescence needs to be thought of as an opportunity to decarbonise real estate and drive value and performance.

Is BNG a silver bullet?

As COP16, the biannual Biodiversity Summit, approaches in Columbia from 1 November – the climate sister COP29 in Azerbaijan comes straight after – we take a look at how the UK's Biodiversity Net Gain (BNG) legal requirement is shaping up after half a year in force. In the first five months, from 12 February 2024 to the end of June, Patrick Dillon, a senior analyst in Knight Frank's Research Analytics team, analysed 1,300 planning applications across 29 LPAs. The research found that less than a fifth triggered a BNG assessment, with less than half of those identifying a need for BNG.

Overall, the investigation discovered that the total demand was 118 units, an average of just over 4 per local planning authority (LPA). Suppose we were to scale to all LPAs in England; that would be c.3,100 BNG units required annually. However, not all will require off-site or statutory options.

According to the Knight Frank quarterly survey of volume and SME housebuilders, on-site is the primary method for meeting BNG requirements. Of those respondents who stated how they would satisfy the BNG requirement, 76% can meet the need on-site, with 15% seeking off-site options and the remainder going to statutory credits.

Thus far, the demand for BNG is limited, this article offers some views on why, yet in The Rural Report's latest edition, the survey found that over 20% of respondents were looking to create BNG or other environmental credits. "From a landowner's perspective, there is more of a cautious approach to setting up or investing in habitat banks than earlier in the year. We expect this to increase as confidence grows in the policy, development applications pick up, and the Government's planning reform proposals become clearer," notes James Shepherd, Partner in Knight Frank's Rural Consultancy.

With the new government pledge to build 1.5 million homes in the next five years, this could grow. But, for landowners, it is important, as cited in The Rural Report, to 'think before you leap'. In particular, understand the local market dynamics and what could happen, but also assess all other options available – be that carbon or payments from the Sustainable Farming Incentive.

What else I am reading

GRESB results with 65% having net zero targets and 29% incorporating embodied carbon, City of London Corporation cuts emissions by two-thirds, Footasylum secures Sustainability Improvement Loan, which, in its TCFD sustainability documentation, has previously focused on retrofitting retail stores with LED lighting and investing in sustainable logistics/warehousing, have global emissions peaked?

Sign up to Knight Frank Research.