What impact will Covid-19 have on prime residential markets globally?

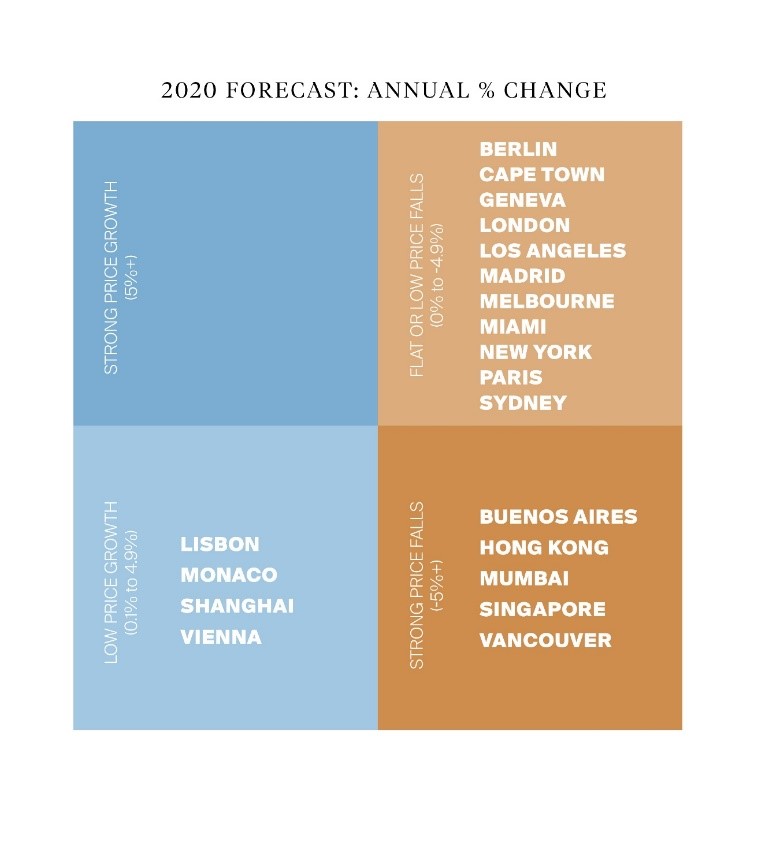

Lisbon, Monaco, Vienna and Shanghai are the only four major prime residential markets set to see price growth throughout the remainder of 2020 as the impact of Covid-19 takes its toll on luxury residential property markets around the world.

4 minutes to read

Analysis by Knight Frank of 20 cities globally highlights the direction of travel for prime prices in 2020 and 2021 based on projections for demand and supply, the impact of Covid-19 in the different markets and the varying government stimulus measures announced.

The scale of global economic uncertainty is unprecedented and therefore putting an exact figure on forecasts is challenging. As a result, Knight Frank has placed the 20 cities analysed into four price bands including markets that will see: strong price growth (+5% or more), low price growth (0% to 5%), flat or low price falls (0% to -5%) and strong price falls (-5% or less).

At the start of the year, Knight Frank predicted a number of markets around the world would see healthy prime price growth. Paris led Knight Frank’s Prime Global Forecast for 2020 with expected growth of 7%, Miami and Berlin were set to see rises of 5% and prime price growth was anticipated in Geneva and Sydney at 4% respectively.

According to Liam Bailey, global head of research at Knight Frank: “There were positive signs in several markets globally that prime prices would rise throughout 2020 but unsurprisingly, Covid-19 has put a halt to that. Of the 20 cities Knight Frank has analysed, 16 of these will see prime price declines in 2020, with only a handful avoiding a fall into negative territory – either because of historic supply shortages or because transactions were able to continue during lockdown and these measures are already being eased.”

Of the cities set to see a decline in prime prices, those likely to be hit hardest are either emerging markets or cities that were already seeing weak price growth at the end of 2019. Singapore is one exception; Knight Frank predicted prime prices would rise by 3% throughout 2020 but the fall-out of Covid-19 and the length of time the Singapore market has been affected, changes the prediction to a decline of up to 5%.

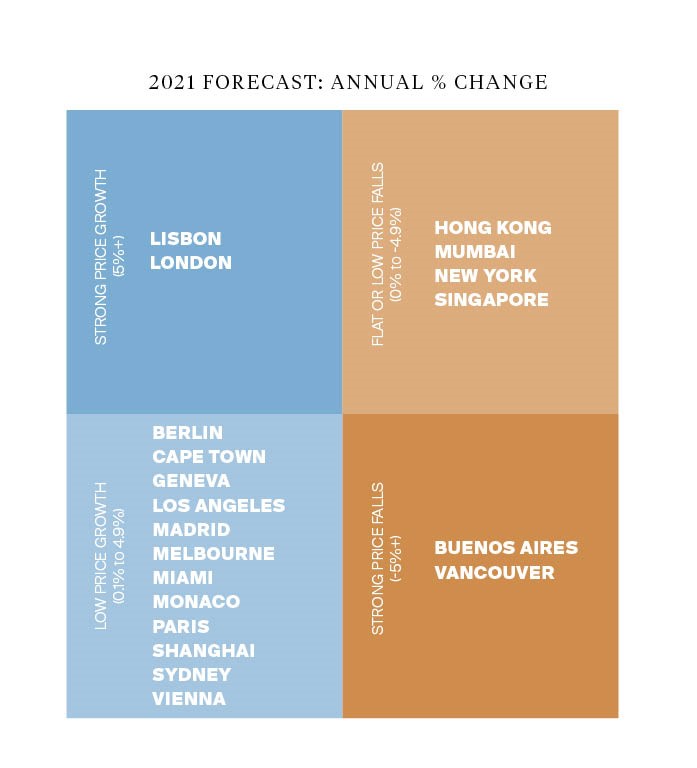

Looking ahead to 2021, we expect to see a slight rebound in most markets.

London and Lisbon sit out in front in 2021, with forecast growth above 5%. In Lisbon, Portugal’s handling of the crisis combined with strengthening demand and limited prime supply, will underpin price growth. A number of other European markets such as Berlin and Madrid are also expected to rebound well.

In London’s case, the political certainty provided by last December’s general election boosted housing market confidence during January and February. With prices in some areas down as much as 25% over the last five years, we expect a sharp uptick in 2021.”

Of the three US cities tracked, Miami is expected to perform strongest throughout 2021. The market here was already strengthening in 2019; in part due to the State and Local Tax (SALT) deduction, which heightened Florida’s appeal but, the Covid-19 crisis, has also underlined Miami’s lifestyle advantage for many living in high-density markets.

Los Angeles’ distinct lack of new prime supply should cushion price falls in this market in 2021, whilst in New York, much like London, prime prices have declined in recent years but transactions were beginning to pick-up in early 2020. There is evidence of safe haven flows from emerging markets in the last few weeks into New York and the volatility of equity markets is prompting some high-net-worth-individuals (HNWIs) to rebalance their investment portfolios giving greater weight to property assets.

Whilst a degree of resilience is expected in terms of prime prices in some markets, sales volumes in all markets have dropped significantly in Q2 2020, although the majority of these markets expect the slowdown to be short-lived with traction expected to be gained in the second half of 2020.

Trends to monitor

With Covid-19 creating a ‘new normal’, Knight Frank has outlined several future trends to look out for across prime property markets around the world:

EMEA & US:

- With air travel paused, we may see buyers prioritise second home markets closer to home that can be reached by road or rail

- With interest rates set to remain at historic lows in most advanced economies, some HNWIs will look to take advantage by refinancing or releasing equity in order to buy elsewhere

- The dollar remains strong and this provides both US but crucially, UAE, HK and many emerging market buyers (whose currency is pegged to the USD) with an advantage in many markets

- With the holiday rental market impacted, a number of landlords are transitioning to the long-term rental market – this will suit city destinations where there is domestic demand rather than more remote second home markets reliant on overseas tourism

- Property will continue to appeal as a long-term investment and store of capital

APAC:

- Markets starting to exit lockdown restrictions (China, South Korea, Vietnam, New Zealand, Australia)

- Sales volumes to rebound but still below long-term average

- Economic fallout to weigh on markets

- Stimulus measures and accommodative monetary policy to assist

- Cooling measures could be eased in many markets

Subscribe to our daily research update or listen to our latest Intelligence talks podcast