Sticky inflation, family offices and shrinking inventory levels

Plus, China’s faltering recovery

4 minutes to read

Inflation

Inflation may be heading in the right direction but it’s sticky, and causing central bankers, and high street banks, a headache.

Australia and Canada surprised markets by hiking rates last week after each paused earlier in the year.

The UK has seen numerous mortgages wiped from the market as gilt yields have risen and lenders absorb worse-than-expected inflation forecasts.

Surprisingly, the Eurozone is a rare bright spot. Spain, Portugal and France posted much-reduced CPI figures of 2.9%, 3.9% and 5.1% respectively in May 2023.

That said, the European Central Bank’s President Lagarde has reiterated, “we are not pausing” and “we know that we have more ground to cover.”

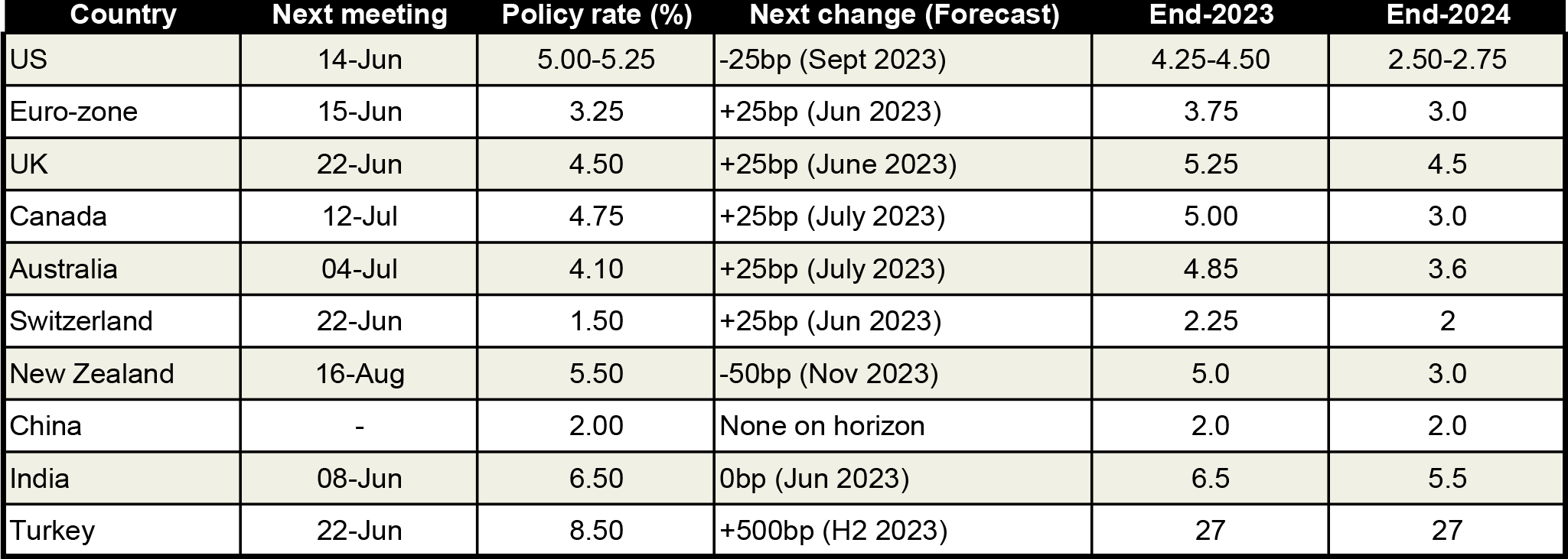

The chart below sets out Capital Economics view of where rates are forecast to sit at the end of 2023 and 2024.

Two camps are emerging. New Zealand’s Central Bank has signalled it has reached its peak; the US could be next, although debate rages on the direction the Federal Reserve will take today.

The second camp is comprised of the Eurozone, the UK, Australia and Switzerland, all of which have further to run.

It’s interesting to note that when Canada and Australia paused earlier this year, both housing markets saw activity and prices strengthen, suggesting a degree of pent-up demand is building.

Once we see start to see major world economies move in different directions, expect greater volatility in the currency markets, presenting opportunities for some cross-border investors.

Family offices

From Singapore to Hong Kong and Dubai to Monaco, authorities are going out of their way to attract family offices and their associated wealth.

Family offices are estimated to hold US$4 trillion globally, larger than the entire hedge fund industry, according to Campden Wealth.

But it’s an opaque world with few family offices obliged to disclose the extent of their wealth. What we do know, is that it’s big business.

Research by KPMG reveals around 40% of CIOs for US family offices are paid more than US$1 million, while 17% of those in Asia earn more than SG$1 million ($740,000), and 6% in Europe make at least €1 million ($1.1 million).

The industry is set to expand further. New data from Knight Frank’s Wealth Populations Report confirms the world’s billionaire population is forecast to rise by 28% between 2022 and 2027, taking the total tally to 3,372.

Although Africa is set to see the biggest percentage increase in the next five years, numbers are rising from a low base. Instead, Asia-Pacific is the region to watch as its billionaire population swells from 999 to 1,514 by 2027.

Supply

Tight supply is supporting house prices; it’s a key trend we highlighted in The Wealth Report 2023, with Los Angeles, Singapore, London, Paris and Madrid experiencing such constraints.

However, although home sales may have tumbled across global markets, house prices are proving relatively resilient.

In the US, house prices have fallen just 3.6% from their peak, in the UK they’re down 2.5% on average and in Australia, where rates have risen 12 times to 4.1%, they’re still only down 5.0%.

Limited stock, both fewer new-build units due to slower construction rates, and constrained inventory of existing stock, are mitigating price falls.

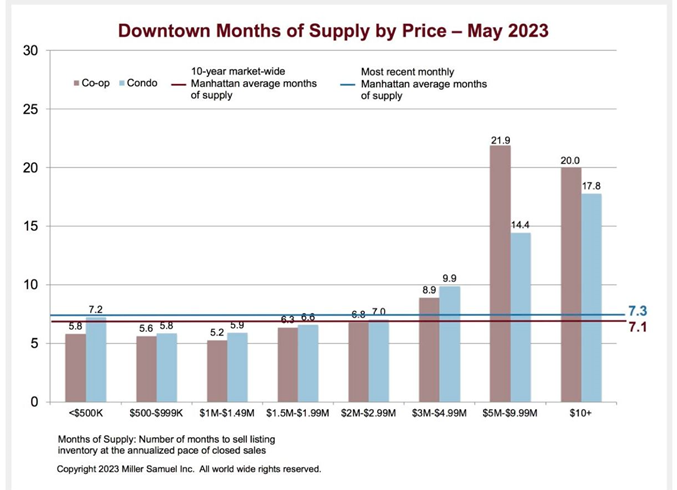

Two charts on this topic caught my eye this week. The first from my colleague Jonathan Miller who produces reports for Knight Frank’s partners in the US, Douglas Elliman.

Jonathan’s data reveals that the supply of properties priced below US$2 million in Downtown Manhattan now sits below the 10-year average.

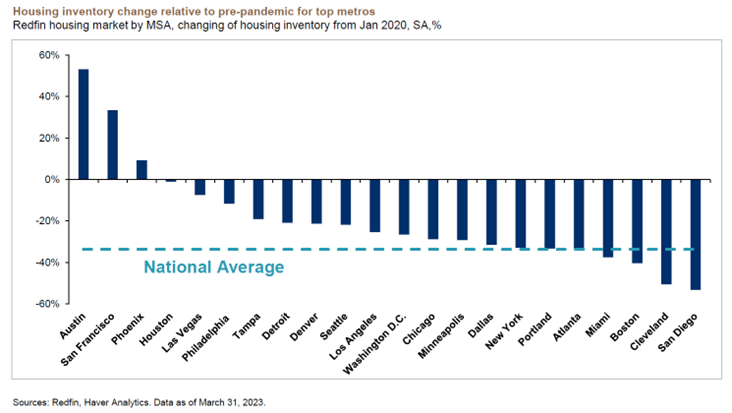

But it’s not a trend exclusive to New York’s luxury segment. Inventory levels across most US cities now sit well below their pre-pandemic levels.

Whilst sales may weaken further as higher mortgage rates pinch, prices may not register the declines many envisaged at the start of the year.

Knight Frank will be releasing its latest Prime Global City Forecast next month, setting out our research network’s view of where prime prices are headed, sign up here to get your copy.

China

China’s recovery is faltering. As the country reopened post-Covid-19, the expected jump in economic activity has failed to materialise, with potential repercussions for global markets and consumers.

Whilst the rest of the world may be fighting high inflation, China has the opposite problem. Consumer prices rose by only 0.2% year-on-year in May and policymakers are now mulling over a cut in interest rates.

Prices across the Chinese mainland increased for the fourth consecutive month in April, up 0.4% month-on-month but down 0.2% on an annual basis, according to the National Bureau of Statistics.

Affordability is not the challenge for China’s policymakers, prices are not detached from rents or incomes, instead concerns relate to indebted developers and households, as well as oversupply in some cities.

Sign up here to receive the latest instalment of the Global House Price Index to gauge how China’s slowdown compares to 55 other countries and territories.

In other news…

UK expats hit by mortgage drought (FT), the rich world is in the middle of an immigration boom (The Economist) and why a golden age of residence permit investors is coming to an end (React)