UK Logistics Market Update - May 2026

Navigating Volatility: Cost Pressures, Pricing Shifts and Changing Demand Patterns

20 May 2026

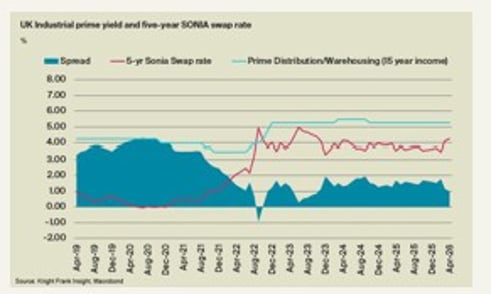

Rising alternative asset yields and swap rates are reshaping pricing

Since late February, the Iran war has pushed up energy prices, interest rate expectations and alternative asset yields, as investors assess the broader economic and inflation implications.

Five-year SONIA swaps are currently at 4.30% (14 May 2026), up 29 basis points month-on-month and 46 basis points year-on-year. While lender margins for logistics remain stable and competitive at 145–175bps for prime assets (c.55% LTV), higher swap rates have lifted all-in debt costs to at least 5.75%.

With prime UK logistics yields at c.5.25%, debt is no longer accretive. At the same time, 10-year gilt yields have risen to c.5.1%, narrowing the spread between logistics and risk-free assets. This is likely to drive further softening in pricing, alongside fewer aggressive bids and greater scrutiny of lease structure, income durability and re-letting risk.

However, volatility also creates opportunity. Investors less reliant on debt, or with access to cheaper capital, may benefit from reduced competition and improved pricing. This may be particularly relevant for overseas buyers, given recent sterling weakness.

The outlook remains sensitive to geopolitical developments. If tensions ease, Capital Economics expects 10-year gilt yields to fall towards 4.5% by year-end, easing pressure on property yields.

Political uncertainty adds to market pressure

Financial market volatility has also been compounded by domestic political uncertainty. Following recent local election results and speculation around Labour leadership, concerns over a more expansionary fiscal stance have weighed on sterling and pushed bond yields higher.

Cost pressures intensify for logistics operators

The conflict has also had a direct effect on logistics operators. Around 20% of global oil supply passes through the Strait of Hormuz, and disruption has pushed Brent crude above $110 per barrel, compared with an average of $69 in 2025.

UK diesel prices have risen sharply, reaching around 189p per litre by April, up from c.142p in February. This is feeding directly into distribution costs.

More broadly, inflationary pressures remain elevated across energy, labour and supply chains. With consumers increasingly price-sensitive, businesses have less scope to pass on cost increases than during the inflation spike of 2022.

This environment favours larger operators with scale and operational flexibility, while smaller firms face greater margin pressure. Operators in the optimal locations and in buildings where they can mitigate against some of the rising energy costs will be best placed.

Development costs are also rising, driven by labour, fuel and materials, particularly steel. Combined with softer pricing and yield uncertainty, this is likely to further reduce speculative development activity.

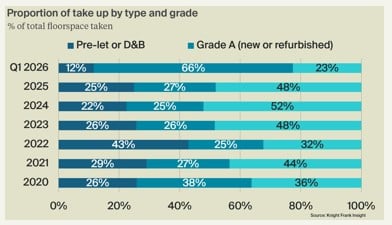

Q1 figures demonstrate occupiers’ focus on core assets

Q1 data shows occupiers overwhelming focus on Grade-A assets, with 77% of take up focused on Grade A space (including pre-let and design and build options). Meanwhile secondhand facilities that are Grade B or worse, accounted for just 23% of take up. This marks a shift from last year and the year before when around half of space take up was in facilities that were Grade-B or worse.

Rising operating costs are pushing occupiers towards buildings that improve efficiency, even at higher rents. Modern assets offer better energy performance, higher eaves, and infrastructure that supports automation and productivity.

While the overall vacancy rate rose in Q1, reaching 8.3%, the rise in the vacancy rate has been driven largely by second hand stock returning to the market, while the availability of new and grade A space is becoming more limited. Grade A vacancy is just 4.2%. However, in some regions it is at or below 1%, notably in Scotland, Wales and in West Yorkshire.

Rent reviews and income risk

The ban on upward-only rent reviews (UORRs), legislated through the English Devolution and Community Empowerment Act 2026, represents a structural shift in lease dynamics.

Historically, UORRs provided landlords with income certainty and downside protection. While strong rental growth has reduced their practical impact in recent years, they have remained important in protecting income during downturns.

Over the long term, rent review structure has had limited influence on average rental growth. However, in weaker markets, UORRs have historically prevented rents from falling in line with wider declines, particularly during periods such as 2008–2012.

The removal of this mechanism introduces greater income variability, particularly for secondary assets. As a result, investors are likely to place greater emphasis on tenant quality, lease length and alternative rent review structures, including indexation.

This may lead to widening yield spreads between prime and secondary stock, and a reduced appetite for active asset management strategies that rely on rental growth.

Read further commentary here:

Amazon enters the 3PL market

In early May, Amazon launched Amazon Supply Chain Services (ASCS), opening its logistics network to businesses beyond its marketplace sellers. This marks a significant expansion of Amazon’s long-standing strategy to monetise its internal infrastructure, positioning it as a direct competitor to global 3PL providers, parcel carriers and freight forwarders.

The initial market reaction was notable, with listed logistics operators and parcel carriers facing downward pressure on share prices, reflecting concerns around intensified competition. Amazon’s ability to leverage scale, data and automation presents a credible challenge, particularly in areas such as pricing efficiency, service reliability and network reach. Its vertically integrated model, underpinned by advanced forecasting and inventory management capabilities, raises the competitive bar for more traditional operators.

However, the impact on real estate demand is likely to be more nuanced. ASCS is unlikely to drive a step change in take-up, as it primarily redistributes existing supply chain activity rather than creating new demand. Instead, the more meaningful effect will be on how occupiers structure their networks.

For large, generalist 3PLs, margin pressure may lead to consolidation, rationalisation of portfolios and a greater focus on highly efficient, scalable facilities. In contrast, specialist operators serving sectors such as pharmaceuticals, automotive or hazardous materials are likely to remain more insulated, given the technical and regulatory barriers to entry.

There is also potential for smaller and regional logistics providers to benefit by integrating with Amazon’s platform, effectively extending their geographic reach and service capability without the need for significant capital investment. This could enable a more flexible, hybrid logistics model, blending owned infrastructure with third-party networks.

The net effect is likely to be an intensification of competition across the logistics sector, rather than outright displacement. For the real estate market, this reinforces existing trends: demand concentrated in well-located, high-specification assets that support operational efficiency, data integration and automation.

Sign up to Knight Frank Research.