The government takes rent controls off the table – again

Making sense of the latest trends in property and economics from around the globe

29 April 2026

The government is not considering a one-year rent freeze in England, a government spokesman told the FT yesterday. Those comments followed a report in the Guardian earlier this week that the policy was on the table as a means to support household budgets as costs rise due to the conflict in the Middle East.

Rent controls don't work – research shows they reduce housing supply, quality and investment in maintenance – so it's good news that the government has quashed the rumour, but floating it before initially refusing to deny it is damaging in and of itself.

Remaining competitive

For the 2026 edition of The Wealth Report, published last week, we spoke to experts about the outlook for London. Tinkering with wealth and property taxes has continued alongside the rise of low-tax competitors like Dubai. Changes to the non-dom regime announced in October 2024 prompted a flurry of high-profile wealthy individuals to announce they were relocating. Upper estimates suggest as many as a quarter of affected non-doms will leave.

Among the themes that emerged in that piece was the degree to which the UK needs a period of stability covering regulation, taxation and politics if it is to remain competitive. Tony Travers of the Department of Government at the London School of Economics told us that the risk is not that London suddenly becomes uncompetitive, but that prolonged political and fiscal uncertainty slowly erode confidence at the margins.

"You do not want political instability, and you do not want a perception that your tax system is just about to be reformed in a way that makes it even less attractive than it is already," Travers added. "Successive governments have managed to do that for some years now."

The UK's private rented sector showed signs of stabilisation in the early months of 2026. UK Finance data showed purchasing activity among landlords had started to rise again, and TwentyCi figures showed that the proportion of homes listed for sale that had previously been let had fallen back to long-run averages. What renters need is for this trend to continue, ensuring supply rises and blunts rental growth. That will require more of the policy stability that attracts long-term investment, and fewer reactive policy signals – even if they are quickly withdrawn.

Passing through

The Bank of England is widely expected to hold Bank Rate at 3.75% tomorrow, but the risks of hikes later this year will only grow the longer talks to resolve the Middle East conflict remain at an impasse.

Economists polled by Reuters last week mostly expect an 8-1 vote by the MPC to keep Bank Rate unchanged this week after March's 9-0 vote. They mostly see rates unchanged for the remainder of the year, which is markedly different from investors. As of Friday, markets priced a quarter-point increase in July, another in September and a small chance of a third before the end of the year.

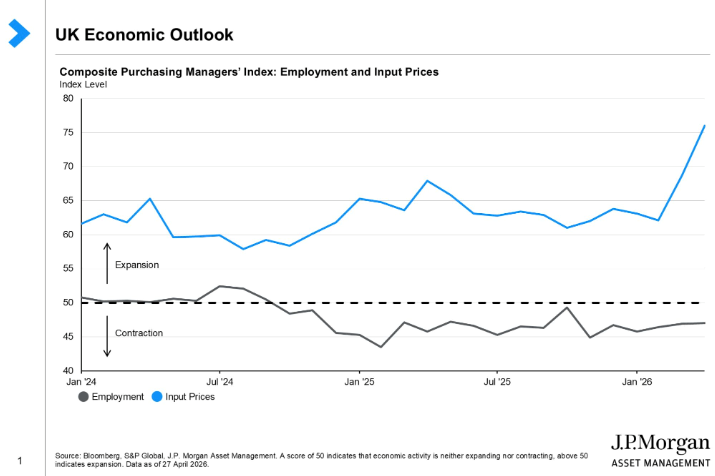

Economists often cite the performance of the jobs market to explain why they believe the BoE will opt to avoid hiking rates. Below is a useful chart from Karen Ward, Chief Market Strategist EMEA at J.P. Morgan Asset Management, showing surging input pricing in a key business survey. Businesses will likely try to pass these costs on to end consumers in the coming months, which will push up inflation, but employers are making layoffs.

"With this backdrop it seems highly unlikely workers in the UK today will feel confident enough to ask their bosses for a pay rise," Ward says. "Rising inflation will thus squeeze disposable income leading households to cut back where they can. This in itself will drag down inflation over time."

New forecasts from The National Institute of Economic and Social Research show the headline rate of inflation picking up to 4.1% at the start of 2027, up from 3.3% now, due to the surge in oil and gas prices caused by the conflict in the Middle East. The group thinks the BoE will raise rates only once this year in July.

Economic shocks

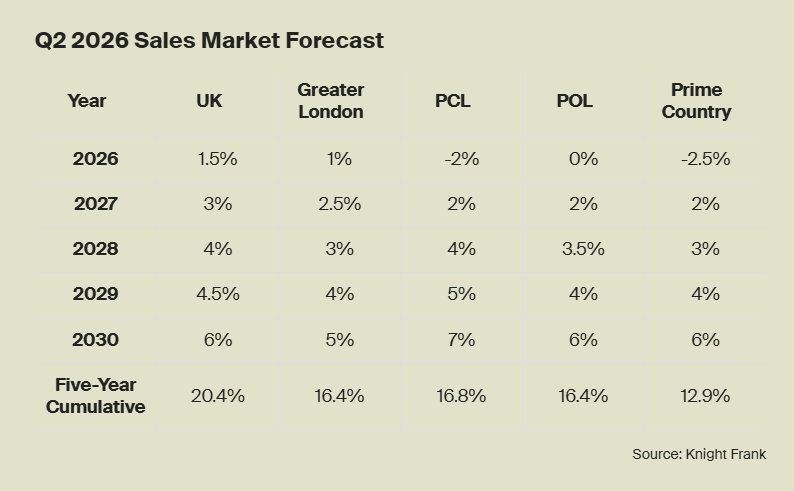

We have revised down our house price forecasts due to the rise in mortgage rates, dampened buyer sentiment and speculation as to how the government will respond to the resulting economic shock.

We expect UK house price growth of 1.5% this year, followed by 3% next year and 4% in 2028. That is down from an expectation in September that prices would grow by 3% in 2026 and 4% next year.

We also expect higher rates to have an impact in prime markets, despite the fact buyers and sellers are typically more discretionary and hold more equity.

Prices in prime central London are forecast to drop by 2% this year, as opposed to an expectation in September they would be flat. Similarly, we think prices in prime outer London will be flat in 2026, which is down from our previous forecast of 2%.

Furthermore, we expect average prices in the prime Country market, an area that covers a range of £750,000-plus rural and urban locations outside London, to fall by 2.5% in 2026. They declined by 5.5% in the year to March.

You can read more analysis from Tom Bill here.

In other news...

Netherlands’ Plan for Tax on Wealth Sparks Fierce Opposition (Bloomberg), Robots Need Offices Too: The AI Boom Comes to NYC Real Estate (Bloomberg), John Lewis sued by Brent Cross landlords for cut of online sales (Times), Homes in London are taking almost a week longer to sell (Times), Taylor Wimpey profits dented by falling house prices and rising costs (Times), and finally, UK wealth tax would backfire, warns IFS (FT).

Sign up to Knight Frank Research.