The New Frontier - Your weekly science and innovation update - 9th March 2026

Your weekly pulse check on science and innovation. Those on the supply side of real estate can track the trends set to drive demand, while occupiers gain fresh perspective on competitor activity and sector dynamics.

10 March 2026

Arms and ambiguity

In the space of a single week the Ministry of Defence (MoD) awarded Leonardo a £1 billion contract for 23 helicopters, with the potential to add 600 jobs while at the same time declining to say when it would publish the Defence Investment Plan that is supposed to give the entire defence industrial base sight of procurement priorities for the next decade. Originally promised for the summer of last year, it slipped to autumn, then to Christmas, then to “as soon as possible”. Most recently, the trade union representing defence workers sent a petition to Downing Street demanding that the PM honours the promise to increase defence spending. Unite’s general secretary, described the delay as “dither and delay” that puts thousands of jobs at risks. The reason for the delay appears to be arithmetical, with a potential £28 billion gap between the ambitions laid out in the Strategic Defence Review and the funding confirmed in the Autumn Budget. Without the Investment Plan companies will find it harder to commit to expanding production capacity and headcount.

While on the topic of defence, AI companies are asking this question: Is this technology for war, or isn’t it? The answer will influence investment decisions and strategic direction, with a knock on impact for real estate.

At the forefront is Palantir, who secured a £240 million UK Ministry of Defence contract in December 2025, and made a commitment to make London its European defence HQ. xAI has agreed to unrestricted lawful military use of its Grok system. OpenAI negotiated a deal with the US Department of Defense that claims it includes safeguards while Anthropic drew a line in the sand when it comes to the mass surveillance of US citizens and autonomous weapons systems. This appeared to have helped them gain consumer trust, with reported record downloads of its AI tool Claude.

Camden takes the start-up crown

Data from Beauhurst finds that Camden has topped the UK local authority rankings for number of company formations in 2025. A total of 45,500 companies were formed throughout the year, an increase of 4.13% from 2024 and 231% from ten years ago. These findings underscore Camden’s status as a thriving tech and innovation hub with just under half of the new companies being in either information and communications or professional, scientific and tech sectors. While the top ten was dominated by London local authorities, Birmingham recorded the highest number of incorporations outside of the capital, with 18,800 new businesses formed in 2025, this was followed by Manchester with 15,500. Overall, the County of Herefordshire recorded the fastest growth rate in 2025 (73.1%), followed by Stafford (58.8%), with both authorities significantly outpacing other areas.

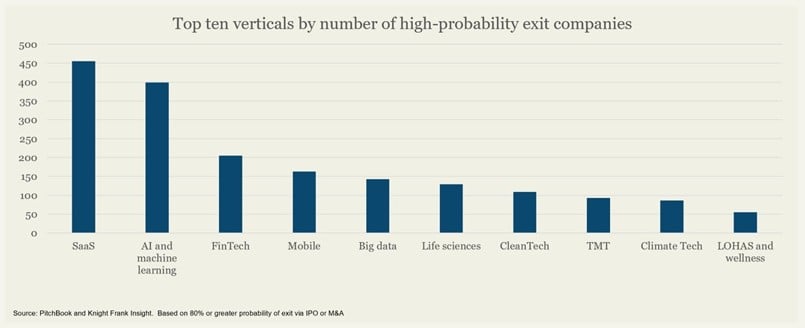

The exit economy

After years of muted public offerings, could the exit pipeline be stirring? Twenty three companies listed on the London Stock Exchange in 2025, raising £2.1 billion, a 170% year-on-year increase in proceeds.

The question of which sectors dominate the UK’s exit-ready cohort is perhaps unsurprising but worth noting. Information technology, software, AI and fintech account for the overwhelming majority of high-probability exit candidates. Healthcare and life sciences form the largest non-tech bloc. And a third cluster, cleantech, climate tech and energy transition technologies is emerging, aligned with decabornisation investment themes. From a geographic perspective most exit-ready companies are in London (61% of total), followed by Cambridge (5.92%) and Oxford (4.16%).

Getting ahead of the exit pipeline matters not only for capital markets but also for real estate. Companies preparing for an IPO, for example typically consolidate their office presence, moving from more flexible arrangements into longer-term leases on high-quality space. Design and fit-out is centred around signalling to investors a clear strategic direction, maturity, and permanence.

Stability without stimulus

The Spring Forecast statement came with no fresh targeted relief or stimulus for science and tech sectors, on which the UK’s long-term competitiveness is supposed to rest. The Chanceller did promise to set out three major choices that will determine the course of the UK economy into the future at a Mais lecture in two weeks: To go further strengthening global trade relationships, to go further in backing innovation and harnessing the power of AI and to go further in transforming our economic geography but no further details were announced. There were also some ommissions from the statement. The call for Evidence on Tax Support for Entrepeneurs, launched at the Autumn Budget and closed at the end of February received no follow up. Industry figures had also hoped for immediate measures to broaden the reach of the Enterprise Investment Scheme and Seed Enterprise Investment Scheme, or for time-limited employer national insurance relief. Neither materialised. Whilst the industry welcomed the emphasis on stability and previously announced growth initiatives there was frustration. Sam North, co-founder of SCALE said that without acceleration the UK risks losing momentum at the very moment its scaleup ecosystem needs it most.

The Spring statement came against the escalating conflict in the Middle East. For science and tech companies, a protracted conflict could increase energy costs, already a constraint on growth. For the broader investment climate, the combination of conflict, commodity volatility and market uncertainty makes capital allocation decisions harder.

Pharma’s new orbit

The UK Space Agency has committed to accelerating the development of an emerging industry focused on space‑based pharmaceutical manufacturing. Companies and researchers are investigating how drugs produced in microgravity could significantly advance treatments for diseases such as cancer. On Earth, the crystallisation of proteins and small molecules is disrupted by convection currents, sedimentation, and other physical forces. In microgravity, these forces are effectively eliminated, enabling the formation of larger, more uniform, and purer crystals.

The government has identified this area as a strategic capability for UK leadership, economic growth, and national security. Companies active in the field include BioOrbit, Space Forge, and OrbiSky. The underlying science is well established. Merck, for example, has been growing protein crystals in space since the early 2000s. Historically, however, progress has been hampered by high costs and limited access, two barriers that are now rapidly diminishing.

In Cardiff, Space Forge is pursuing an ambitious vision of manufacturing semiconductor materials in orbit. Its £22.6 million fundraising round was the largest ever for a UK space‑tech startup, underscoring the momentum building behind this new industrial frontier.

In other news

PitchBook published their latest Emerging Tech Indicator (ETI), which provides a quarterly review of early-stage investment activity amongst the worlds’ top VC firms. AI remained the dominant area of ETI investment in Q4, capturing $5.3 billion across 53 deals. The 10 largest deals alone represented 61.4% of all capital deployed into the vertical, driven by massive investment into emerging frontier AI labs with experienced research teams. Q4 2025 health tech & wellness ETI activity reached $678 million across 23 deals, up significantly compared with the previous eight-quarter average of $332 million and 16 deals per quarter. The uptick in activity reflects emerging opportunities in consumer healthcare technologies and AI-enabled provider solutions as well as a growing VC interest in more traditional healthcare services. Spurred by both new AI-powered threats as well as improved defensive capabilities, ETI activity in cybersecurity spiked to a record $643.1 million in Q4. Biotech is seeing green shoots, driven by the opening of the IPO window and transformative potential of AI in life sciences. As momentum builds, ETI investors have returned to the sector, closing 10 deals in Q4, the most since Q4 2022.

The UK is launching a start-backed research lab for “blue sky” work in AI, with an initial commitment of £40 million awarded over six years to projects that aim to solve fundamental limitations in AI models, such as hallucinations, unreliable memory, and unpredictable reasoning.

The government released £30 million in funding for UK companies developing satellite communications. Scotland may be set to benefit, given it is one of the main clusters for the space industry in the UK. The Scottish Government have a stated ambition for Scotland to become Europe's leading space nation. Scotland's space sector employs more than 7,000 people, with ambitions to increase jobs to 20,000.

OpenAI said it would make London its largest research hub outside the US, citing Britain’s tech ecosystem as an ideal environment to invest and develop new AI systems.

The UK created another Unicorn. London-based Allica Bank, a challenger bank that works with SMEs, raised over £100 million with a valuation of $1.2 billion. The company has been expanding rapidly with employee count growing from 110 in 2020 to 568 by December 2024.

TechBio company Genomics opened its new flagship office in London’s Knowledge Quarter. The company was formed by leading statistical geneticists from the University of Oxford.

UKRI launched a £76 million investment to launch four new national compute resources.

Oxford Biomedica said that Swedish private equity giant EQT decided not to proceed with its takeover offer for the British gene and cell therapy company.

NIHR awarded £47.8 million to 51 NHS healthcare providers and 79 primary care organisations to fund commercial research equipment. The funds will be used to purchase equipment ranging from diagnostic kits and EKG machines to scanners and mobile research units, with 60% of the investment directed toward primary care organisations to bring commercial clinical trials to underserved communities. The award will also be used to modernise research spaces and build new modular facilities. Mobile research units will screen and diagnose patients for trials in areas that lack access to healthcare facilities, while diagnostic equipment will help effectively set up and deliver trial care.

Oxa raised raised $103 million in a new funding round that will support commercial development of its self‑driving software for industrial vehicles, as well as ongoing work in physical AI and robotics. The investment will also fuel the company’s international expansion.

ARIA has invested in CommonAI and its Scaling Inference Lab, which is a testbed for AI hardware technologies. Backed by £50 million, the Lab is set up to address a key bottleneck for startups and research groups developing innovative AI hardware: the lack of an open platform to showcase their technologies due to the dominance of large, closed systems in today’s AI hardware market. Delivered by CommonAI CIC, the Lab will create real and deployable rack-level Al systems, designed to increase the ability of startups to insert new technologies with the goal to rapidly reduce cost of large AI systems.

Sign up to Knight Frank Research.