The New Frontier - Your weekly science and innovation update - 16th March 2026

Your weekly pulse check on science and innovation. Those on the supply side of real estate can track the trends set to drive demand, while occupiers gain fresh perspective on competitor activity and sector dynamics.

16 March 2026

Evotec, Sandoz and the new geography of pharma and biotech

The first fortnight of March delivered a series of announcements that, taken together, describe a life sciences sector in the middle of a fundamental operating model reset. The most striking came from Evotec. The German contract research organisation unveiled its 'Horizon' programme: approximately 800 additional layoffs, closure of four sites over two years (including in Abingdon) and a goal of reducing site count from 14 to 10. The aim is to eliminate overlap and create centres of excellence anchored to its core drug discovery and preclinical development capabilities. Combined with earlier reductions, total headcount cuts since 2024 now stand at approximately 1,400. Targeted savings of €75 million by end-2027 come with restructuring costs of €100 million across 2026 to 2028.

At the same time, Sandoz moved in a structurally different direction. The Swiss generics and biosimilars business announced a dedicated standalone biosimilars unit, separating it from its small molecule generics division to enable 'clear ownership, fast decision making and stronger alignment'. This is a story of strategic concentration and one reinforced by Sandoz's acquisition of Evotec's Toulouse biologics facility, turning one company's rationalisation into another's expansion.

These two announcements sit within a broader industry wave. Novo Nordisk is cutting approximately 9,000 jobs globally. IQVIA reorganised its segment reporting at the start of 2026 without mass layoffs, but with a new CFO and a structural emphasis on its commercial solutions and real-world evidence businesses.

The real estate implications pull simultaneously in two directions. Consolidation and footprint rationalisation is the more immediately visible trend. But some of the forces driving restructuring are also creating new demand for centres aligned with new focus areas.

UK Spinout Investment: Selective, not broken

Data from Beauhurst shows that UK spinouts raised £1.96 billion in 2025, a 45% fall from 2024's £3.57 billion and the lowest total since 2020. Deal numbers declined to 384, the fewest since 2016. On first reading, this looks like a sector in retreat.

It is not quite that simple. The 2024 figure was distorted by megadeals for Autolus and Bicycle Therapeutics, which together represented over a quarter of that year's total. Strip those out and the decline, while real, looks less dramatic.

The sectoral divergence within that picture is sharp and has direct real estate consequences. Life sciences remains the largest sector by deal count at 206 transactions, but its trajectory is downward, with deal volume below the three-year trend. Pharmaceuticals, clinical diagnostics, and precision medicine all recorded fewer deals and smaller average round sizes relative to recent norms signalling moderated momentum. Digital and Technologies tells the opposite story. AI recorded 71 deals with average round sizes above the three-year norm. Cleantech, robotics and automation, sensors, and Big Data all similarly outperformed on deal value.

The geographic picture is equally instructive for those thinking about regional growth and demand. Cambridge spinouts raised £486 million across 52 rounds. Oxford raised £391 million. Together they accounted for more than £800 million, roughly 41% of the national total. But the more interesting signal is at the periphery. Edinburgh, Bristol, Manchester, and Glasgow were all high-ranking universities by deal count and value, and Edinburgh ranked second for top head office locations by number of equity deals into spinouts in 2025.

Where robots go to school

An article in the Financial Times evidenced a new type of facility that barely existed a few years ago is now being built at scale in China, and the question for UK developers is whether demand will grow closer to home.

Humanoid robots require vast quantities of physical, embodied data that cannot be synthesised easily or scraped from existing sources. The main way to generate it at scale is to put robots in a room with human trainers and repeat tasks thousands of times a day. China has moved fastest. Local governments have funded approximately 40 training centres across the country to address data shortages in robotics research. In Beijing's Shijingshan district, the Phase II Humanoid Robot Data Training Centre replicates 16 real-world scenarios that include factories, retail environments, elderly care settings, and smart homes across more than 10,000 square metres, processing over 6 million data entries annually. In Shanghai, AgiBot operates a 4,000 square metre facility where hundreds of VR-equipped data collectors teach robots household and commercial tasks.

The physical design of these facilities is closer to a motion-capture film studio than a traditional factory or lab. They require dense camera arrays and ceiling-mounted motion capture systems, reinforced flooring capable of bearing repeated robotic movement, charging bays, high-bandwidth edge computing infrastructure, and exoskeleton or haptic glove rigs for human trainers. The underlying infrastructure requirements are intensive: power density, connectivity, and specific floor-loading specifications.

As western technology firms scale their programmes, and several major players have announced significant robotics investments the demand for training infrastructure outside China will follow. For UK developers and landlords with adaptable industrial or hybrid assets, the robot training farm is worth watching closely.

It’s all in the name

Google named its King's Cross headquarters Platform 37. The name nods to its location next to the railway station and to Move 37, a move in a game of Go played by DeepMind's AlphaGo against world champion Lee Sedol. The company has also unveiled plans for the AI Exchange, a new public space at the King's Cross campus dedicated to deepening understanding of artificial intelligence, offering free educational programming, interactive exhibitions, and cultural events.

The practice of giving a building a name that carries strategic or cultural meaning is more common across the tech sector than it might initially appear. Salesforce's 'Ohana Floor' concept is now deployed across its global portfolio. 'Ohana' is a Hawaiian term for extended and chosen family and the floors in each building are opened to nonprofits and community organisations. To date, events on those floors have raised over $15 million for charity. Apple's original Cupertino campus was named Infinite Loop, drawn from software terminology. Nvidia named its two Santa Clara headquarters buildings Endeavour and Voyager, both references to exploration missions.

Across all these examples, the same logic operates. Naming a space is a culture signal, a recruitment tool and increasingly a community relations strategy. The most sophisticated examples treat a premium floor or landmark space not as executive real estate but as a civic asset and a physical embodiment of the company's stated values.

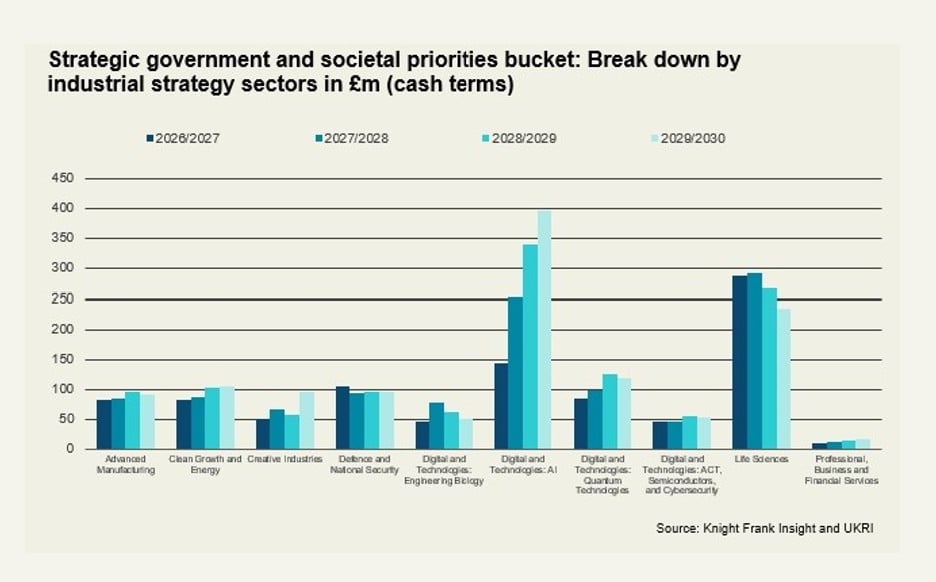

UKRI budget 2026–2030: the bucket list

UKRI provided more details on its new methodology for distributing investment, which is split into three buckets: curiosity-driven research, strategic government and societal priorities, and support for innovative companies. A fourth bucket cuts across all three areas and is focused on activities that enable and strengthen the UK R&D system.

The sectoral rebalancing within the strategic government and societal bucket is where the sharpest signal for real estate sits. The proportion of that bucket flowing to AI is set to more than double, totalling over £1 billion over the period. Life sciences sit in second place in terms of overall funding but its annual share falls from 31% to 19%.

As public research funding tilts towards AI, digital technologies and industrial strategy priorities, the pipeline of research-intensive companies and institutions reliant on that funding will increasingly skew in that direction and the facilities they eventually require will reflect that mix.

Other news that caught my eye this week…

Cambridge / IonQ. The University of Cambridge has launched a major partnership with IonQ to support the creation of the IonQ Quantum Innovation Centre in Cambridge. The Centre will house a 256-qubit quantum computer — the most powerful in the UK when installed.

Swansea. The UK's first National Microgravity Research Centre has been completed at Swansea University.

Wales. A £23 million investment expands pharmaceutical production at Norgine's facility in Hengoed.

European AI. Meta's former chief AI scientist Yann LeCun has raised more than $1 billion for a new European start-up — Europe's largest seed funding round on record.

AI and the workforce. AI job cuts accelerated this week as Block and Oracle signalled that smaller, AI-enabled teams will replace roles, with the resulting savings in some cases redirected into massive data‑centre build‑outs. The debate is whether these job cuts are genuinely as a result of AI or more a case of AI “washing”. On the flip side PwC plans to increase the number of graduates it takes on next year.

The Iran conflict. The Tech sector has become a target in the Iran conflict, with Hackers supporting Iran claiming responsibility for a significant cyberattack against medical device company Stryker. A knock-on effect of this increased activity will be growing demand for digital and cybersecurity consulting and tools.

Government tech contracts. The UK government handed a contract worth £63 million to Atos and Softwire to deliver digital development services for the electoral system. This is part of a broader plan to digitally transform the public sector, with tech firms likely to be the recipients of further government contracts, which may result in expansion-led activity.

Agri Tech fundraise. Tropic closed an oversubscribed $105 million Series C round led by Forbion and Corteva Catalyst. Capital will be used to scale global production of the company’s banana and rice portfolios and accelerate climate-resilient crop pipelines. Tropic, a biotechnology firm specializing in gene-edited tropical agriculture. The firm is based in Norwich Research Park.

Cursor’s annualised revenue surpassed $2 billion in February, according to reporting from Bloomberg, citing a person familiar with the matter, reflecting growing adoption of the artificial intelligence coding assistant and more broadly the growth of so-called vibe coding. The company is reportedly in talks for a funding round that would value the company at $50 billion, a jump of almost 60% from the valuation it secured six months ago. The company’s growth comes with headcount growth. According to PitchBook the firm has gone from 5 employees in 2023 to 300 in 2025. A cursory glance at their careers sits shows that current vacancies are a mix of office-based and remote roles.

This one blew my mind slightly…Australian-based startup Cortical Labs has announced it is building two “biological” data centres in Melbourne and Singapore backed by neuron-filled chips. Cortical Labs grows real human brain cells (neurons) in a dish and places them on top of a microchip covered with tiny electrodes. These electrodes let the chip talk to the neurons (sending signals) and listen to them (reading their electrical activity). The result is a tiny biological computer made from living cells.

And finally, a little teaser on some work looking at AI companies headquartered in London and their headcount growth, part of a broader piece quantifying the AI pipeline and ecosystem in the capital. More to follow in upcoming notes. The dataset covers over 1,000 companies employing 90,899 people in total (note figures are global). The median firm has 19 employees, the mean is 81, unsurprisingly signalling a long tail of small firms and a handful of large outliers. Nine firms hold 40% of employment. Analysing companies that have annualised headcount data between 2020 and 2025, we can see that 85% have grown headcount over the period. Total employment across this panel rose from 14,443 in 2020 to 43,349 in 2025, a net increase of almost 29,000 roles.

Sign up to Knight Frank Research.