Conflict raises new questions for inflation and growth

Making sense of the latest trends in property and economics from around the globe

04 March 2026

Five days into the conflict between the US, Israel and Iran, the implications for the global economy and real estate markets are yet to come into focus.

There were some very large falls in Asian stock markets overnight, led by countries most reliant on energy imports. That heralds where the most immediate pressure is likely to be felt: Asian economies like China, India, South Korea, and Japan are most vulnerable to energy price shocks, followed by Europe and then the US, Ajay Rajadhyaksha, Barclays’ global chairman of research, told Bloomberg this morning.

Still, the reaction in western markets has been more benign in the face of spikes in energy prices not seen since Russia's invasion of Ukraine, largely because there is still much investors do not know. The length of the conflict, Iran’s long-term future and its implications for regional stability, and the effectiveness of US President Donald Trump’s pledge to escort tankers through the Gulf and insure vessels via the US Development Finance Corporation all remain uncertain. US stocks and bonds stabilised after the US government issued those pledges. Yields on two-year gilts jumped for a second day, though yesterday's rise of 16 basis points to 3.8% later eased back to settle 10 basis points up.

At the very least, central bankers can be expected to act with more caution in the coming months. Investors now put the probability of a March rate cut by the Bank of England at just over 25%, down from 90% last week. Traders now expect one cut by the end of the year, down from two.

Upside risks

Consensus at this stage is that the conflict will be relatively short. Capital Economics outlined three potential scenarios in a note to clients. In the first, energy prices stay around $80 oil and 115p gas until June, then gradually fall back as the conflict resolves quickly. In the second, energy prices rise to $100 oil and 150p gas until June as supply tightens but fall back once the conflict ends. Finally, a longer conflict and infrastructure damage keep prices near $80 oil and 115p gas through 2026, before easing in 2027.

Scenarios 1 and 2 slow the pace of disinflation, while scenario 3 brings another bout of inflation. The company reckons the Bank of England may prove more sensitive to upside inflation risks than many other central banks, given that both headline inflation and inflation expectations are already above levels consistent with the target.

Still, Capital Economics isn't changing its forecasts yet, but the conflict adds upside inflation risks that could delay the next cut to April and cap easing – 3.25% (scenario 1), 3.50% (scenario 2), or no cuts and possibly a rise (scenario 3).

Significant impacts

You probably missed it, but Chancellor Rachel Reeves delivered the Spring Statement yesterday and largely stuck to the message briefed to the media last week that it would be "very, very boring."

New projections from the Office for Budget Responsibility (OBR) showed slower growth this year of 1.1%, down from 1.4% in 2025, but faster growth of 1.6% in 2027 and 2028, up from 1.5% previously. That's all largely moot now, of course.

“Conflict in the Middle East, which escalated as we were finalising this document, could have very significant impacts on the global and UK economies," the OBR added.

Officials tasked with facing reporters after the statement did add a little more detail. David Miles, a senior OBR official, said the rise in global energy prices, if sustained, would add as much as 1% to the level of consumer prices, according to the FT write-up.

Planning reforms

The OBR expects house price inflation to average a little more than 2.5% during the next five years, largely unchanged from the November forecast. The average effective interest rate on the outstanding stock of mortgages is expected to rise from 4.1% this year to 4.5% on average, which is 0.3 percentage points lower than the previous outlook.

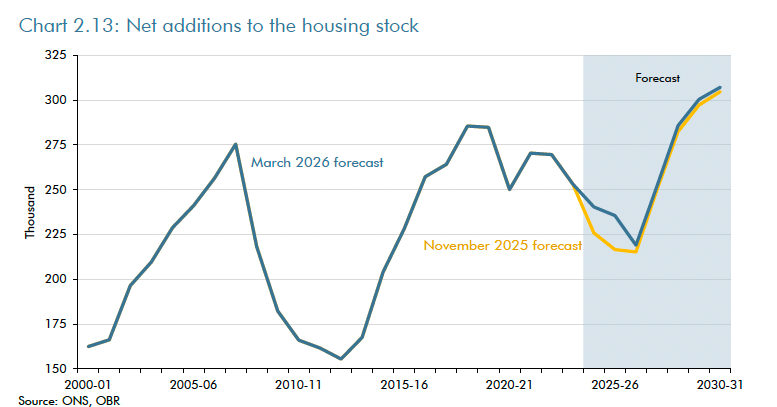

Net additions to the UK housing stock are expected to fall from an average of 260,000 a year in the early 2020s to a low of 220,000 in 2026-27, as recent subdued housing starts feed through. The OBR then expects net additions to rise sharply to just over 305,000 by 2030-31, reflecting the impact of planning reforms. In the current environment, that feels implausible. That level of output would leave cumulative UK net additions between 2025-26 and 2029-30 at 1.3 million, around 30,000 higher than in November.

Finally, the OBR expects growth in housing transactions to average around 2.5% a year over the forecast period "as the housing market turnover rate returns to its assumed medium-term equilibrium and the housing stock continues to grow, boosted by the impact of planning reforms." Transactions are forecast to reach 1.3 million in 2030, similar to the November forecast.

In other news...

Tax exiles in Dubai should pay to be protected by Britain, says Lib Dem leader Sir Ed Davey (LBC), executives’ mood sours on economy as consumers cut spending (Times), and finally, stranded Britons must wait for Middle East evacuation flights (Times).

Sign up to Knight Frank Research.