UK Hotel Trading Performance Review and outlook

Despite the unsettled and challenging trading environment encountered in 2025, the sector has shown steadfast resilience, with a much more robust performance achieved during the second half of the year.

As a result, the steep declines in GOPPAR endured during the first half of the year, driven by reductions in the ADR, combined with increasing costs, were reversed, with full year RevPAR for 2025 on par or ahead of the previous year and GOPPAR almost stable, across most segments in London and regional UK.

As we move into 2026, the operating landscape in the UK has become increasingly challenging, shaped by the cumulative effect of recent policy shifts — including higher business rates, rising employment costs, and new regulatory obligations. Together, these pressures are likely to temper the pace of growth in the UK market over the near term.

Many hoteliers will be looking to sustain the positive trading momentum that underpinned the strong finish to 2025. While budgeting remains cautious across much of the sector, there is measured optimism that 2026 will bring continued revenue growth (building on last year’s comparatively resilient performance) – supported by increased room rates and continued growth in wellness and leisure demand. The biggest challenge, however, will be protecting the Net Operating Profit, as the strong rise in business rates is expected to erode margins across all segments of the UK hotel market.

A year of two halves for the UK Hotel Market in 2025

For the full year 2025, London achieved an average occupancy of 82.5%, an uplift of 1.2 percentage points versus the previous year, with sustained occupancy growth achieved from March through to November. However, ADR proved more challenging from the outset, declining by 2.5% year‑on‑year over the first six months. Stronger seasonal demand in the second half of the year supported a recovery in ADR, with 2% growth over this period offsetting first‑half declines and resulting in full‑year ADR ending broadly in line with 2024.

Whilst all London hotels recovered strongly during the second half of the year, averaging year-on-year RevPAR growth of 4.4% for the six-month period, it was a story of two halves for most segments. For the full year, London achieved year-on-year RevPAR growth of 1.5%.

Across regional UK, notwithstanding a challenging operating backdrop - which during H1 regional UK experienced a decline in RevPAR of 0.4%- the regional hotel market benefited from a more positive set of results generated in the second half of the year, which outperformed the same period last year. In H2, occupancy increased by 1.2 percentage points to 79%, ADR increased by 2.2%, driving RevPAR growth of 3.8% - a positive end to the year. Regional UK thus closed the year with a 1.9% rise in RevPAR to £79, supported by balanced contributions from both rate and occupancy.

Meanwhile the steadfast support of ancillary revenues continued, with marginally stronger growth coming from F&B revenues, TRevPAR grew across the year by 2.0%.

Growth in Ancillary Revenues – underscoring the growing value of ‘Other Minor’ revenue streams.

A defining theme in 2025 was the strong performance of leisure revenues, with UK hotels which offer leisure facilities benefitting from the broader expansion of the UK Health and Fitness sector. As a result, the uplift in leisure revenue, which has stemmed from rising membership numbers, increased demand for spa experiences, and sustained interest in wellness and fitness amenities, increased year-on-year by 7.3% per available room, and a 39% rise since 2019.

Meanwhile, the monetisation of car‑parking spaces has accelerated significantly, with revenues now 32% higher than in 2019. Across Regional UK, in 2025 hotels reported a 10% rise POR in car parking revenue, underscoring the growing value of ‘Other Minor’ revenue streams.

Profitability broadly stable, but with notable variance by hotel class.

During a year of low revenue growth, UK hotels have demonstrated remarkable reslience, albeit with varying degrees of success. Most segments ended 2025 at or close to the profitability levels achieved in 2024, but the strongest performance came from markets with a high volume of leisure demand.

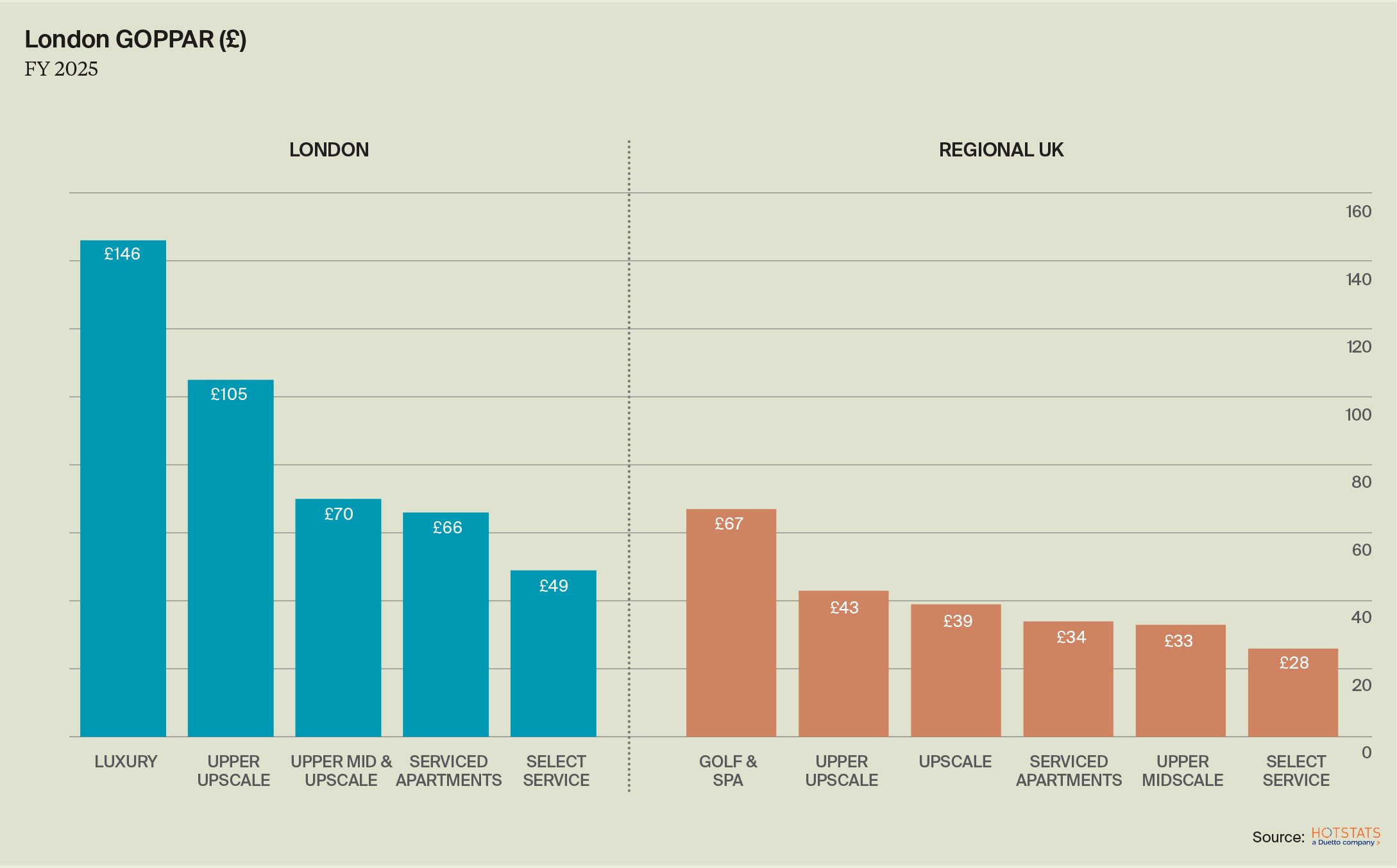

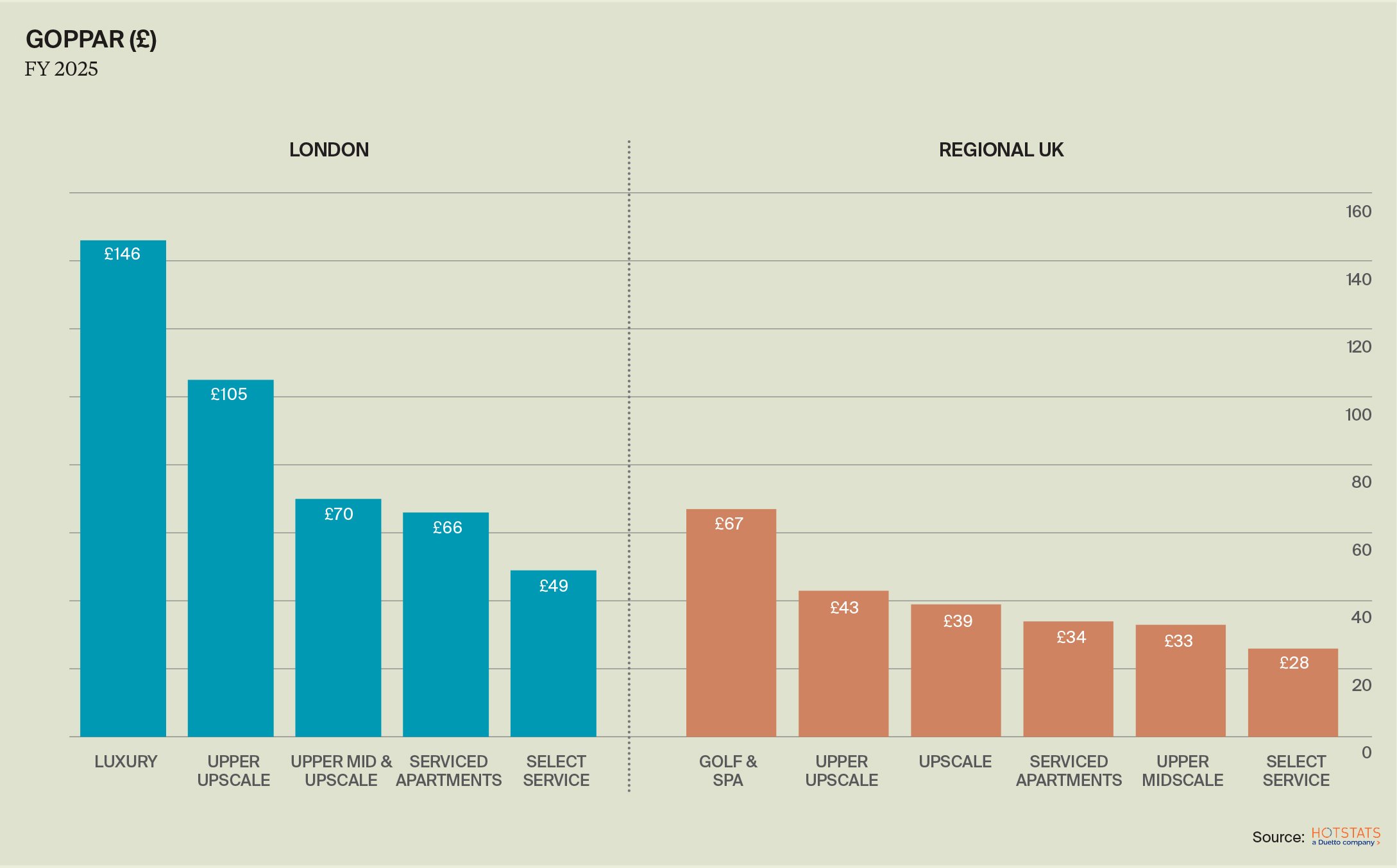

London’s hotel market saw GOPPAR fall 0.5% in 2025 to £111.60, whilst its profit margin fell by 1.1 percentage point to average 41.1%. Across regional UK, GOPPAR held steady at £37, though the GOP margin fell by 0.5 percentage points to 30.3%.

GOPPAR winners and losers

In 2025, the regional upscale segment outperformed all UK hotel classes, recording the highest gains in GOPPAR at 3.4% annual growth, reversing its first half deficit of 4.8%. Where regional upscale hotels truly excelled, was in converting revenue growth into profitability, through a reduction in overheads, despite facing the same elevated payroll pressures as the wider UK hotel sector.

Golf & spa hotels recorded the strongest TrevPAR growth of all UK hotel segments in 2025, achieving a 4.2% increase year-on-year. However, the segment faced pronounced payroll cost pressures, with payroll expenses rising by 6.6% PAR over the same period. Notable efficiency gains were though generated in the second half of the year, enabling the segment to achieve full-year GOPPAR growth of 2.8%.

The biggest declines in GOPPAR were suffered by London’s luxury hotels and regional Serviced Apartments. London’s luxury hotels achieved respectable TRevPAR growth of 2% year-on-year, but this did not provide enough cushion to withstand the rising costs, leading to a 4.0% decline in GOPPAR. For regional serviced apartments, a 3.6% decline in RevPAR led to a sharp decline in GOPPAR, but its lean cost base continued to support the strongest margin performance across regional UK, at 39.5%.

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.