London’s real estate markets rely on a shared framework to achieve competitiveness: time, place, product, and capital. Yet, its housing market is shaped by a fifth factor: policy, which can influence viability, accelerate delivery, and unlock stalled sites.

Policy is a defining factor shaping the London housing market’s current cycle.

From planning reform to regulatory complexities, government measures play a decisive role in determining whether London can meet its workforce’s housing needs.

Without the right measures in place to support demand and supply, the consequences of slowing development in the capital extend far beyond the residential sector and directly affect London’s economic competitiveness.

At a glance

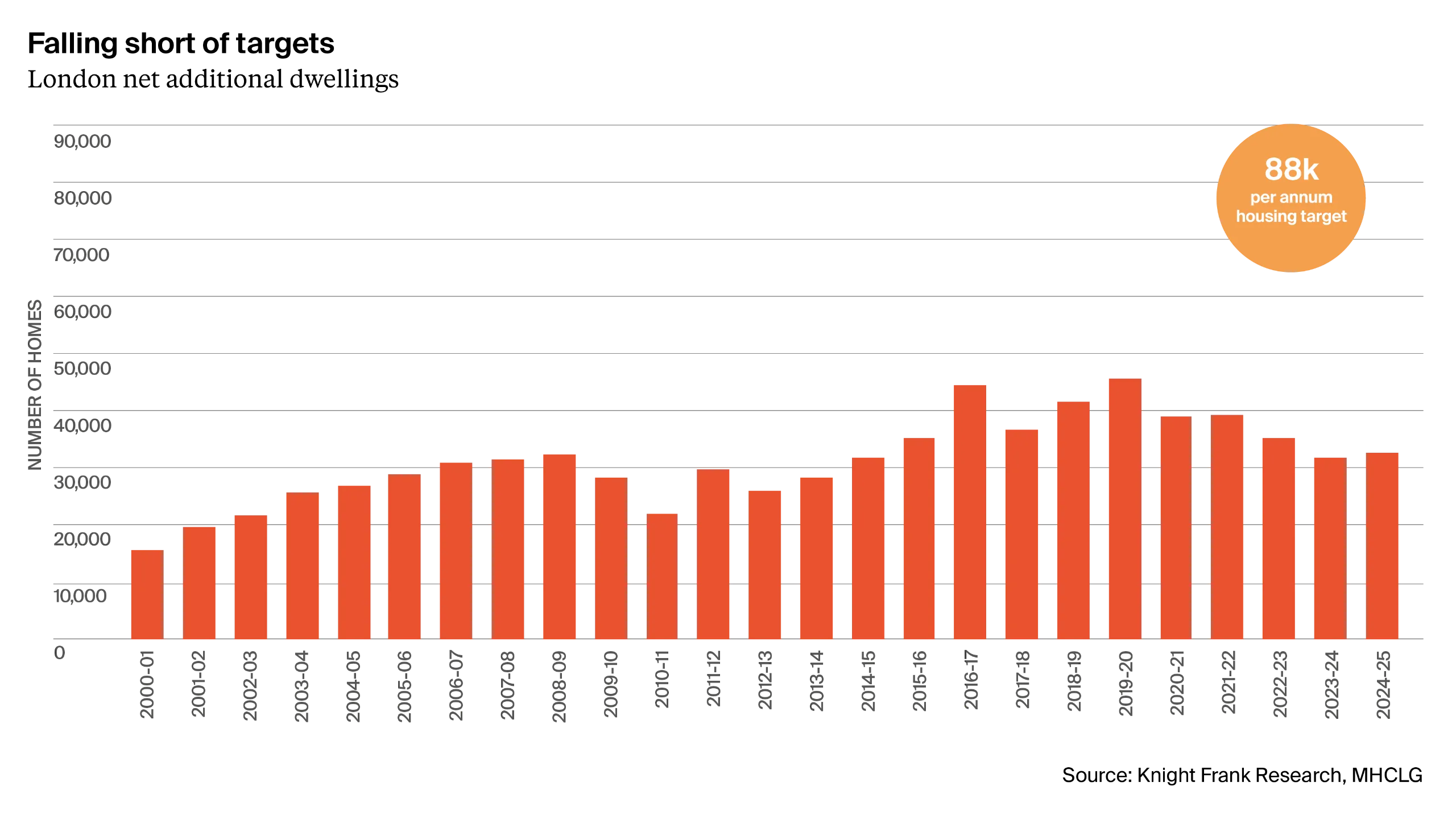

London is delivering far fewer homes than required, with just 33,000 completions in 2025 - only 37% of the annual 88,000 housing target. Low starts today mean low completions in the years ahead.

Developers encounter a challenging environment shaped by worsening viability, construction cost inflation, tighter development finance, and delayed exits.

Political alignment has led to emergency measures to unlock development. These measures offer an incentive to bring schemes forward before 2028, improving strategic decision-making and accelerating land activity.

Developers are seeing early – but fragile – improvements in viability and risk-weighting.

Monetary policy is easing, supporting development financing and buyer affordability. Long‑term recovery hinges on deeper reforms such as improved planning, reduced review burdens, streamlined Gateway timelines, and stronger exit absorption.

Developers and investors may gain an advantage if they can unlock sites during this window.

London’s housing crisis is deepening.

In 2025, just 33,000 homes were completed – only 37% of the 88,000 homes needed each year.

Delivery has fallen 28% since 2020, putting the capital on a trajectory moving further away from its long-term housing goals. Yet, there are signs that suggest the worst is behind us. Lower interest rates, a more aligned political landscape, policy reform, and renewed confidence should help unlock momentum as we head into 2026. Development sites have started to return to the market, a trend that could support a rebound in land transactions.

Figure 1: Falling short of targets – London net additional dwellings

For developers willing to take a strategic view – and who can unlock sites now – these factors could present a unique opportunity to deliver homes. But seizing that opportunity isn’t straightforward, and it’s not going to move the needle anywhere near 88,000 homes.

Looking back to look forward

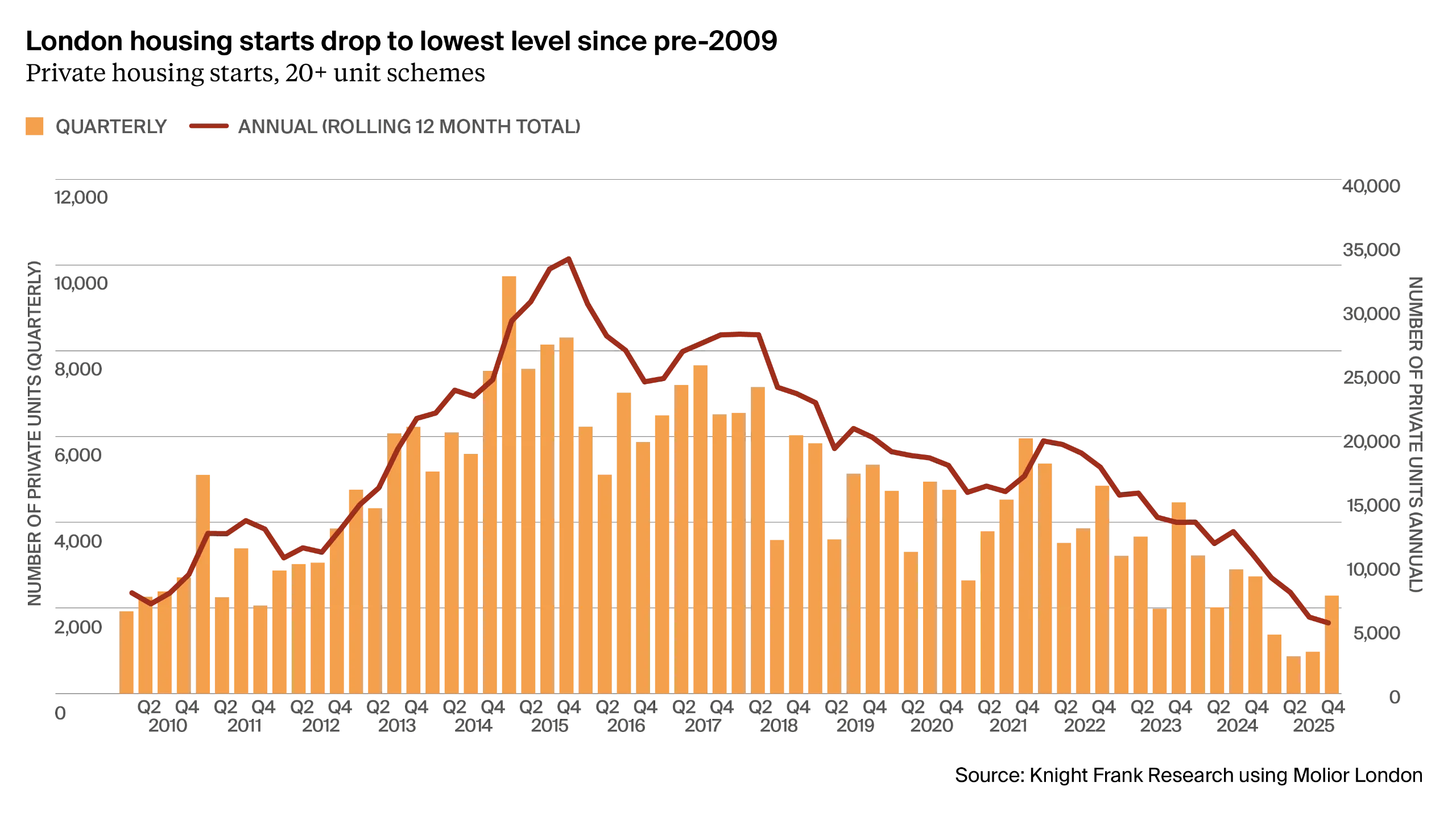

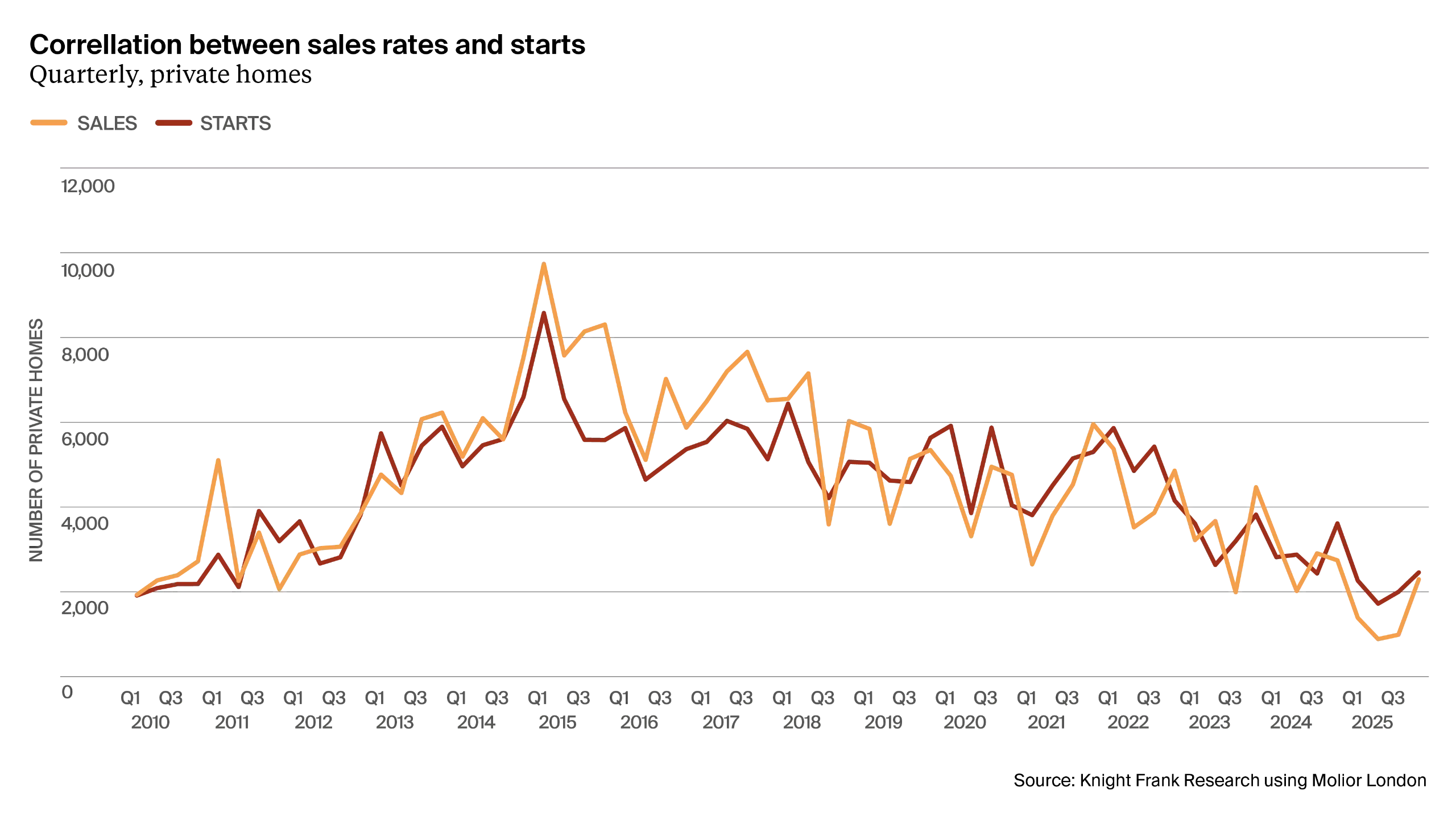

The decline in new housing activity has been starkest in the private sector, where housing starts have fallen to their lowest levels since 2009.

Molior data shows just 5,500 new private homes broke ground in London during the whole of 2025 – half the level of 2024 and 83% lower than the 2015 peak.

Figure 2: London housing starts drop to lowest level since pre-2009

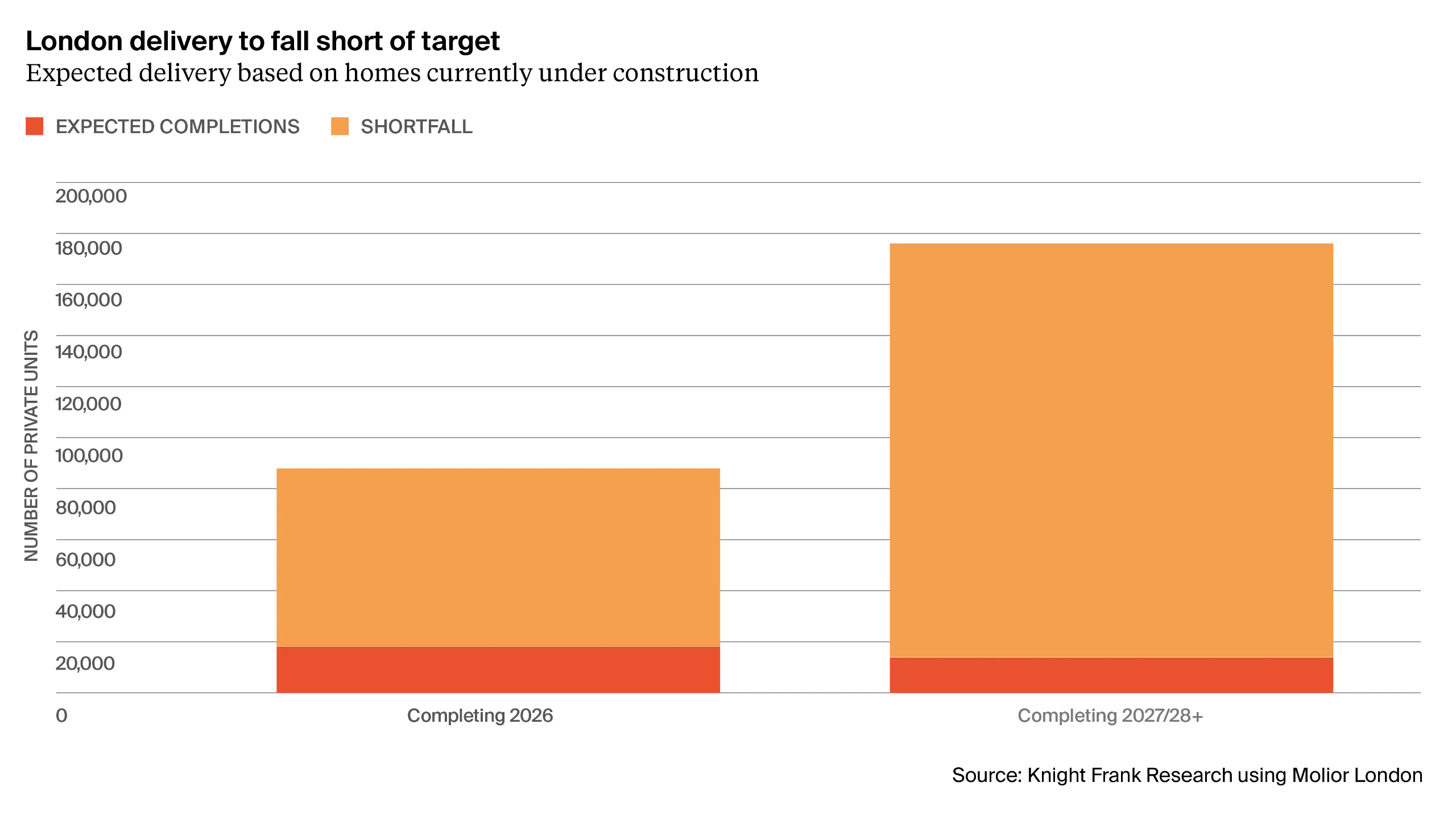

This falling level of starts has longer-term implications: low starts today mean low completions in the years ahead. Based on the current delivery pipeline, 14,053 homes are expected to complete across 2027 and 2028, just 8% of the government’s 176,000 two-year housing target.

Figure 3: London delivery to fall short of target – Expected delivery based on homes currently under construction

The perfect storm

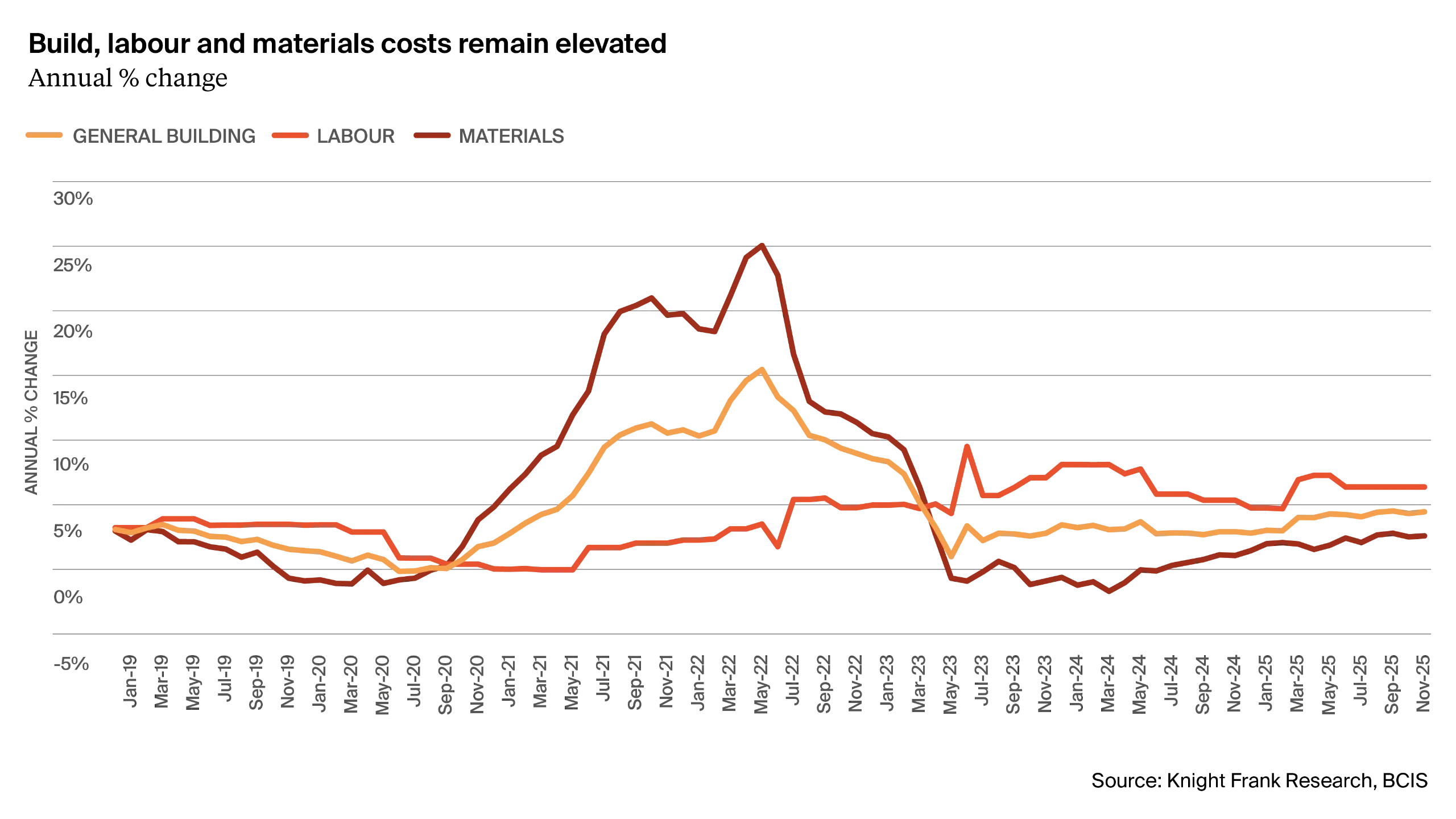

The current slowdown isn’t the result of a single shock – a myriad of challenges has collectively impacted viability and confidence.

On the development side, construction inflation has risen sharply in recent years, up by more than 30% since 2020 according to the BCIS.

Compounding this, the cost of development finance has become more restrictive. Borrowing is more expensive, lender appetite can be more conservative, and risk adjusted returns are more difficult to achieve.

Regulatory and procedural delays add further complexity. The planning system has faced additional pressure from new building safety requirements. The Gateway process has introduced significant delays for high-rise buildings, adding months to development timelines.

Figure 4: Build, labour and materials costs remain elevated

Show me the exit

At the same time, the sales market for new-build homes has weakened, particularly among domestic buyers and buy-to-let investors.

The previous peak in London housebuilding was in 2015, when developers started 33,782 homes – still less than half the government's target. Developers sold 26,313 homes that year, aided by Help to Buy and plenty of off-plan investor sales, de-risking projects and enabling them to progress.

But the government introduced a 3% stamp duty surcharge for second homes and buy-to-let properties a year later, and off-plan investor purchasing dwindled. That levy has since been raised to 5%, a move which followed the closure of Help to Buy in 2023. Starts have now been falling for a decade.

Figure 5: Correlation between sales rates and starts

Private new homes sales totalled 8,436 in 2025, according to Molior, down 28% annually. The impact of weaker demand is clear: if developers can’t sell homes, they won’t build them.

And yet, there are early signs of improvement. Both starts and sales rose markedly in Q4 2025 versus the rest of the year. The numbers remain far from where they need to be but the data implies momentum may be returning – albeit slowly, and from a low base.

This time it’s different. So, what’s changed?

For the first time in more than a decade, London benefits from political alignment between central government and City Hall.

This alignment helped pave the way for emergency measures, announced jointly by the Ministry of Housing, Communities and Local Government and the GLA in late 2025, aimed at unlocking development.

Although still at consultation stage, the proposals paint a positive picture for improving supply. The withdrawal of guidance restricting density and additional mayoral intervention powers should also help shift risk in favour of getting projects off the ground. A temporary reduction in affordable housing requirements to 20% suggests a more pragmatic stance. The net result is that we’re likely to see more schemes come forward where the development economics now make sense.

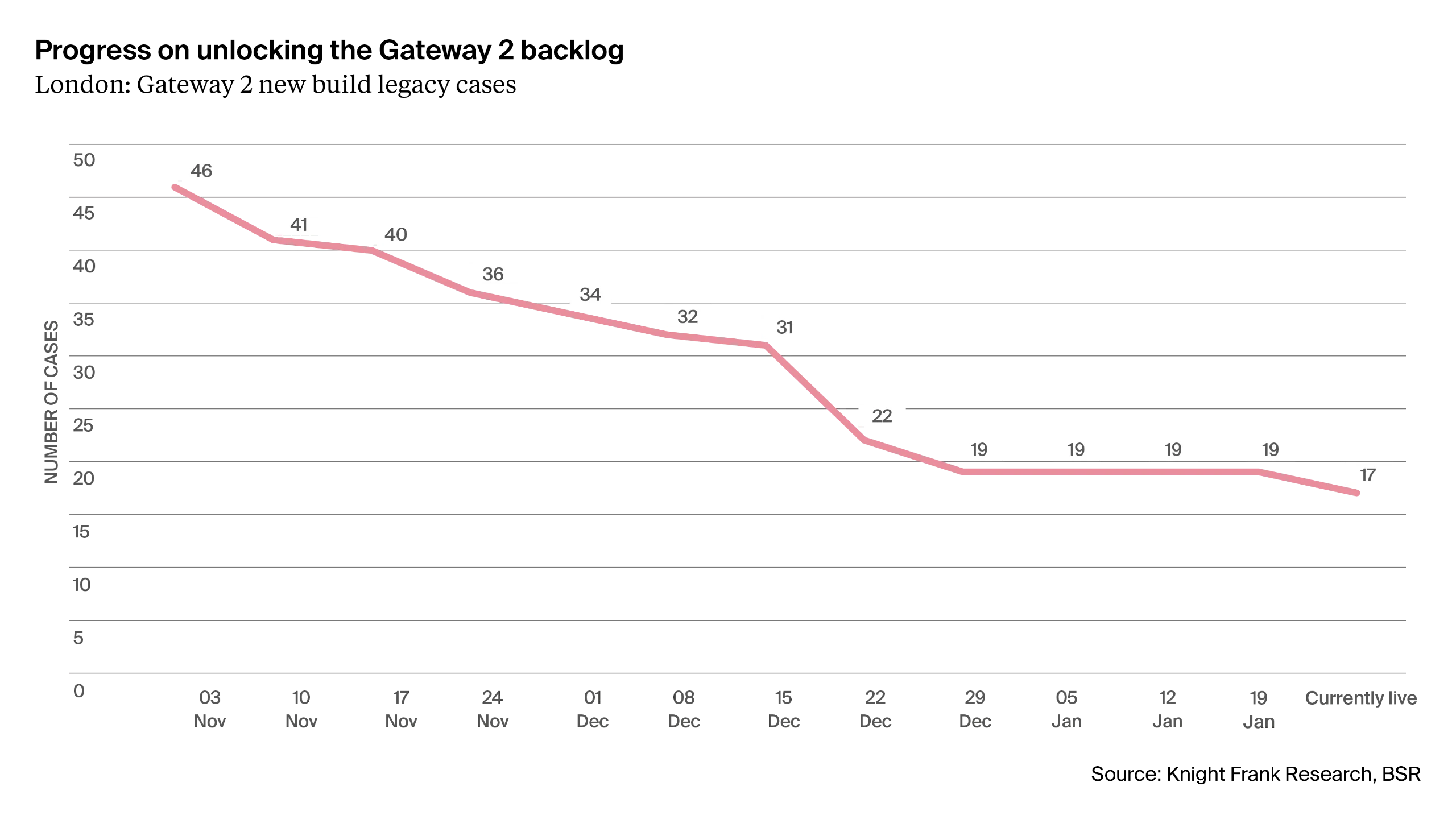

The measures are also time limited, so development will be more profitable now than it will be post-2028, providing developers with a powerful incentive to get building. However, delays at the Building Safety Regulator (BSR) relating to Gateway 2 remain a blocker to the delivery of high-rise, high-density housing.

Figure 6: Progress on unlocking the Gateway 2 backlog

While challenges remain, clearer guidance, better resourcing and a more proportionate approach to approvals have begun to reduce bottlenecks.

The latest data from the BSR shows legacy new build cases in London are down from nearly 50 in November to 17 at the end of January, with 7,354 residential units approved.

While this signals a more favourable policy environment, these reforms are likely to be the first difficult steps towards reversing the generational decline in housebuilding.

Macro matters

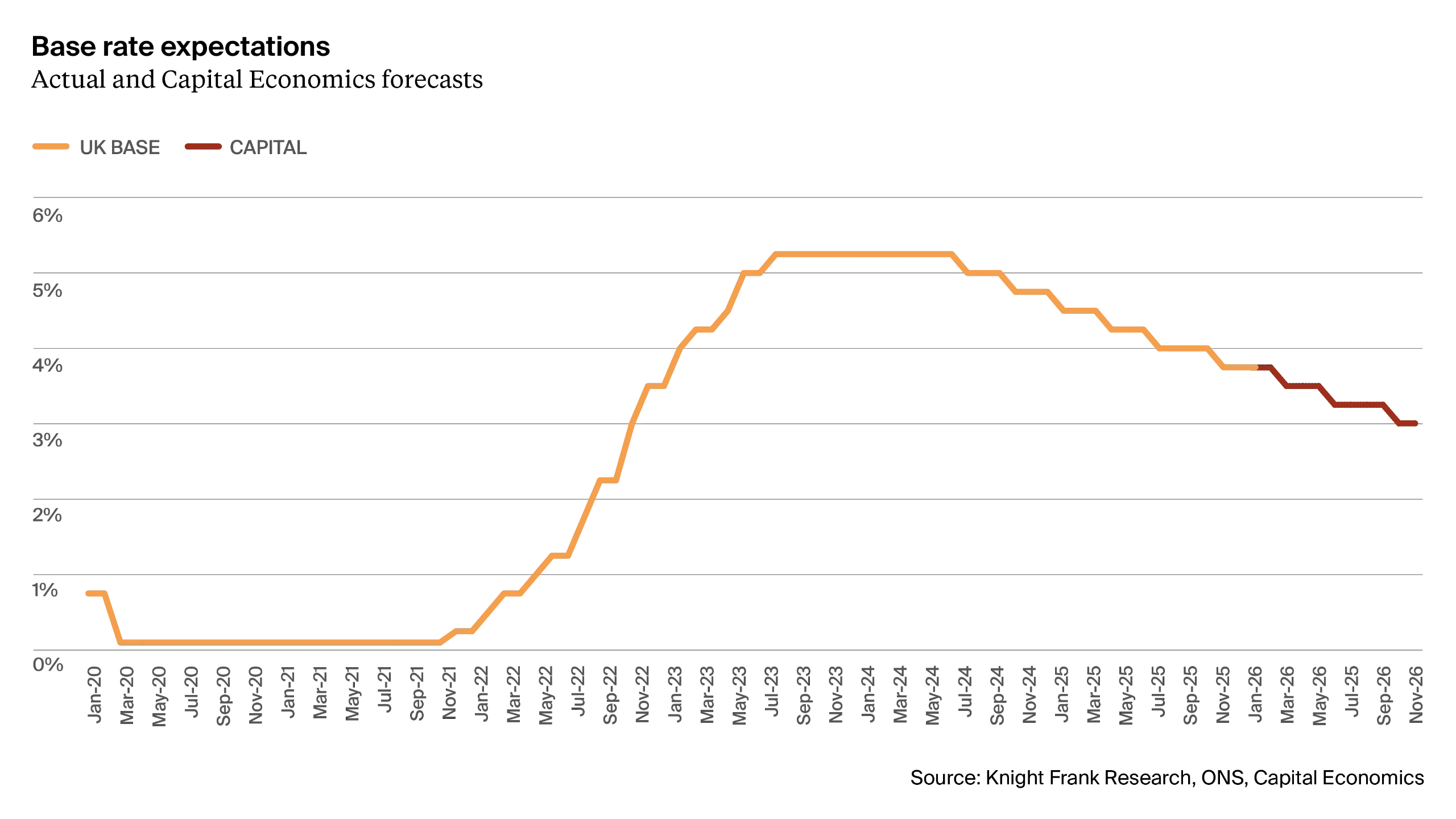

The fact the Bank of England has cut rates six times since 2024 – bringing the base rate down to 3.75% – matters for development viability and mortgage availability.

The future direction of monetary policy is also now firmly towards supporting growth even if there’s still caution. Further rate cuts are expected throughout 2026, which will improve the pricing of debt available to developers, and loosen the affordability burden on buyers. Capital Economics expects three cuts in 2026, taking the base rate to 3.0% by year-end, one more than the two expected by financial markets.

Figure 7: Base rate expectations – Actual and Capital Economics forecasts

Progress, but you can’t live in a planning permission.

While recent reforms mark meaningful progress, more is required if London is to restore delivery to sustainable levels. So, what do we need?

1. The planning system must continue to evolve, reducing uncertainty and enabling timely decision-making.

2. The removal of late-stage review mechanisms, an outdated tax imposed on developers that undermines viability and discourages equity investment.

3. Improvements to the Gateway system must continue until approval times become predictable and proportionate.

4. Demand-side support – developers won’t build housing at scale if there is insufficient absorption on exit. Targeted support for first-time buyers would help restore the confidence needed for private developers to commit to new schemes.

Read the full paper

Access all the details from Insight 5 in The London Series 2026