London’s office market is entering a new cycle shaped less by volatility and more by structural clarity. The turbulence of the early 2020s has given way to a market where risk has been re‑priced, supply is tightening, and demand is consolidating around high‑quality space.

This is a steadier, more disciplined expansion – one where London’s scale, liquidity and labour‑market depth give it an advantage that few European cities can match.

As the conditions that once fuelled oversupply fade, the city is shifting into a position where momentum feels quieter, but ultimately more durable.

At a glance

London’s scale, liquidity and labour-market depth underpin its resilience. Vacancy rates are below long-term norms, and prime rents have risen, outpacing all major peers.

Occupiers face a tightening market where securing future-proofed buildings early will be critical as demand outpaces supply.

Developers can leverage London’s structural resilience to justify new schemes but must anticipate strict planning and longer lead times.

The next phase is defined by structural scarcity. Planning and procurement now consume a larger share of development timelines, providing a first mover advantage.

Occupiers should commit decisively to best-in-class space and avoid optionality that delays delivery.

Developer and investor strategies should reflect the changing investment landscape to outperform where risk-adjusted returns are improving.

Office jobs growth will outpace peers, capital inflows remain robust, and supply is tightening. This points to a multi-year period of steady rental growth, resilient income and superior returns.

Occupiers should expect rising rents and limited availability of prime space, and act early to avoid cost pressures.

Landlords and developers can position themselves for sustained rental growth and income resilience but must be disciplined with delivery.

Our fourth paper in The London Series 2026 explores the role of capital in the London office market.

Capital is one of four variables in the London Equation, our framework for understanding how the city competes.

Strength in scale, momentum in demand

London’s economic outlook over 2026-30 signals a period of steady, broad‑based expansion rather than exuberant growth – but it remains one of Europe’s most durable office markets.

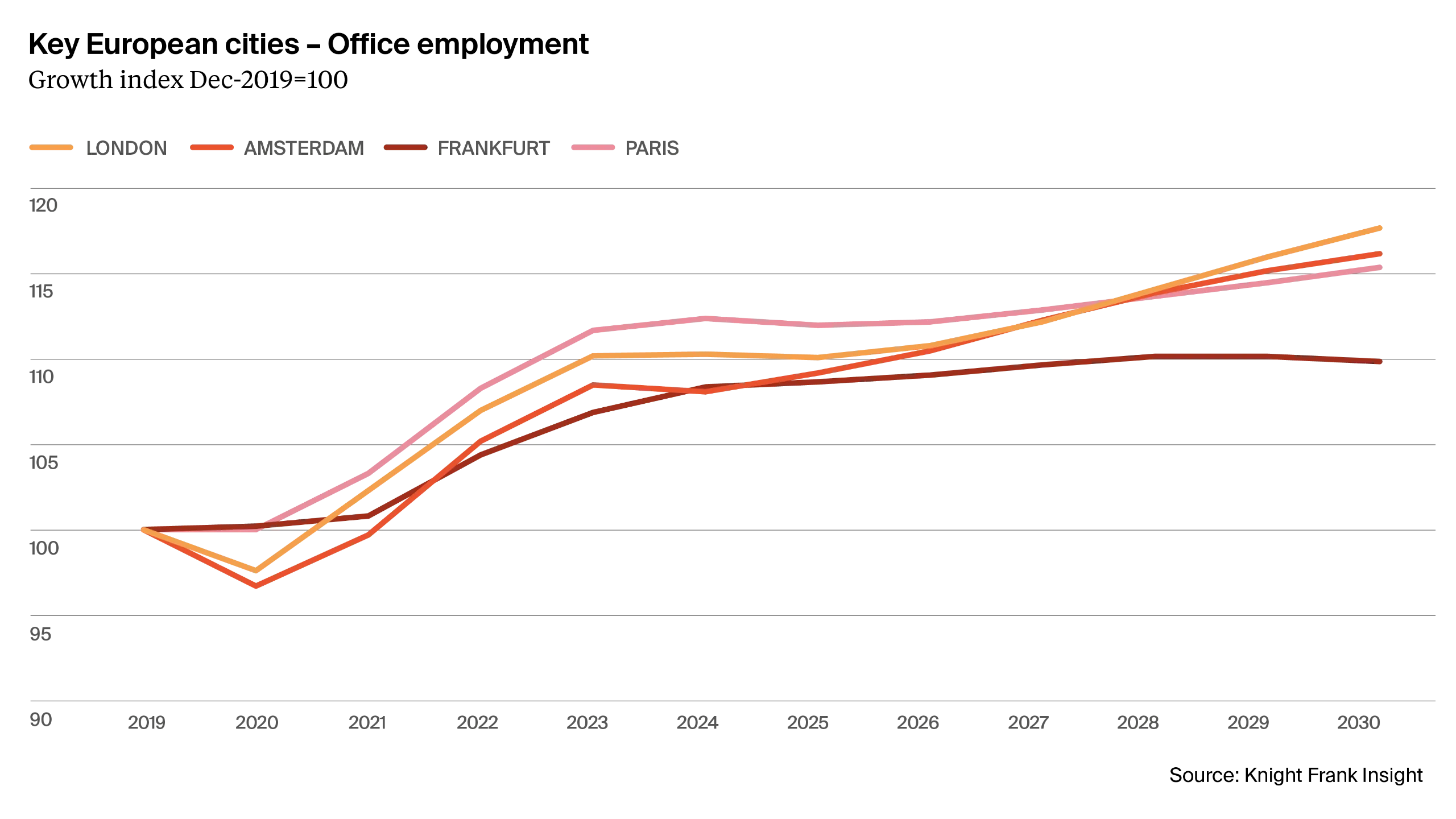

What distinguishes London is the depth of its labour market: over the next five years, the city is projected to add around 186,000 office‑based jobs, far more than Paris, Madrid, Berlin or Amsterdam. In a continental context, London’s labour market remains the engine room: large enough to absorb shocks, diverse enough to sustain hiring across sectors, and attractive enough to continue pulling in firms seeking access to global talent.

This momentum shapes the demand side of the office equation, which is increasingly the decisive factor in market performance. Even as real‑estate delivery slows across Europe, London’s ability to generate far more incremental office jobs than any peer reinforces its relative resilience.

Cities that grow their knowledge‑economy workforce the fastest – and by the largest absolute numbers – are best placed to sustain rental growth.

Seen through this lens, London’s forward profile is not one of runaway growth but of quiet strength: an economy still expanding, a labour market still deepening, and a projected wave of new office‑using workers unmatched anywhere else in Europe.

Figure 1: Key European cities – office employment

The capital that keeps attracting capital

Staying power has always been one of London’s defining advantages, and the investment data confirms that resilience.

Even through a period of sharply higher rates and weaker global risk appetite, London has continued to attract more capital than any other major European office market. In the most recent window, 2023-2025, the city drew an average of £6.9bn per year, ahead of Paris at £6.0bn and far beyond Amsterdam, Berlin, Madrid and Milan, which each sat closer to £1bn annually according to MSCI data.

This consistency speaks to the city’s long‑standing role as Europe’s most liquid, most internationally recognised safe harbour for real estate investment. The depth of cross‑border demand reflects the breadth of London’s investor base, the transparency of its market, and the global familiarity that anchors allocations through cycles.

Breaking away from the pack

Across Europe, office markets are still settling into a slower, structurally more selective cycle. London, by contrast, is beginning to separate from this middle ground.

Vacancy in both the City Core and West End Core is now below long‑term averages, with the City falling from 7.6% to 6.2% in a single year – a clear sign demand is re‑anchoring around high‑quality space. Prime rents in London are also rising more decisively than in any major peer.

City rents increased by 11% over the past year, and the West End by 22%, outpacing Paris, Berlin, Madrid and Amsterdam, all of which posted far smaller uplifts.

London is projected to record the strongest prime‑rent growth in Europe between 2026 and 2030, supported by its deep occupier base and a sustained shift toward modern, high‑spec buildings.

These fundamentals translate into a compelling investment proposition. The City market in London offers higher prime yields, giving investors more income on day one. This yield sits alongside a stronger rental outlook and healthier occupancy trends, creating a combination of income resilience and growth potential hard to match.

The West End meanwhile functions as London’s defensive core – a market where scarcity, brand value and global occupier demand have consistently translated into resilient income. Over the next five years, prime rents are expected to grow by around 4.2% per annum, supporting real income growth even in a calmer economic environment.

Attractive today, compelling over five years

Core offices in the City look increasingly compelling as the next cycle takes shape. Using the market’s own forward signals, a stabilised, income‑secure asset delivers a gross annual return of around 10%, and this is without any yield compression.

For Core Plus, the opportunity looks even more pronounced. With rents reset to market levels and continuing to grow, a Core Plus London City asset generates a five‑year cumulative return of around 83%, equivalent to around 13% per year, again with no yield movement assumed.

Scarcity era begins

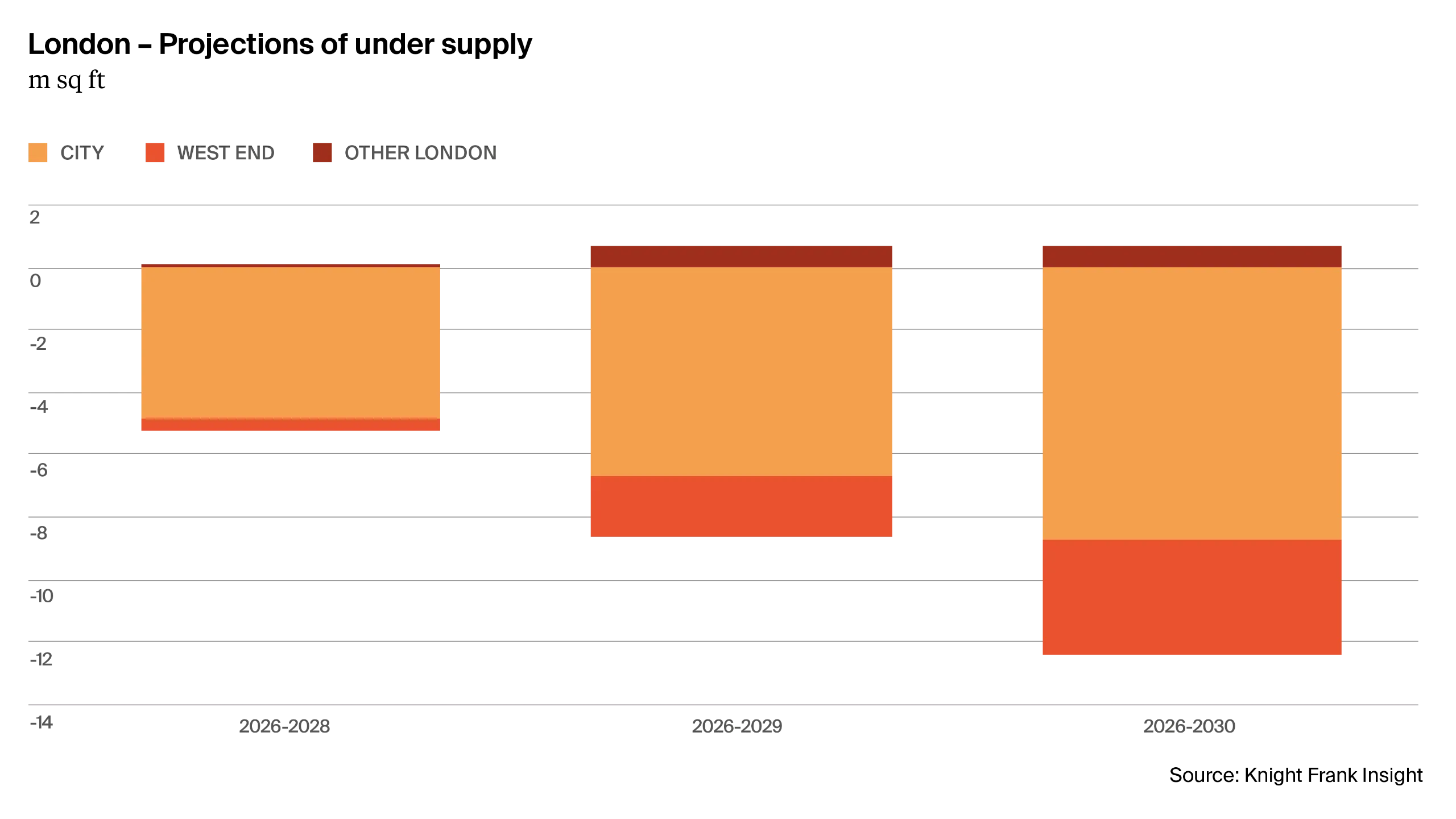

London is moving into a period where scarcity will define the office market.

Over the coming years, the pipeline of best‑in‑class space falls well short of what the market will require. By 2026-2028, London is projected to be undersupplied by around 5.2m sq ft, rising to 8m sq ft by 2029, and reaching as much as 11.6m sq ft by 2030 as demand continues.

High construction costs, planning friction and stringent occupier requirements mean new space cannot appear quickly enough to soften the market. The result is rental growth that is less cyclical, less fragile and far more predictable – naturally reducing leasing risk for investors.

Figure 2: London- Projections of under supply

Time to reset the hurdle

There is a growing argument that traditional real‑estate hurdle rates – borrowed from cycles defined by cheap debt and abundant supply – no longer reflect market reality.

The conditions that once justified high target returns have changed and applying them risks mispricing today’s opportunity set. This reset is occurring alongside broader shifts in capital markets. Against this backdrop, high‑quality offices in structurally constrained global cities offer income visibility and capital preservation that compares favourably on a risk‑adjusted basis.

If supply remains limited and rental growth less volatile, the rational response is a recalibration – recognising downside risks have narrowed while income resilience has strengthened. For investors, the reward is clear: a market where disciplined delivery supports rental performance, downside protection is enhanced, and hurdle rates evolve to reflect a more balanced, durable investment landscape.

Implications for the market

The next phase of London’s office cycle will be shaped by structural scarcity rather than cyclical exuberance.

The market is moving decisively toward a regime where high‑quality space remains chronically undersupplied, which will stabilise rental growth. In previous cycles, surges in speculative supply often pushed rents into sharp reversals, but the current backdrop limits the risk of overbuild. Investors can expect a market in which leasing risk is lower, growth is steadier and volatility is reduced.

Playbook for market participants

Planning and procurement lead times now consume a larger share of the development process, meaning projects that move first will deliver into the tightest supply.

Commit with clarity: Excessive optionality can dilute outcomes where well defined strategies benefit from consistency and follow through.

Specify for performance: Occupiers are choosing buildings based on energy efficiency, amenity and digital capability, so assets that don't meet these standards will fall behind quickly.

Target reversion: Capturing embedded upside through lease events will become a critical lever for returns, particularly for Core Plus strategies.

Rethink hurdle rates: Applying historic targets to a market with lower volatility and tighter supply may lead capital to overlook the cycle’s strongest opportunities.

The outlook

London enters this cycle from a position of quiet but accumulating strength.

Jobs growth is set to outpace every major European peer, capital continues to flow back into the city, and the supply of best‑in‑class space is tightening just as occupier needs become more demanding.

The combination of subdued delivery, deep demand and moderating macro volatility points toward a multi‑year period where rents rise steadily, income remains resilient and risk‑adjusted returns exceed those of previous cycles.

This is a more disciplined, more durable and ultimately more investible phase – one where early movers will benefit most. For investors and developers willing to align with this new reality, the coming years offer something increasingly rare: a market where the fundamentals are improving with unusual clarity.

Read the full paper

Access all the details from Insight 4 in The London Series 2026.