Product: Building at the limits

London’s office market is shifting from a race to build more to a race to build what truly works. The city is not short of demand – it is short of deliverable, future-proofed workspace.

London’s office market is shifting from a race to build more to a race to build what truly works. The city is not short of demand – it is short of deliverable, future-proofed workspace.

Rising costs, planning friction and a rapid shift in occupier expectations have created a development landscape where only the most resilient schemes break ground.

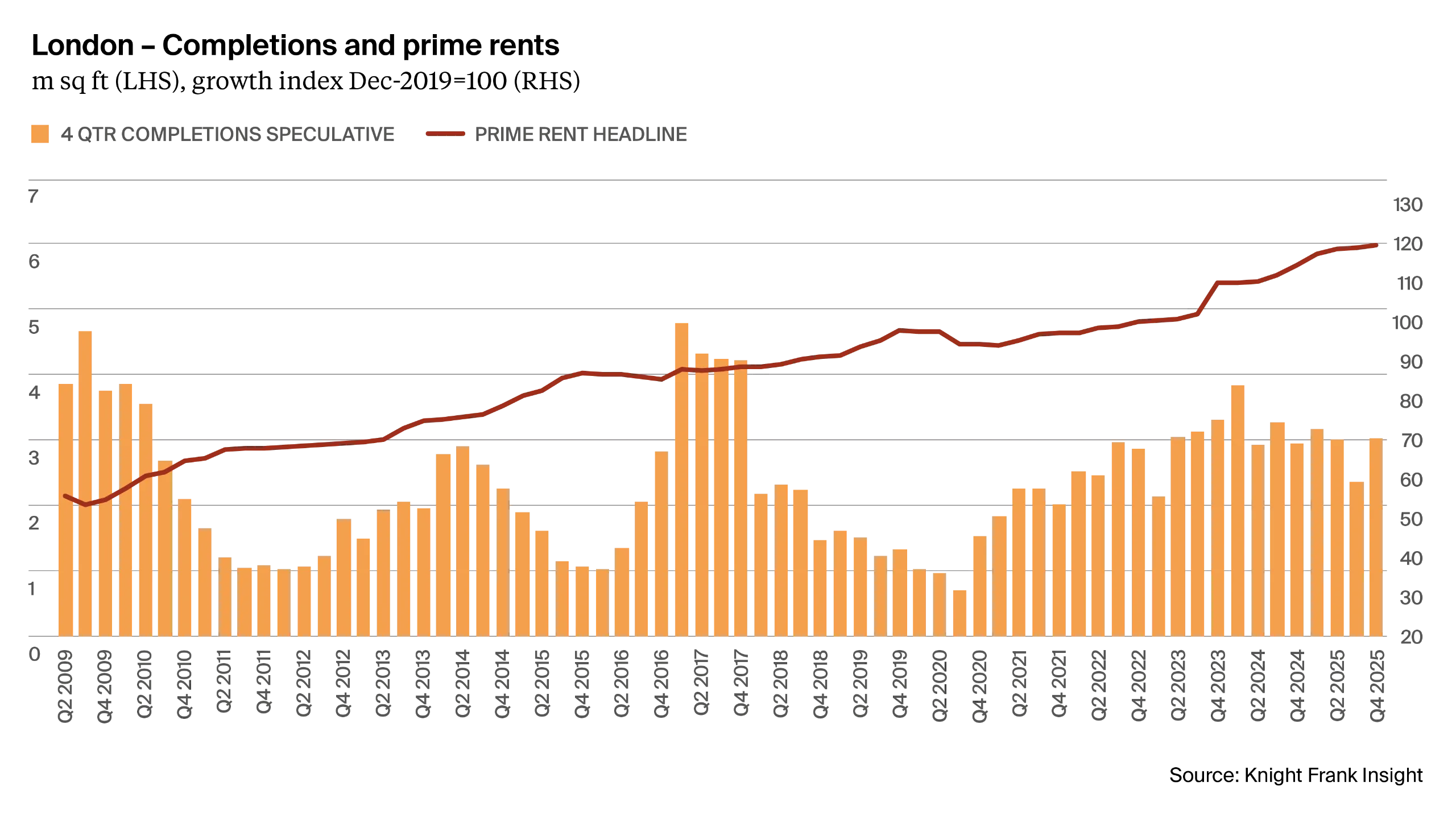

Demand has been robust, seeking low-carbon, high-amenity, digitally capable buildings, while supply has been stuck in a lower gear. Since 2019, there has been 36.1m sq ft of new and refurbished take-up whilst completions have only tallied 27.6m sq ft.

This structural shift in better quality lease-up has resulted in vacancy rates in the City Core and West End Core submarkets below 1%. Developers who can deliver certainty, not just ambition, will define the next cycle.

Demand remains strong for future-proofed, high-spec workspace, but delivery is constrained by high costs, planning friction and financing hurdles.

Best-in-class offices combine technical performance with hospitality-driven amenity and flexibility. Older stock cannot meet these standards.

Development volumes will remain lower than previous cycles, but projects that proceed will be more resilient and valuable.

Product is one of four variables in the London Equation, our framework for understanding how the city competes.

London’s office development market has moved from a period of growth to one of structural constraints.

Rising costs and higher financing rates have reshaped viability, creating a market where demand is concentrated in prime space, amenity rich schemes in high connectivity locations – but delivery remains muted.

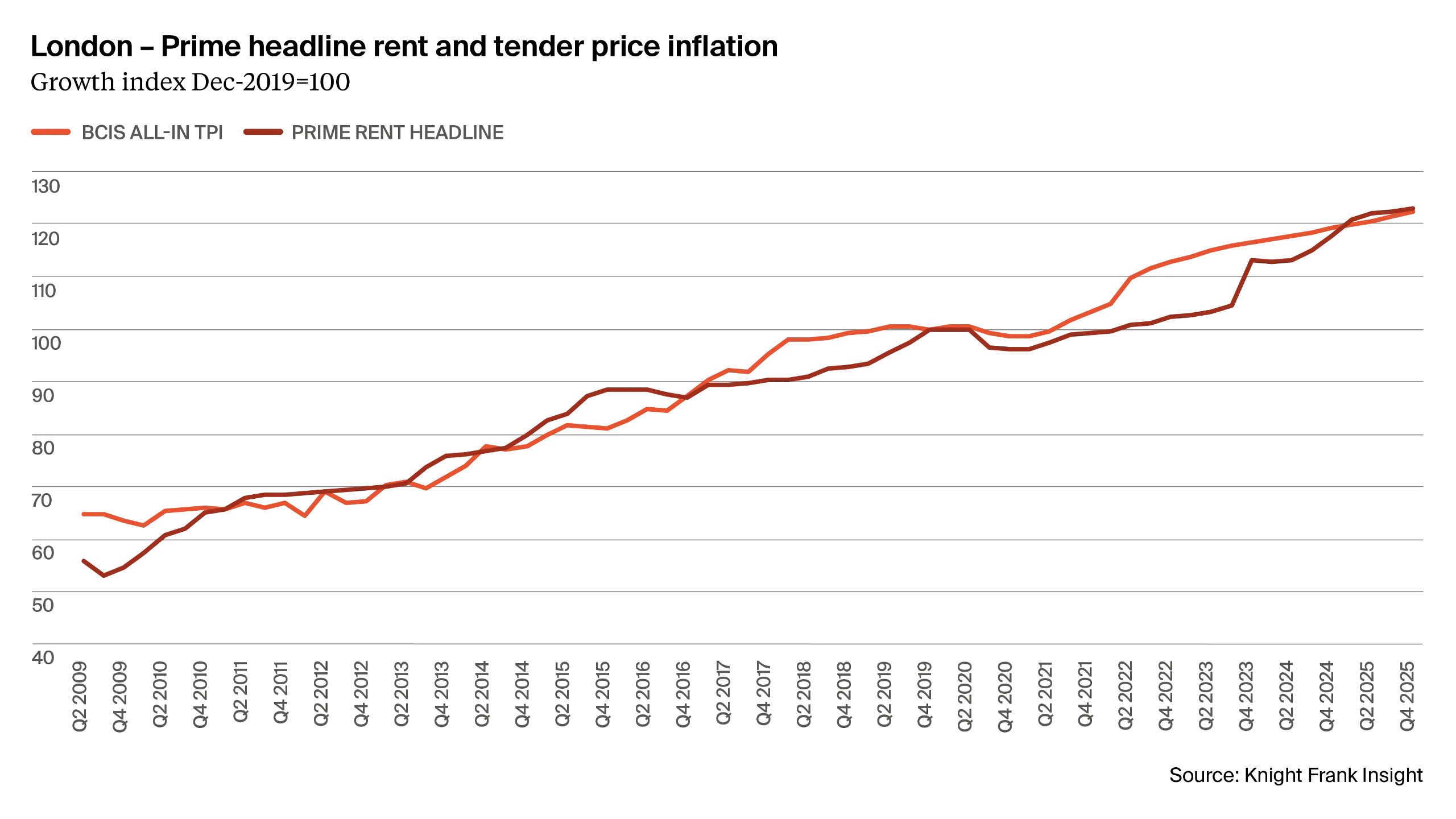

Construction costs have been a major headwind. The BCIS All-In Tender Price Index has risen by nearly 20% since 2020, reflecting higher labour costs, volatility in material prices, and compliance requirements including planning led interventions.

Fit-out costs have also escalated sharply. Cat A fit-out, which provides a landlord-ready base, now ranges from an average of £70 per sq ft, compared to £40-£50 per sq ft five years ago.

Prime headline rents in the City Core have grown strongly, from £72.50 per sq ft in 2019 to £102.50 per sq ft in 2025 (+41.4%), whilst in the West End Core they have grown from £115.00 per sq ft to £185.00 per sq ft (+60.9%).

Historically, such rental growth would have triggered a surge in speculative development. However, development completions have been more modest – at an annual average of 2.4m sq ft across the capital – broadly in-line with historic averages.

Rental growth has occurred during a period where the composition of leasing activity has changed. New and refurbished space now accounts for over two-thirds of total take-up, reflecting occupiers’ preference for high quality new workspace.

This means demand is concentrated in the very product that is most expensive to deliver – a tension that defines today’s market.

Financing costs have compounded the challenge.

Policy rates rose from a low of 0.10% in Q1 2020 to a peak of 5.25% in Q2 2024, compared to an average of 0.51% in the previous cycle. Similarly, five-year swap rates, a benchmark for development loans, averaged 1.5% during the 2010s, climbing from a low of 0.19% in Q2 2020 to a peak of over 5.0% in Q3 2023.

Higher rates mean higher borrowing costs and tougher viability tests. Even strong rental growth cannot fully offset the drag from expensive debt and heavier discount rates. The pool of buyers for completed office buildings is also smaller as debt driven buyers struggle to service loans with rental income.

Planning has evolved into a longer, more tightly sequenced corridor that slows delivery and compresses development windows.

Major schemes often take 12-18 months from submission to consent, compared to 6-9 months a decade ago. Pre-application cycles now require multiple rounds of design revisions to address sustainability, heritage, and community impact. Technical scrutiny is deeper than ever. Energy performance, embodied carbon, biodiversity net gain and fire safety compliance are now core planning tests.

Post‑Grenfell, planning policy tightened around façade and cladding materials, requiring far more stringent fire‑safety compliance. Schemes in or near residential buildings now face heightened scrutiny on fire separation, escape routes and building interfaces, increasing design and regulatory requirements.

This all adds cost and time, and while months are absorbed navigating successive technical gateways, the economic context can shift materially.

A majority of future supply is refurbishment-led (52.3%) reflecting carbon priorities and cost realities. Retrofit is London’s future strength, but a retrofit-first pipeline is not enough. A significant share of older buildings cannot meet the structural, spatial or ESG performance standards that modern occupiers require.

There are signs of improvement. Cost inflation has moderated from its 2021– 2022 peak, and tender price inflation is running at low single digits. Policy and swap rates have begun a downward trajectory from their 2023 highs. If these trends persist, conditions for development will improve.

There are reasons for optimism from a planning standpoint, too. The City of London Corporation has materially increased the volume of higher‑level planning consents despite a more demanding regulatory backdrop.

This has not reflected looser scrutiny, but a more strategic and action-oriented planning approach, supported by the emerging City Plan 2040 and a comprehensive sustainability guidance framework.

Around half of approved space is already moving into construction, signalling that the City has been able to convert planning momentum into delivery more effectively than most London authorities. The resulting pipeline is highly selective – skewed toward large, premium schemes with strong sustainability credentials – but it demonstrates that significant scale can still clear the system.

Despite this improvement, the forward supply position remains structurally tight. An under‑construction and likely speculative delivery programme of just under 5.0m sq ft over the next five years equates to only around 50% of forecast occupier take‑up over the same period.

In contrast, Westminster remains a net drag on office capacity. Policy and practice prioritise heritage protection, townscape preservation and mixed‑use balance, which dilutes office outcomes via change‑of‑use to residential, hotels and cultural uses. Conservation area and listed‑building constraints narrow the scope for height, massing and deep structural upgrade, pushing schemes toward boutique refurbishments rather than larger scale redevelopment.

The supply consequence is negative. Unlike the City, Westminster has not materially grown its Prime and Grade A base through planning. For occupiers, this means reduced choice, slower delivery, and a mismatch between modern workspace requirements and what the borough can realistically bring forward.

Occupier demand has undergone a fundamental reset. Best-in-class offices today are defined by a blend of performance, experience and flexibility that older buildings simply cannot match.

These buildings deliver lower operational energy use, higher air quality and thermal comfort, all electric MEP systems, and embedded smart-building infrastructure that supports real-time optimisation. They pair this technical performance with hospitality-driven amenity – terraces, wellness facilities, collaboration zones, high-quality food and service offerings – that support culture and talent retention. They are also inherently flexible, with efficient floorplates, resilient risers, robust digital infrastructure and future-proofed layouts that allow occupiers to evolve space as working patterns shift.

London is now structurally undersupplied in this category, reflecting an imbalance between what occupiers seek and what London can deliver.

It is likely London will build fewer offices in the coming cycle, but the buildings that emerge will be higher performing, more resilient and more valuable. Scarcity will support rental strength at the top end, while ageing and non-compliant stock faces accelerating obsolescence.

After four years of costs outrunning rents, the viability equation is finally shifting. The turning point is from rents rising faster than cost inflation, narrowing the gap from above. This reflects a structural improvement in development economics as rental growth accelerates while cost inflation remains contained.

The next phase of London’s office cycle will be defined by scarcity rather than oversupply.

Structural constraints on delivery mean the volume of new, high-quality office space will remain limited even as occupier demand continues to concentrate at the top end of the market. As a result, vacancy compression is likely to persist in prime submarkets, with letting risk lower for well-specified buildings in strong locations. For secondary and non-compliant stock, functional obsolescence, rising capex burdens and weaker liquidity will accelerate value divergence.

This cycle will reward timing and scale. Projects that can navigate planning early, lock in specification and move decisively into construction will deliver into the period of strongest rental tension.

Start earlier and commit sooner: Schemes that enter early are better positioned to withstand economic volatility and deliver into constrained supply windows.

Design for demand concentration: Buildings that cannot meet occupiers’ ESG, wellness and digital expectations will struggle to compete, regardless of location.

Recalibrate viability metrics: Economic rents should be assessed in the context of structural scarcity, not historic averages.

Be selective on retrofit: Capital should be directed toward assets that can meet modern standards without disproportionate intervention.

Lean into disciplined speculation: High-conviction speculative development now offers asymmetric upside as leasing velocity and rental growth outpace delivery.

Delaying decisions narrows choice: Pre-letting earlier in the development cycle may be the only way to secure best-in-class space on preferred terms.

London is not running out of demand – it is running out of the buildings demand wants.

While development volumes will remain lower, the projects that do proceed will be higher-performing, more resilient and more valuable. Economic rents are turning decisively upward as rental growth begins to outpace cost inflation, improving viability without relying on a return to ultra-cheap capital.

The next cycle will belong to those who recognise that conditions are quietly but materially improving – and act on it.

Developers who start early will deliver into a market characterised by constrained supply, strong occupier hunger and supportive rental dynamics. In this environment, certainty of delivery is the ultimate competitive advantage.

Access all the details from Insight 3 in The London Series 2026.

Sorry!

An unexpected error has occurred.

Please try again later.