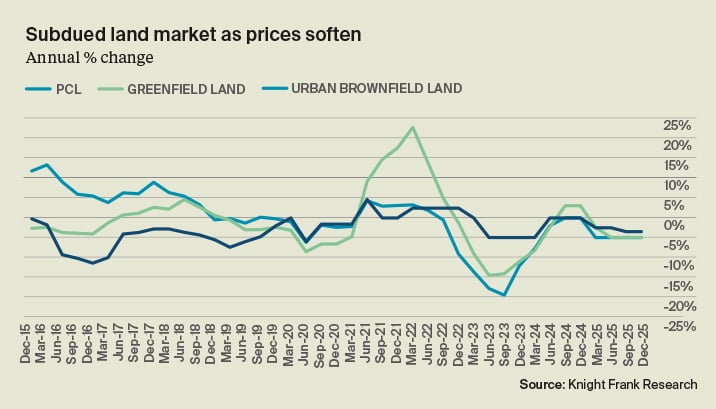

UK residential development land values remained flat through the final quarter of 2025. Uncertainty ahead of the November Budget, subdued buyer demand amid elevated mortgage rates, a restrictive planning and regulatory environment, and limited grant funding for registered providers continue to weigh on developers’ appetite for land.

Urban brownfield and greenfield land values fell by 5% over the course of 2025, while values in prime central London declined by 3%.

Government borrowing costs stabilised following the November Budget, which paved the way for mortgage rates to ease through January. Fiscal measures announced in the Budget should cause inflation to undershoot the Bank of England’s November forecasts, the BoE said in February, which should enable mortgage rates to ease further as the year progresses.

This has lifted sentiment among developers and housebuilders, with tentative signs of a recovery in appetite for land emerging through December and January. The prevailing view is that Q4 will mark the bottom of the market, though any recovery will hinge on borrowing costs easing further, alongside renewed government efforts to reduce planning and regulatory hurdles and the introduction of a support scheme for buyers at the foot of the property ladder.

Land acquisitions

Housebuilders in the suburbs and countryside face fewer headwinds than those in urban locations. The grey belt policy is fuelling land acquisitions, for example. Clearer guidance on the redevelopment of lower-quality sites within the Green Belt has brought forward opportunities in sustainable, well-connected locations that had previously been difficult to progress.

Large cities, particularly London, face unique challenges. However, development data confirms a tentative recovery in activity, though improvements are coming from a historically low base. Work started on nearly 2,300 private homes in the final three months of the year, according to Molior – that’s up from 986 in Q3, 882 in Q2 and 1,385 in Q1. London has an annual housing target of 88,000 homes yet private starts are down 84% in a decade, from 33,782 at the peak of the market in 2015 to just 5,547 last year.

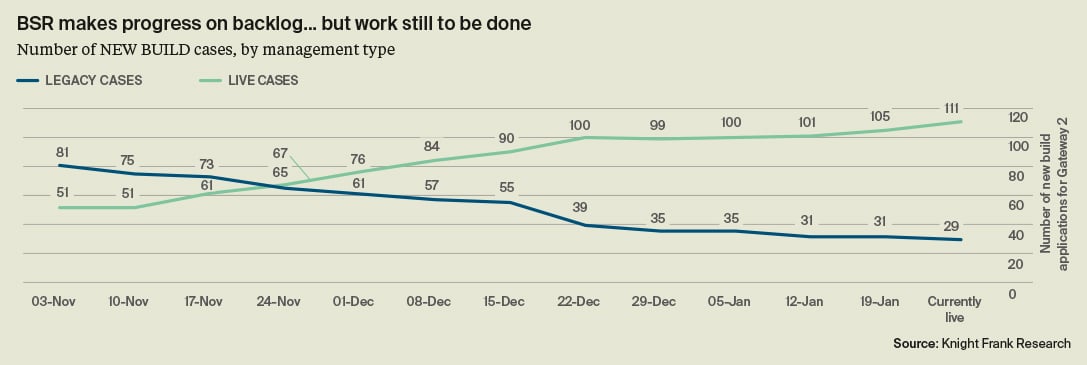

The government’s policy agenda has so far been positive, though it has largely focused on supply-side measures. Increases in technical staff at the Building Safety Regulator have started to ease delays in the Gateway 2 process, though it still adds significant uncertainty. Amendments to the Planning and Infrastructure Bill announced in October may limit opposition to residential projects, while larger sites may soon be subject to a new fast-track process. The Greater London Authority has consulted on cutting affordable housing thresholds and easing some of London’s many prescriptive design requirements, with a decision expected in the coming months.

Many of these changes will help to varying degrees, but they are unlikely to be enough to enable delivery to hit the government’s targets. A meaningful increase in delivery will hinge on cutting into the risks presented by the planning system, particularly an overhaul of the late-stage review process. And while leading fixed rate mortgages should drop below 3.5% by spring, which will improve affordability at the margins, a targeted buyer support scheme would do much more to unlock development. The promised increase in grant funding for affordable housing providers should also be ringfenced to ensure it is directed towards expanding the supply of affordable homes, rather than being absorbed by balance sheet repair or legacy issues at registered providers.

If the government acts on these issues, the early months of 2026 will provide early-cycle opportunities to purchase land at subdued values.

Buyer sentiment

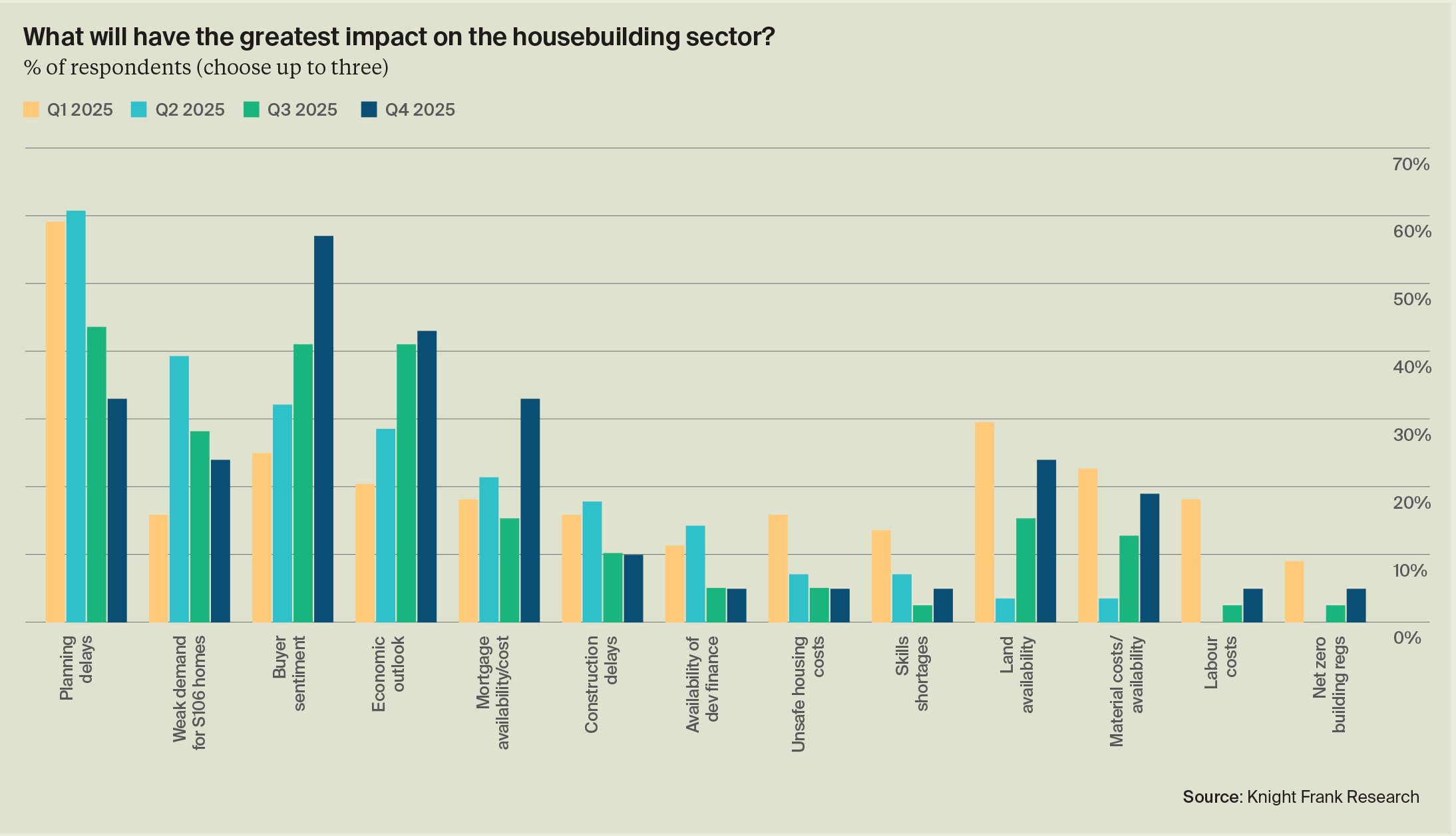

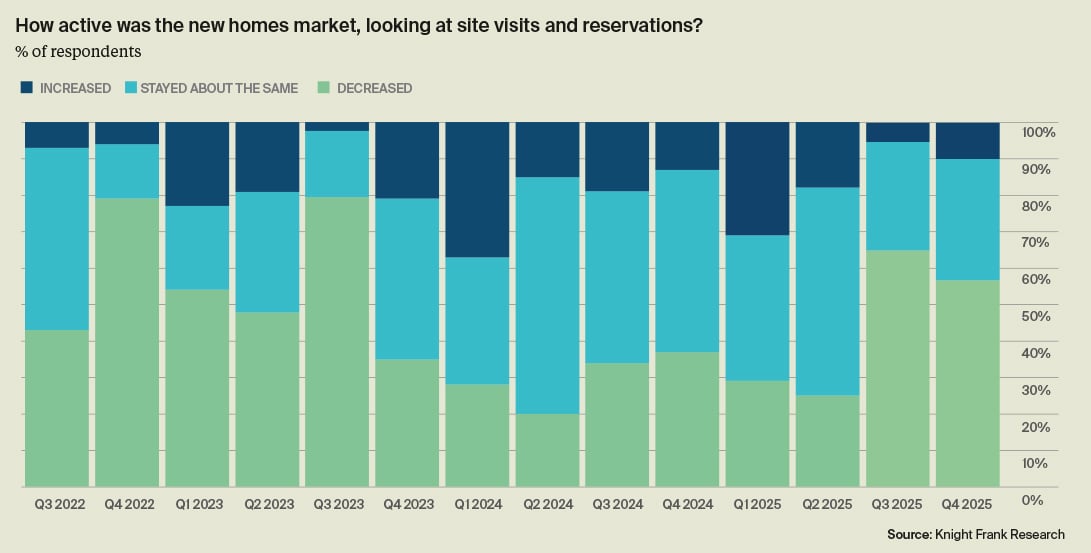

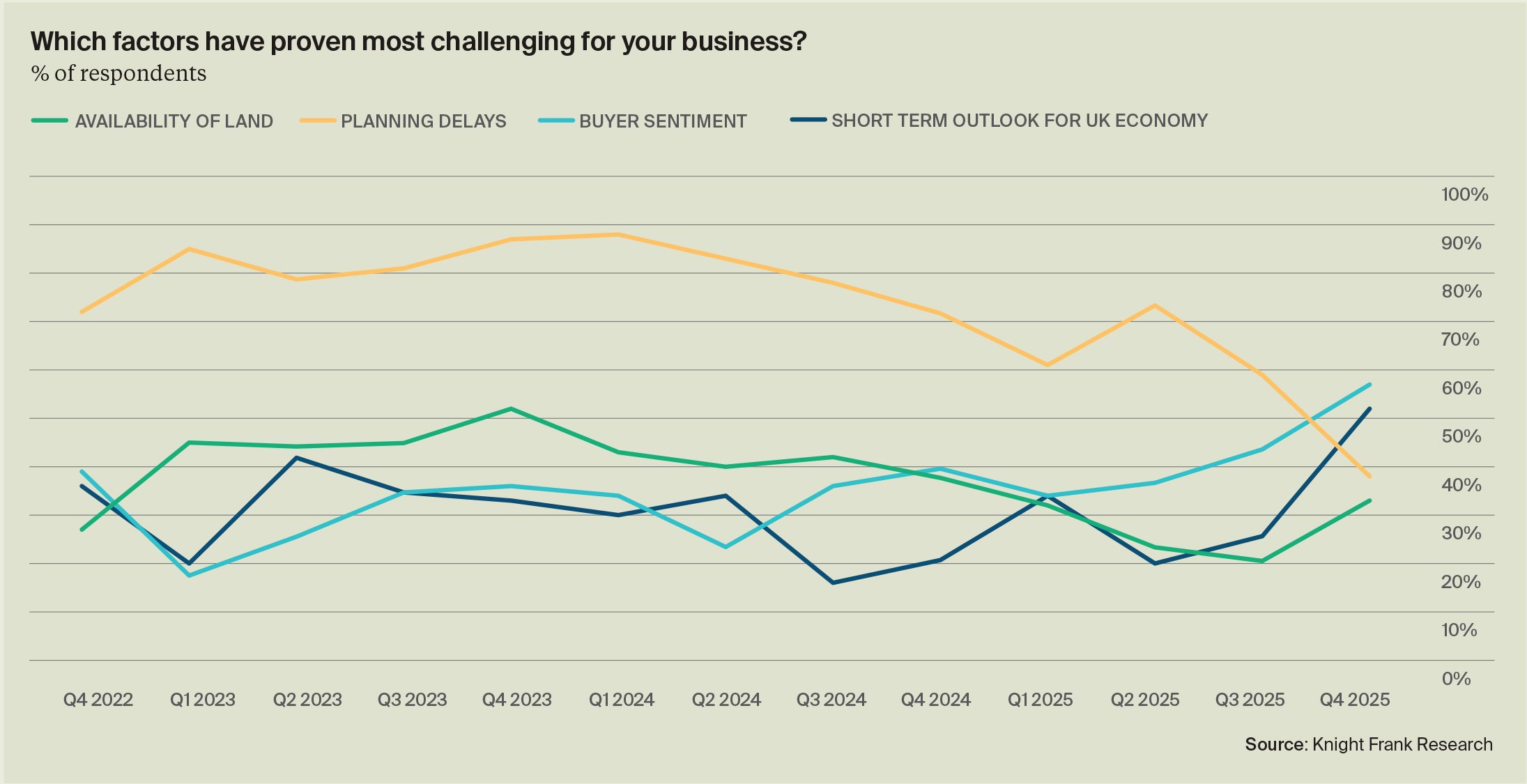

Some 57% of respondents to Knight Frank’s quarterly survey of small and volume housebuilders said site visits and reservations declined during the final quarter, compared to less than 10% that registered an increase. A third said there was no change. Buyer sentiment, the short-term outlook for the UK economy and planning delays were cited as the most significant constraints during the quarter.

Almost half of respondents reported that land supply was constrained, with many site owners unwilling to transact at price levels that would support development viability.

Emergency measures to unlock development announced by the Greater London Authority in October, which include a fast tracked planning route for sites that provide at least 20% affordable housing on private land, are likely to be ‘largely ineffective’, according to 44% of our respondents. The same proportion said they will help at the margins, without being transformational. A little more than 10% said they would be very effective.

Developers expect the challenges through Q1 to remain largely the same; buyer sentiment, the UK economic outlook, mortgage availability and costs and planning delays were the most common choices. Still, the survey confirms a tentative recovery in sentiment; nearly 30% expect reservation volumes to improve through Q1, 57% expect no change and just 14% expect weaker demand.

Buyer support

This points to a modest uplift in development activity. More than half of respondents expect to start more homes than in the previous quarter, 43% anticipate no change, and fewer than 5% expect to scale back activity. Still, nearly half expect land values to remain static through Q1, while 38% expect further easing. We also asked respondents to rank factors that were most likely to increase their appetite for land and development. More First Time Buyer support was the clear priority, followed by interest rate cuts, planning reform and further falls in land values.

The government has signalled it will make further adjustments to housing policies. In January, housing minister Matthew Pennycook told the Financial Times that there were “live discussions in government about what we might do” to stimulate demand. That comes a month after the government began major consultation on a revamped National Planning Policy Framework. Developers would most like to see a permanent presumption in favour of suitably located urban development, followed by measures to make it easier to bring forward small sites and streamlining local standards to speed up plan production.

Overall, the picture at the turn of the year is one of stabilisation rather than meaningful recovery. Pricing appears to have found a floor, sentiment has improved modestly, and activity is beginning to lift from very low levels. However, the pace and durability of any upturn will depend on further easing in borrowing costs and tangible progress on planning reform and buyer support.

In the absence of these, land markets are likely to remain subdued, with selective opportunities emerging rather than a broad-based recovery.