UK Student Market Update - Q4 2025

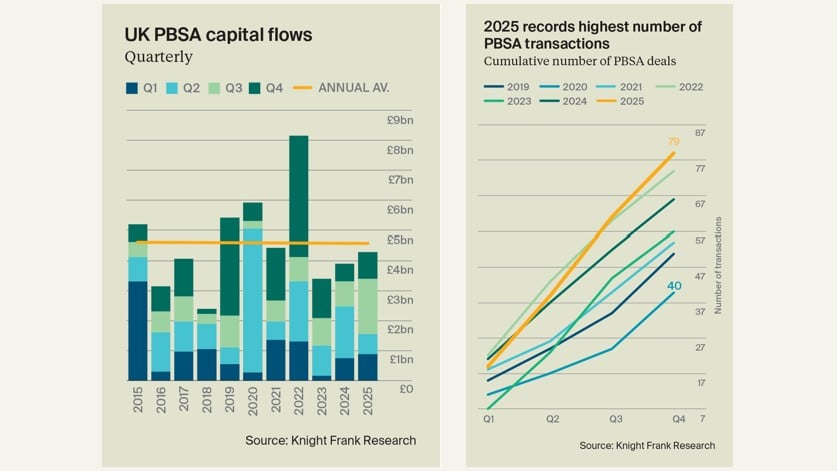

Investors committed £4.3 billion to the PBSA market in 2025, up 10% year-on-year.

Investors committed £4.3 billion to the PBSA market in 2025, up 10% year-on-year.

Investors spent nearly £880 million on UK purpose-built student accommodation (PBSA) in the final quarter of 2025, taking annual investment to £4.3 billion, up +10% year-on-year, and just shy of the long-run 10-year average of £4.5 billion. Established investors remained the backbone of the market in 2025, but fresh capital seeking best-in-class or first-generation assets with cap-ex potential have deepened the liquidity pool.

A total of 79 deals completed in 2025, a +20% increase on the previous year. However, a higher volume of transactions should not be mistaken for an ‘easy’ investment market. Capital markets intelligence points to misalignments between vendor and purchaser pricing expectations, which in some cases has prolonged deal times. Investor appetite was strongest for first-generation standing stock, particularly where there is potential to deliver value-add returns. Yet the backdrop of a second consecutive weaker leasing cycle for 2025/26, an attractive 10-yr Gilt environment of around 4.50% and share price declines among publicly listed sector participants – such as Unite Group plc falling roughly 30% in H2 2025 – have put returns into perspective for investors.

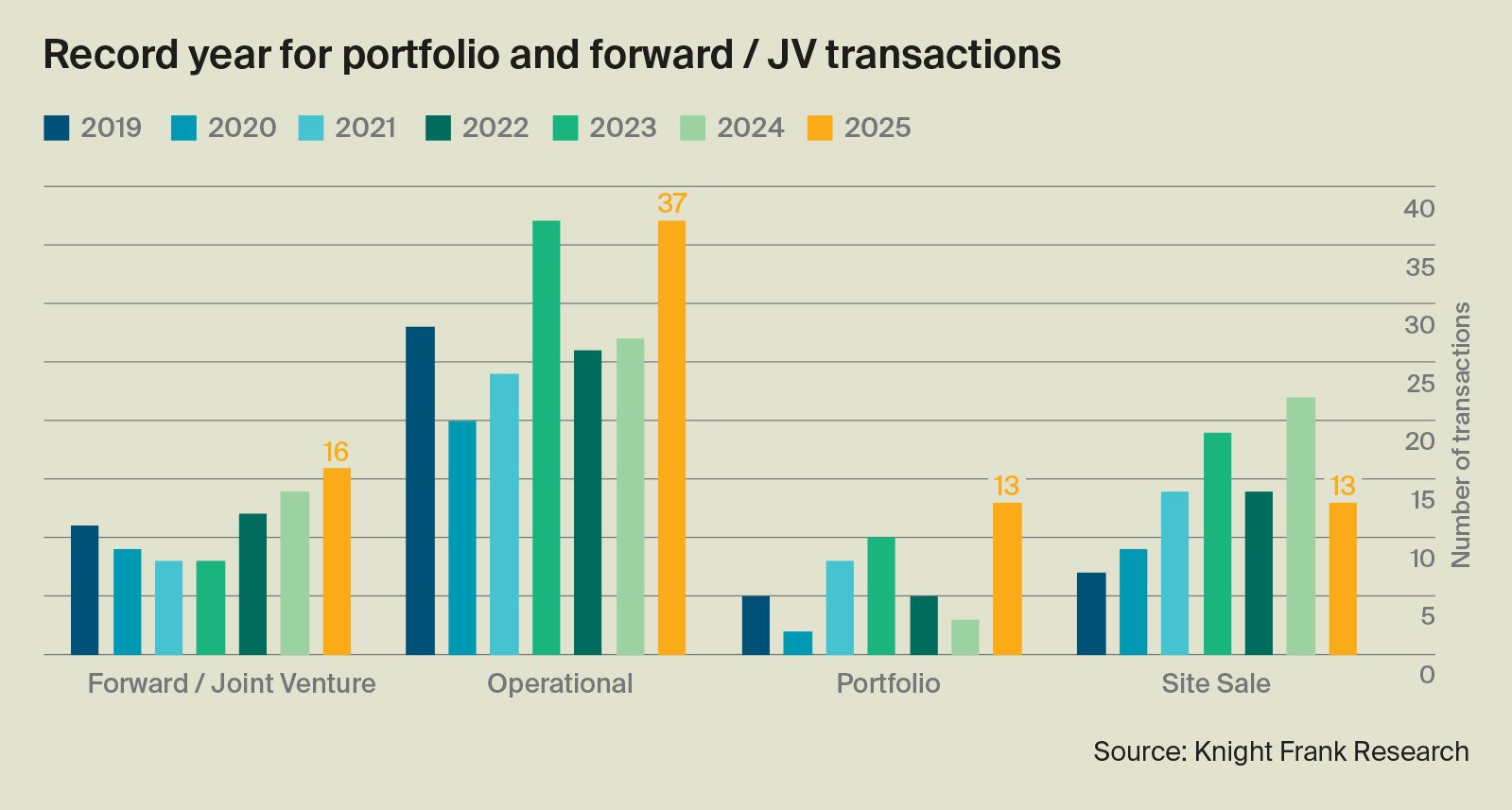

Single asset operational stock accounted for the largest share of investor activity in 2025, consistent with long-term trends, with 37 assets sold. But 2025 also saw a notable resurgence in portfolio level transactions and launches – underscoring investor demand for scale across core-plus and value-add platforms. In total 13 portfolios traded, five of which transacted for more than £200 million.

With operational opportunities finite, investors explored alternative deployment routes. A record number of funding deals and joint ventures took place, accounting for 16 of the 79 total transactions. By contrast, land sales dropped to 13 transactions. A tougher development landscape – with significant delays at the Building Safety Regulator because of Gateway 2, alongside planning and viability challenges – have had an impact on capital allocation.

Despite the operational intensity of PBSA assets, market maturity and a breadth of management platforms enable institutional entry and de-risked operations. The private direct let PBSA market remains highly concentrated, with around 40% of stock controlled by just nine investors, while the remainder is fragmented and fiercely competitive for scale.

In 2026, we expect to see capital chasing expansion. This will be focused on 1) plug and play ability across platforms, 2) composition strength, with a preference for 100% Russell Group exposure and ‘manageable’ asset sizes of 400-500 beds, 3) middle market product offering, appealing to both domestic and international students, and 4) risk adjusted returns; defensive entry points relative to the amount of scale desired, and active asset management to unlock rental reversion.

There have been three key student demand updates in January 2026: 1) UCAS end of cycle 2025/26 data, 2) UCAS January deadline 2026/27 data, and 3) HESA enrolment figures for 2024/25.

1) Who applied 2025/26?

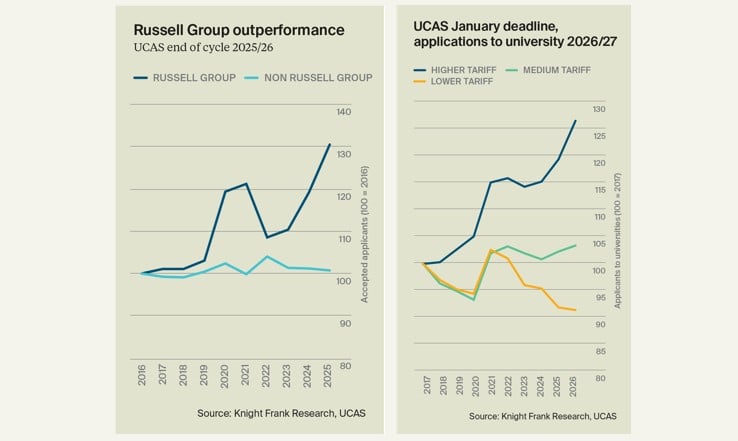

The number of undergraduates accepted onto university courses in the UK for the 2025/26 academic cycle was up by +2.3% year-on-year (YoY), totalling

577,725 students, according to the end of cycle data from UCAS. The number of international student acceptances climbed nearly +8% in the year, while domestic student numbers were up +2%.

Within the headline figures, a familiar pattern exists: Russell Group institutions outperforming, reinforcing a flight to quality for students. Accepted applicants to Russell Group institutions have risen +9% in 2025 and are up +18% since 2023. Growth in international students at Russell Group institutions has been even stronger, with acceptances up +11% year-on-year and +14% since 2023.

2) Who’s applying 2026/27?

As at the equal consideration January deadline, a record 619,360 applications were made to UK universities, a +3% increase from last year. UK students make up the majority of applications at 494,540 (+3% YoY), while international students accounted for 124,830 (+5% YoY). Similar to the 2025/26 end of cycle data, a flight to quality is evident. Some 43% of all UK undergraduate applications were for higher tariff universities, compared to 39% in 2019. On an annual basis, applications were up +6% to higher tariff, +1% to middle tariff, and down -1% to lower tariff institutions.

Applications from Chinese students are up +10% on last year’s deadline, equivalent to an increase of 3,220 applicants. Whilst positive, it shines a light on the growing reliance on China as an international student market – now accounting for 28% of all international applicants, compared 15% in 2019.

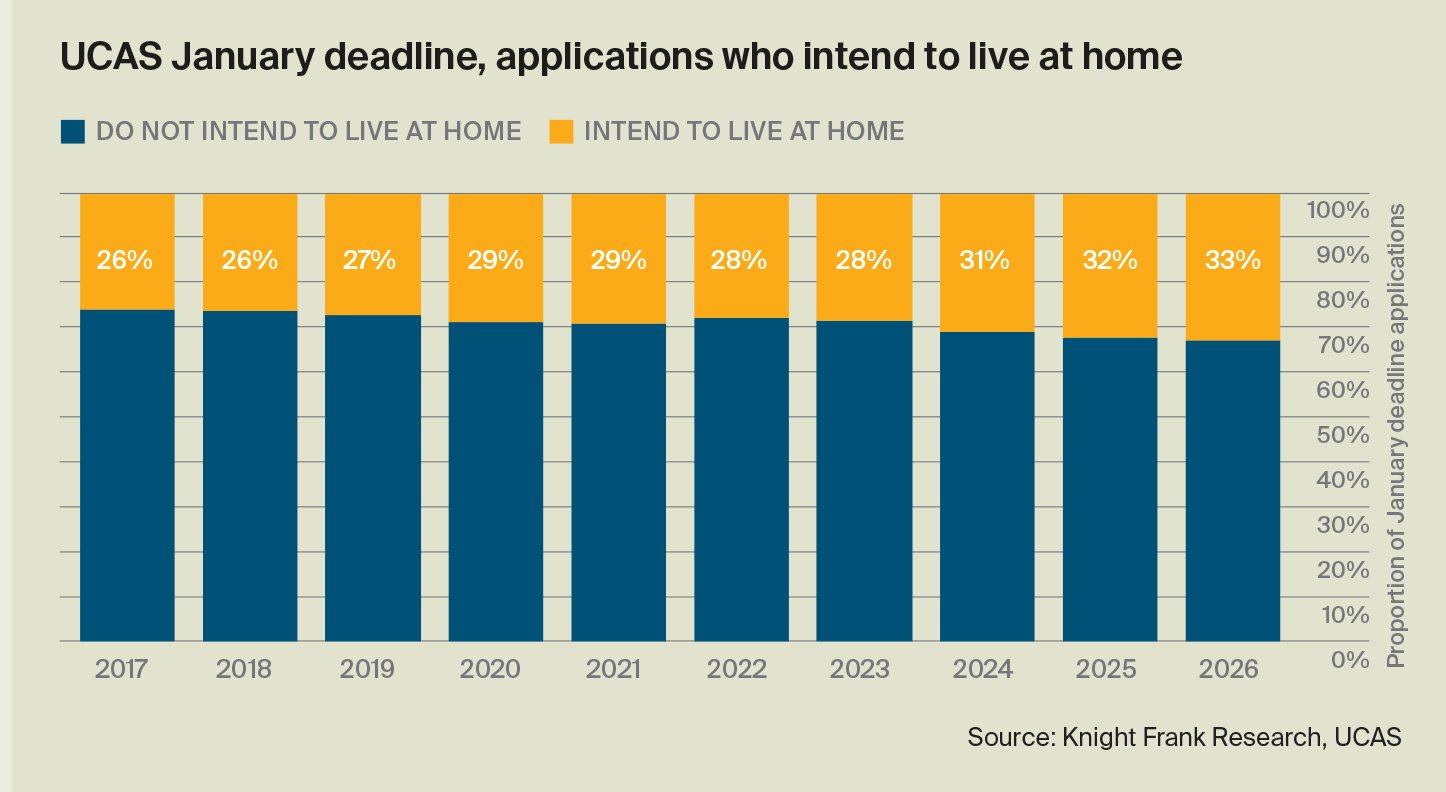

The proportion of January applications that stated they intend to live at home for the upcoming cycle also rose to 33%. While this is not a direct correlation for those requiring accommodation, it can be used as a proxy for wider affordability concerns, and the rise of the commuter student in some locations.

3) Bums on seats 2024/25

There were 2.27 million full-time students enrolled at UK universities for the 2024/25 academic cycle, the latest data from HESA shows, a 0.7% fall on the previous cycle. Within this: undergraduate numbers increased by +1.5%, while postgraduates fell by -7.5%.

UK domiciled students were up +1.8% over the same period, while overseas students fell by -6.6%. It is important to note that HESA enrolment data – despite being the definite picture of student demand in the UK – lags a full academic cycle. As such, it is important to supplement it with more current demand metrics. Home Office international student visa data, for example, points to an 8.8% annual increase in visas granted over the four quarters to Q3 2025. A granted visa does not automatically equate to an enrolment, but it can be used as a proxy for incoming international students in the 2025/26 cycle.

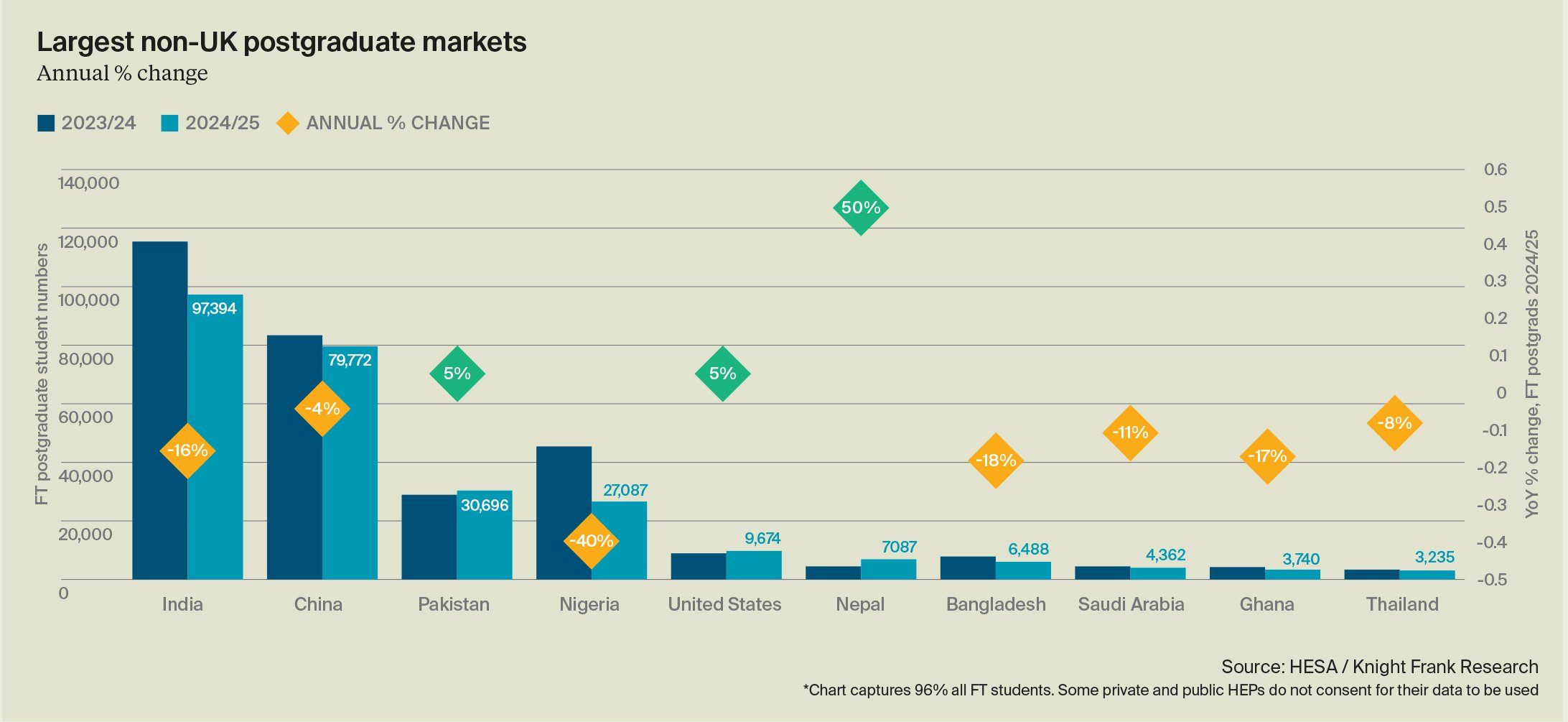

Following the visa dependant rule change in January 2024, international postgraduate numbers fell -11% year-on-year in 2024/25. However, country variation is at play, with large postgraduate markets such as Pakistan and the United States recording +5% growth in the year, while postgraduate students from India and China fell -16% and -4%, respectively.

Of note in the 2024/25 cycle data, is Nepal’s meteoric rise of +50% year-on- year, to just over 7,000 postgraduate students. This is largely linked to changes in international visa policy in competing postgraduate destinations. Australia’s Home Office has moved Nepal, India, Bangladesh and Bhutan to the highest risk category for student visas, meaning students from these destinations are under increased scrutiny. While Canada’s international student caps and increased proof of finances permits are also acting as a deterrent for certain domiciles.

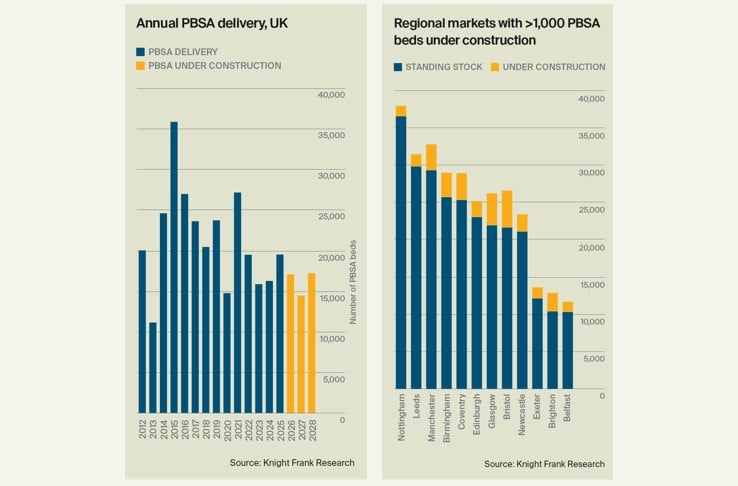

Some 19,600 new PBSA beds were delivered across 64 schemes in 2025, representing a +20% increase on the previous year, albeit delivery remains short of the five-year pre-pandemic annual average of more than 25,000 beds. London saw the highest level of new delivery with 4,350 beds added to supply, followed by Nottingham (2,550), and Leeds (1,900). The private sector continues to play the leading role in providing new accommodation for students, accounting for 90% of all new beds completed last year.

There are an additional 50,250 PBSA beds under construction across the UK. The largest concentrations, in terms of the absolute numbers, are in London (14,600), Bristol (5,000), Glasgow (4,300), Coventry (3,600) and Manchester (3,500), which together account for 62% of all development activity across the UK.

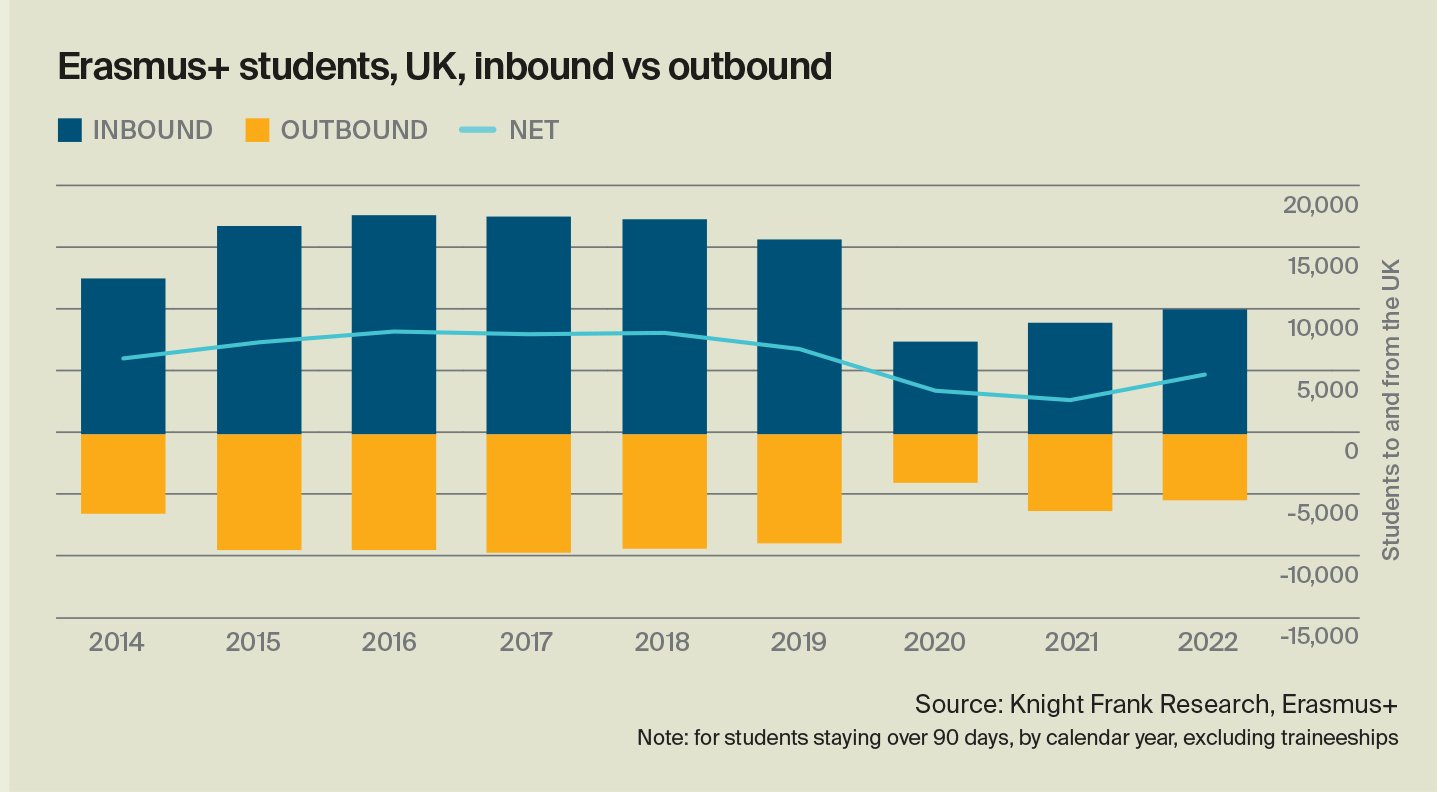

The UK government has confirmed that it will rejoin the Erasmus+ student exchange programme in 2027. The deal allows students to study, or work in UK or Europe for two to 12 months without extra tuition fees, reversing the post-Brexit suspension. Re-entering the programme comes with fiscal implications for the UK, costing £570 million per annum. The previous program cost circa £150 million and funding for Turing Programme in 2026 was £78 million.

At the programmes’ peak, approximately 17,900 students came to the UK and 9,500 left, leaving a net positive figure of circa 8,400 students in the UK requiring accommodation. The primary benefit of rejoining lies in the reputational advantage for UK universities, which will once again be able to market themselves as part of a major European mobility programme. This extends beyond student participation to include staff and research personnel, for whom the scheme also facilitates short-term placements.

Mid-tier universities stand to gain the most, having seen substantial declines in EU student numbers post-Brexit. However, the financial impact is expected to be limited, given the shorter duration of Erasmus+ exchanges compared with full-degree enrolments.

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.