The New Frontier - Your weekly science and innovation update

Your weekly pulse check on science and innovation. Those on the supply side of real estate can track the trends set to drive demand, while occupiers gain fresh perspective on competitor activity and sector dynamics.

29 September 2025

Visa Wars

The US has lit the touchpaper on a new battle for global talent. The Trump administration’s latest salvo imposes a one-off $100,000 levy on each H-1B visa, the lifeline for international scientists, coders and engineers entering the US workforce. Current visa holders are spared and applications lodged before 21st September sneak through unscathed, but the policy direction is plain.

Where Washington slams the door, the UK spies an opening. Keir Starmer’s government has convened a Global Talent Taskforce to position the UK as the world’s easiest landing spot for entrepreneurs, academics and scientists. Radical options are being weighed, from abolishing visa fees entirely for top tier recruits to streamlining applications and even reforming tax regimes. Investors are pushing hard. Harry Stebbings of 20VC described the US clampdown as “Europe and UK’s greatest opportunity”, calling for a fast track to the UK for every displaced H-1B holder.

That message is echoed by the Startup Coalition, which in an open letter urged the Home Secretary to “act boldly, not cautiously”. It called for an expanded Global Talent Fund, rapid visa approvals for H-1B applicants seeking to relocate, and reforms to the EMI scheme that underpins recruitment in high-growth firms. With foreign born entrepreneurs behind 39% of the UK’s fastest-growing businesses, the economic stakes are evident.

Yet the picture is not one of unqualified optimism. At the same moment that government signals openness to skilled workers, it is proposing a levy on international students. Public First estimates that a 6% surcharge would trigger a fee rise large enough to cut demand by 16,000 students in year one and over 77,000 across five years. The financial fallout for universities could exceed £2.2 billion, with research budgets one of the likely casualties. That matters not only for higher education but for the innovation economy that draws talent and ideas from it.

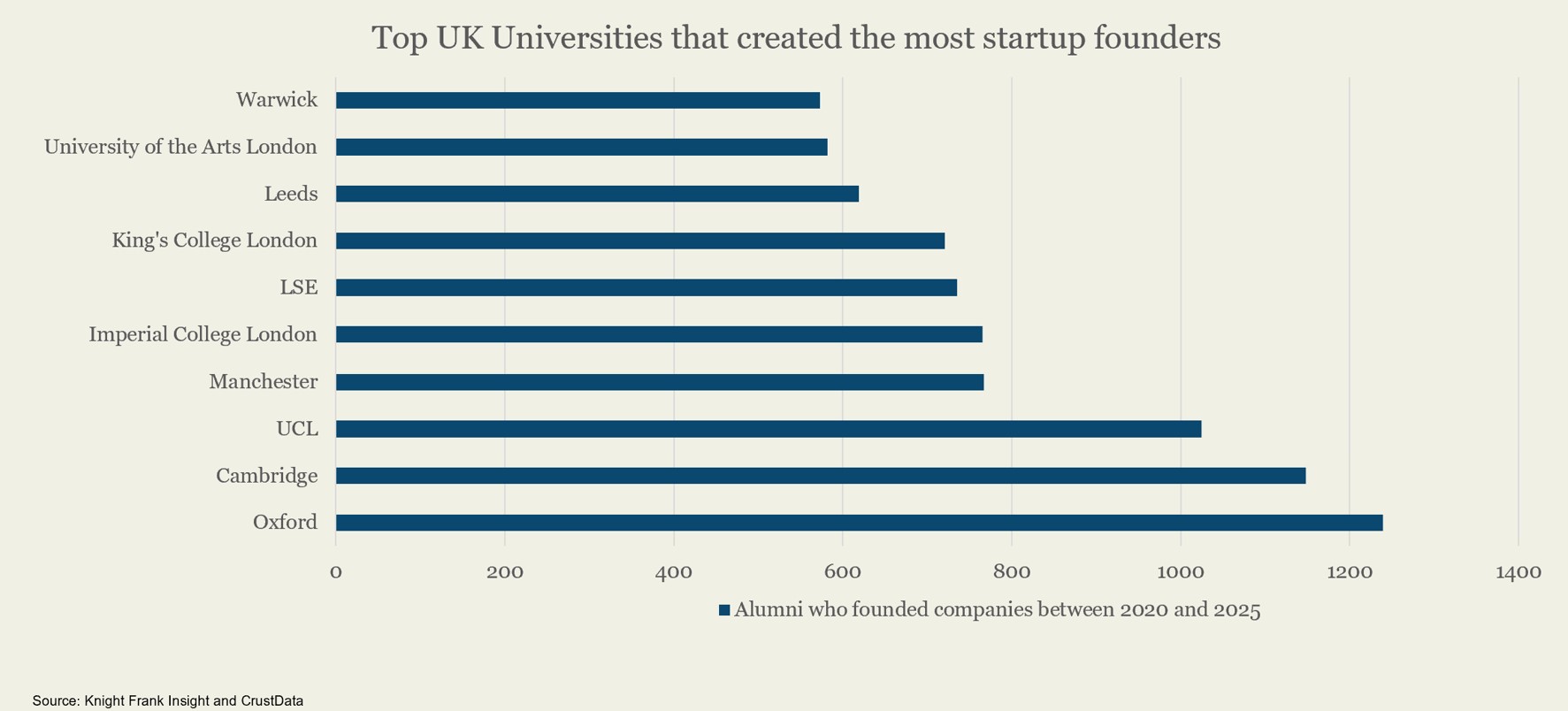

The link between university talent and entrepreneurship is stark. Oxford has produced 1,239 startup founders since 2020, with Cambridge close behind on 1,148 and UCL at 1,024. Manchester, with 767, leads the northern charge, while London’s cluster of Imperial, LSE and King’s College collectively pump out thousands of entrepreneurs. If universities are forced to cut deep, this entrepreneurial pipeline could be choked. Employers sponsoring skilled migrants already face costs approaching those of the US levy, according to Vialto Partners, sharpening questions over competitiveness.

UK Sixth in Global Innovation Index, but its Cities Outperform

Talent links directly to innovation capacity, and here the UK faces both setbacks and bright spots. The WIPO Global Innovation Index ranks the UK sixth worldwide in 2025. The UK still scores strongly on outputs, but others are moving faster. China, for example, has entered the global top 10 for the first time.

At a city level, the story is more upbeat. Four UK clusters make the world’s top 100. London sits eighth, while Cambridge claims second place globally for innovation intensity, fuelled by world leading scientific publishing. Oxford ranks fifth on the same measure, while Manchester breaks into the index for the first time at 94th. These city clusters show how innovation often concentrates in specific places, shaping the geography of opportunity.

The report also provides a useful update on conditions in science and innovation. When it comes to venture capital deal values rebounded modestly in 2024, but this recovery was highly concentrated in US megadeals and AI related sectors. Deal counts have declined for a third consecutive year.

Research output has surged to record highs. Nearly 2 million scientific publications were published in 2024. China and India were key growth drivers. The UK grew by 3% compared to 14% for China. Publications remain the only innovation metric growing above the long-term trend, underlining the resilience of the global research base.

International patent filings grew slightly, reversing a rare decline in 2023. There is regional disparity though. China and Korea increased filings, while the US, Japan, and Germany all reported declines.

Corporate R&D reached a record $1.3 trillion in 2024. However, growth in nominal terms slowed to 3.2%, or 1% in real terms. Despite representing a historic peak in absolute terms, this marks the lowest annual nominal growth in corporate R&D spending since 2010.

The contrast is sectoral. Software, ICT, and pharma/biotech firms are increasing investment (with double-digit growth in some cases). Automotive, consumer goods, and traditional manufacturing have cut back due to weaker revenues.

Further Context to Pauses in Big Pharma Investment

These global shifts are not abstract. They feed directly into corporate decision making, and in recent weeks the UK has been feeling the strain. The Science, Innovation & Technology Committee summoned pharma executives to explain why projects were being paused or cancelled. MSD’s Ben Lucas pointed to a $3 billion global restructuring and a portfolio pivot away from early discovery in London.

“The decision has been long, a fair while in the making. I would say the reality is, our company is going through a significant strategic shift as we reach the end of a period of time where we've been quite focused in two areas of business, in oncology and in vaccines… as we look to the future, we have a really exciting portfolio.”

He added, “The company is engaged in and publicly declared a $3 billion restructuring that was going to happen globally… We also talked about assessing our global footprint. As part of that assessment, my research lab colleagues have made the decision that, in terms of the early discovery research, they would no longer pursue what had been a long-in-the-making investment here in London.”

“So, it's a multi-factorial decision, a difficult decision. It hasn't been made easily, and we're very conscious of the impact it has on our people and the economy, both locally and in the UK at this moment in time.”

He clarified his points: “We are going to reduce costs from one area of our business and pivot them to new areas of our business. We're not reducing overall investment on a global basis, but it has meant that when you look at our investments in different divisions and different therapy areas, that will change.”

AstraZeneca’s Tom Keith-Roach cited the patent expiry of Forxiga and the UK’s long-standing difficulty in translating approvals into NHS uptake.

The speakers acknowledged that US policy is not the direct cause of recent UK investment decisions, but they are part of the broader international context. Lucas added regarding MSD’s withdrawal.

In response Lord Patrick Vallance, Science Minister, has said “all options” are on the table on drug pricing, underlining that the government knows the stakes. Meanwhile Moderna signalled confidence by opening a £150 million Oxfordshire vaccine facility, part of a £1 billion partnership with the UK government. Darius Hughes of Moderna said that the company would continue to invest in the UK as part of a £1 billion partnership with the government. “We’re here to invest”. Moderna is investing in vaccines in the UK which do not come under the contested VPAG scheme.

Interlocking factors shaping UK investment decisions:

Pricing and rebate pressure

Undervaluation of innovation

Global competition

Business transformation

Pipeline renewal in response to the patent cliff

Cost and regulatory headwinds

US policy

Scotland’s Prescription for Life Sciences Growth

One frontline for life sciences is Scotland, where the ABPI has outlined a manifesto for growth ahead of possible elections in 2026. It calls for guaranteed fast access to new medicines, reinvestment of industry rebates, and a “data-driven NHS” with a single-entry point for companies seeking to use Scotland’s rich health informatics. The life sciences base is already strong, with over 700 firms and 37,000 employees spread across Edinburgh’s BioQuarter, Glasgow’s innovation zones, Dundee’s MedTech cluster, Inverness’s digital health campus and Aberdeen’s BioHub.

The War for Talent in Life Sciences

Another global challenge confronting life sciences companies is the intensifying battle for talent. Hays’ latest global life sciences talent report finds that traditional R&D and clinical roles are no longer enough, they now demand fluency in data science, cloud computing and predictive analytics. The shift is stark. Fewer than 15% of the global life sciences workforce is considered “AI ready”, and more than a third of workplace skills could be disrupted by 2030. In parallel, 60% of workers will require reskilling to keep pace with digital transformation.

This skills gap is already constraining the scale of digital transformation programmes, and competition from the tech sector makes matters worse, with life sciences companies struggling to attract and retain scarce digital specialists. Responses vary. Many firms are prioritising upskilling and reskilling, adopting more agile hiring models, and partnering with outsourcing providers to access niche capabilities quickly and cost effectively. Structured internships, apprenticeships and graduate programmes are being used to tackle looming succession gaps, while stronger employer branding is being deployed to showcase innovation and patient impact to appeal to young scientists and engineers.

The report also highlights an evolving demand profile. Specialists in strategic partnerships and M&A integration are increasingly sought after to help firms navigate patent cliffs. Expertise in supply chain forecasting, inventory planning and operational resilience is rising in importance as firms seek to withstand disruption. On the R&D frontier, niche skills are gaining traction, from RNA scientists to digital twin engineers. Meanwhile, new hybrid roles are emerging, including regulatory-AI integrators and global policy navigators capable of interpreting complex pricing frameworks, medical device regulations and data sovereignty rules.

There is a well-documented connection between talent attraction, retention, upskilling and productivity, and the real estate that underpins them. The places that provide environments enabling all four will be the ones that come out on top.

Patent Cliff Looms, Generics and Biosimilars Poised to Gain

Big Pharma faces a patent cliff with $200 billion of branded drugs due to lose exclusivity by 2030. For generics and biosimilars, this is an unprecedented opening. Firms from Sandoz and Teva to Sun Pharma and Shanghai Fosun are scaling fast, with pipelines designed to capture market share and revenue. It is also of note that the proposed US 100% tariff on imported drugs does not appear to impact generics (see other quick reads for more).

The top ten players in this space are Sandoz, Teva, Viatris, Sun Pharma, Shanghai Fosun, Fresenius Kabi, Stada, Aurobindo, Dr Reddy’s and Cipla.

- Sandoz (Switzerland) – Spun off from Novartis, Sandoz has reinvented itself as a pure-play off-patent giant, doubling down on biosimilars. It saw double-digit growth in its biosimilars business in 2024, launching new products and expanding others. With 28 biosimilar molecules in development and several under regulatory review, Sandoz is aggressively positioning to capture upcoming off-patent markets.

- Teva Pharmaceutical (Israel) – The world’s largest generic drug maker by volume, Teva is emerging from a few tough years with a renewed focus. In 2024 it grew revenue to $16.5 billion, thanks largely to higher generics sales.

- Viatris (USA) – Formed in 2020 from the merger of Mylan and Pfizer’s off-patent division, Viatris remains a top-tier generics player with $14.7 billion revenue in 2024. The company has been streamlining to focus on core generics and divested other non-core units. That means Viatris is now laser-focused on its pipeline of 250+ generics in development.

- Sun Pharma (India) – The largest pharma company in India, Sun Pharma has a global footprint with 43 manufacturing sites and a broad portfolio of generics and branded generics. Sun saw over 10% revenue growth in 2024, partly by moving up the value chain but also by leveraging its scale in generics.

- Shanghai Fosun Pharmaceutical (China) – Representing China’s growing clout in pharma, Fosun Pharma’s generics and biosimilars business is on the ascent. The firm, part of the large Fosun conglomerate, has dozens of generic drugs approved in China, Hong Kong and the US.

Investment Signals from the world’s Top VC Firms

PitchBook’s Q2 2025 Emerging Tech Indicator (ETI) offers a quarterly snapshot of pre-seed, seed and early-stage investment trends. It tracks a select group of top performing VC firms, which account for around 10% of global venture activity, making it a bellwether for where smart capital is flowing. Key headlines include:

AI still dominates, but the focus is shifting. For the seventh consecutive quarter, artificial intelligence led the pack, attracting $3.3 billion across 41 deals. What stands out is the nature of the bets being placed. Investment is migrating from horizontal platforms towards the application layer. Startups building specialised agents, verticalized AI tools and industry-specific platforms are capturing the lion’s share of attention.

Health tech, climate tech and fintech all posted strong gains. In Health tech, Function Health’s $300 million Series B and PB Healthcare’s $218 million seed round were headline grabs, underscoring continued investor conviction in healthcare platforms blending data, diagnostics and delivery. Climate tech secured $691.8 million in the quarter, with nuclear energy and grid infrastructure the key magnets for capital. Fintech also held firm, chalking up 25 deals, half of them at seed stage, as investors returned to early-stage financial services bets after a slower 2024.

Industrial technologies, which encompass Defence Tech had a breakout moment. The sector recorded a record quarter, drawing $421.5 million across 13 deals. Policy momentum and geopolitical shifts are fuelling investor appetite, with autonomy, resilience and dual-use technologies at the centre of attention. Standout raises included AIM, which secured $91.1 million to advance its autonomous heavy machinery, and Kela Technologies, which raised $88 million to develop its defence system integration platform.

Other quick reads….

A new AI research screening platform dubbed AIR-SP - backed by £6 million in government funding - is being built by NHS England to enable trusts across the country to join trials of AI in screening to help speed up diagnosis. It will offer NHS staff access to AI tools in trials to help analyse screening images and pinpoint abnormalities, including signs of cancer.

Eli Lilly announced plans to build four new manufacturing sites in the US this year, creating 13,000 jobs across construction and production. The move lifts its total US capital expansion commitments to more than $50 billion since 2020. Donald Trump announced on Truth Social that the US will impose 100% tariffs on imports of branded or patented drugs, unless a company is building a plant in the country. This is defined as “breaking ground” and/or “under construction.” It is not clear whether the tariffs impact countries that have brokered specific trade deals.

UK FinTech momentum builds. Revolut has opened a new headquarters in Canary Wharf with an emphasis on showcase spaces as much as desks. Tide became the latest UK FinTech unicorn following a £120 million funding round, while GoCardless is expanding into Leeds to tap northern talent pools. Triver raised £114 million to support £1 billion in annual lending to small businesses, and Fnality secured $134.78 million to extend its sterling payments system into US dollar and euro markets, subject to approval. M&A is also gathering pace, with 70 UK and European FinTech deals completed in the year to June 2025, a 50% increase on the previous year.

London-based Renalytix raised $520.05 million in a PIPE round, building on its IPO. Founded in 2018, the company specialises in AI-enabled clinical decision-support tools for kidney disease, including its flagship KidneyIntelX platform. Renalytix employs 110 people.