UK Hotels Trading Update, H1-2025 – A challenging Market Backdrop

21 August 2025

Despite respectable levels of occupancy growth, the challenging market conditions for the London hotel market continued in Q2, with far greater rate sensitivity. The addition of more than 5,300 new rooms added to London’s hotel supply since the start of 2024, has restricted the growth in occupancy and contributed to the decline in the ADR.

Hotels across all segments have reduced room rates to remain competitive and to support occupancy levels. Shorter booking lead-in times have added further pressure to room rates, as cost-of-living pressures continue to impact discretionary spend and delay travel plans. This led to a decline in revenues across all London hotels, with June YTD recording a fall in RevPAR of 2.5 percentage points.

London’s Luxury hotels recorded the sharpest fall in ADR in Q2, declining y-on-y by more than 7%. Whilst international arrivals from Asia and the Middle East to Heathrow Airport are up y-o-y by 2.2%, the number of US arrivals has been held level, with potentially fewer confirmed bookings attributed to the weakening dollar.

Performance across regional UK was subdued, with a marginal decline in RevPAR overall. Yet different marketing strategies employed, led to mixed messages in performance between the different segments. Nevertheless, the domestic leisure market remains relatively robust, with sporting fixtures and music events continuing to support trading. And the trend for continued experiential travel is clear, with leisure revenues rising y-o-y, leading to June YTD TRevPAR being on par with the previous year.

Golf & Spa Hotels have seen total revenues increase by 4.3% per available room over the same period.

Payroll costs since the rise in the NMW and NIC, in the three-month period April to June, have increased y-o-y by 6.6% PAR across all London hotels and by 4,2% PAR across regional UK. The rise in payroll costs, combined with the fall in RevPAR, has resulted in the share of payroll costs to total revenue rising by more than two percentage points to 28% in London and by 1.5 percentage points to 31% across regional UK.

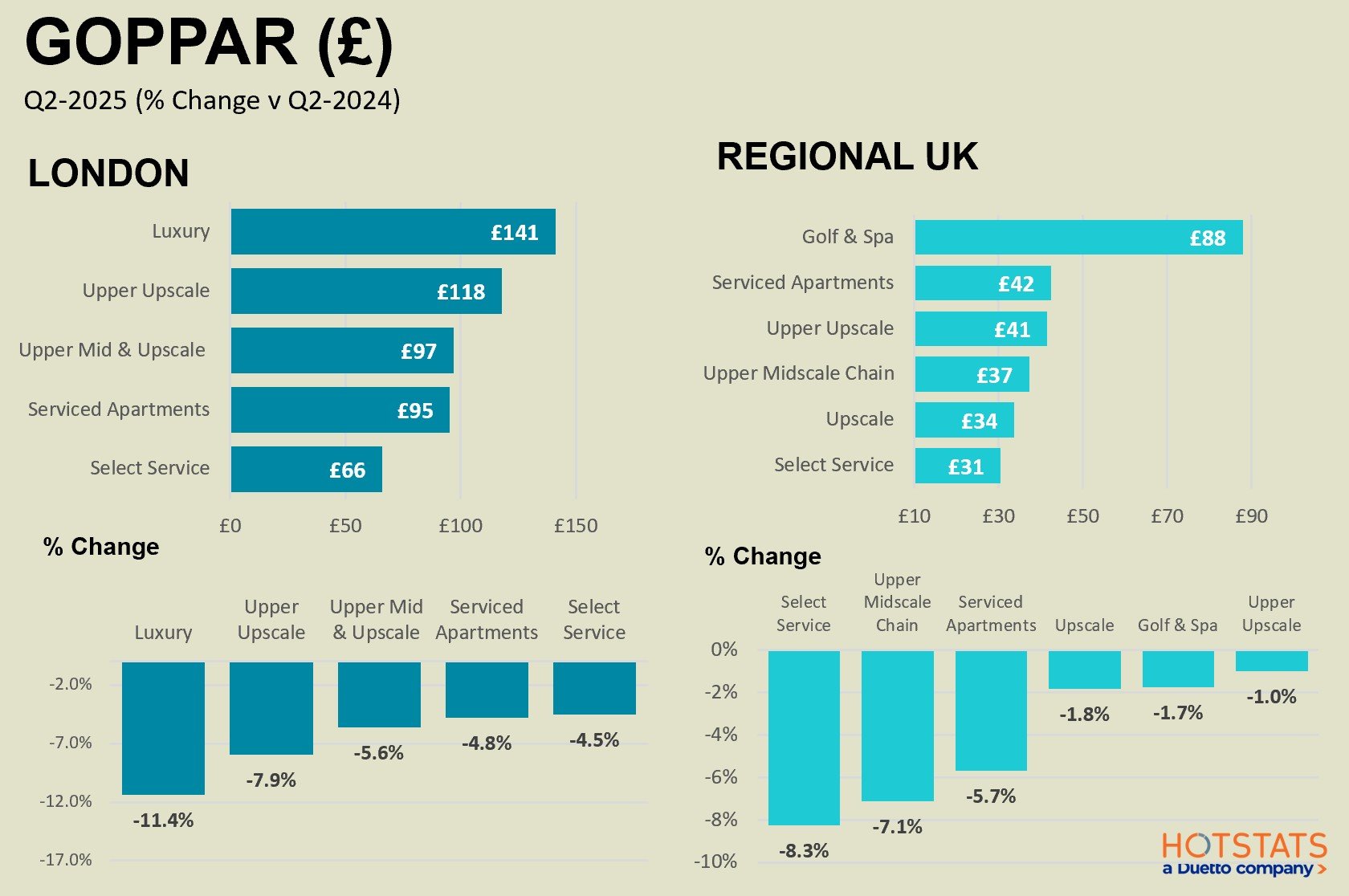

With costs continuing to rise, the UK hotel market has suffered declines in profitability for the second consecutive quarter, with London GOPPAR falling by 8.3% in Q2 and by 4.2% across regional UK. More severe declines were suffered by London’s Luxury (-11%), whilst regional UK’s economy and midscale segments endured declines ranging between 7% and 8%. Meanwhile, London’s profit margin, fell by three percentage points, to average just under 42%. Across regional UK, the profit margin declined by one percentage point to 31%, but this itself shows resilience during a taxing operating environment.

For further detailed analysis of the UK Hotel Market, take a look at Knight Frank’s new look UK Hotel Dashboard

Sign up to Knight Frank Research.