Tenants in waiting?

What the UK’s fastest-growing firms reveal about future retail demand

06 August 2025

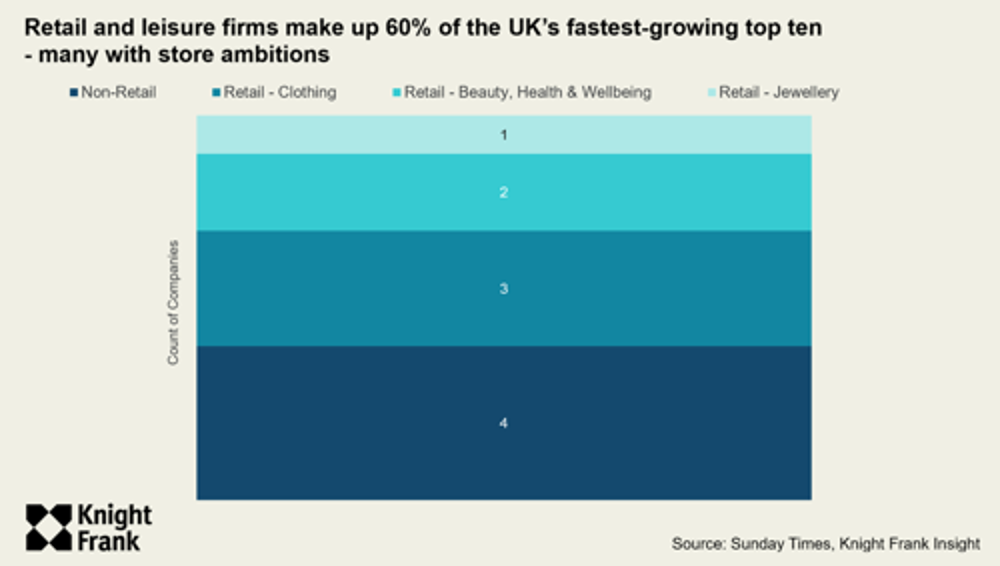

60% of the UK's top 10 fastest-growing companies in 2025 are tied to the retail and leisure sector. This will be of interest to retail landlords across the UK, signalling where future occupier demand for physical retail space may emerge, from high streets to shopping centres, and even retail parks where retail mixes are increasingly diversifying.

[A note on The Sunday Times 2025 methodology: To qualify, companies must be UK-registered, privately owned and independent, with at least £250k in sales in the base year (three years ago) and £5m in the latest year of trading. They must also employ a minimum of five people. The primary measure of growth is CAGR in sales, calculated over three years.]

The dominance of retail and consumer companies among high-growth firms is hardly unexpected. Retail & wholesale remains a major engine of the UK economy, generating 10% of value in 2025, larger than the professional and finance sectors, and projected to reach £249bn by 2030.

But the retail property landscape has evolved. Rather than chasing scale, many occupiers are now building store portfolios with greater precision, shaped by data insights. High-growth companies are no exception and will be targeting locations where the stars (brand, audience, and format) all align.

Physical stores: the natural next step

DFYNE, an activewear brand, tops the list as the UK’s fastest-growing company in 2025 by The Sunday Times, with reported sales growth of +517%. It currently trades online only, but its product category, customer profile, and rate of growth suggest a move into physical retail could be a natural next step.

Stores are a proven way to drive sales. The ‘halo effect’ is well established: online sales actually increase when a store opens, acting as an effective marketing tool, raising awareness in the shopper catchment, and keeping the brand name front of mind.

Other high-growth brands have already made the transition. Odd Muse, a luxury womenswear brand founded in 2020 and growing rapidly (268%), has opened stores in Covent Garden and New York’s SoHo. Rather than large-scale rollouts, it has opted for selective flagship openings in locations that reinforce its brand positioning.

Several high-growth brands from earlier rankings have followed a similar trajectory. Castore (featured in 2023) now operates more than 20 UK stores. ME+EM has opened nine standalone locations. And Gymshark, first identified in 2019, now trades from five stores, with further expansion expected.

In each case, the move into physical retail has marked a shift from digital disruptor to multi-channel operator. For many, opening stores is a deliberate step toward becoming a more mature and established player in the retail sector.

A wider cohort of interest

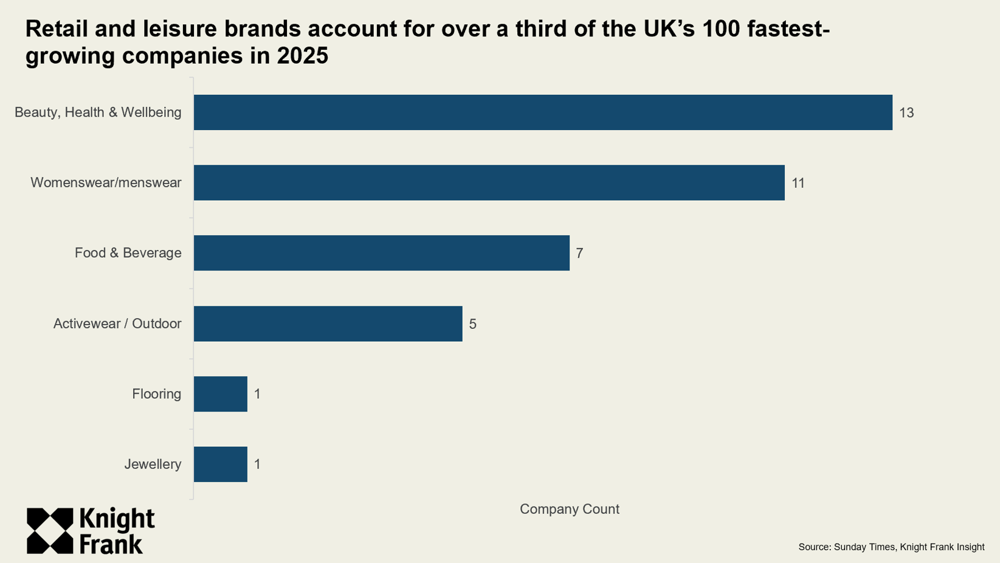

Beyond the top ten, we identify 38 high-growth companies in the broader top 100 with a clear relevance for retail and leisure landlords. These are companies building upon their store portfolio, or are likely to be positioned to do so within the next phase of growth.

The full list is available on request via our research and retail agency teams.

Some 16 high-growth companies are allied to the fashion sector, including Nobody’s Child, Blakely Clothing, and With Nothing Underneath (WNU). Many are in the active, athleisure and outdoor segments (Montirex, Oner Active and Passenger) - categories that benefit from physical product interaction, allowing customers to assess fit, quality and performance in a way online channels struggle to replicate.

Thirteen companies fall under beauty, health and wellbeing, one of the strongest-performing retail sales categories over the past two years. While many of those on the list currently operate online-only, there is a clear opportunity for store formats. For instance, Healf, which offers personalised health supplement subscriptions, could benefit from store formats centred on sampling, advice or consultations.

Seven of the UKs high-growth companies are in the food and beverage (F&B) sector, and include many brands already with a physical presence: Flat Iron, Daisy Green, Wingstop and Coffi Lab.

Location decisions informed by data

Online-only retailers rarely chase national store coverage from the outset. Their first stores are driven by data, not a blind pursuit of scale.

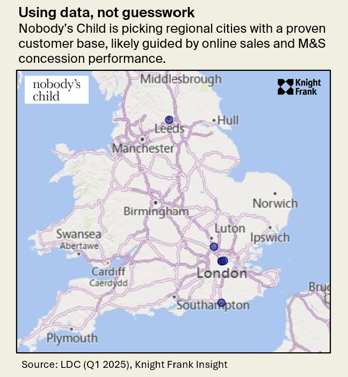

Nobody’s Child, for example, has grown steadily from an online base, building stores across London and, as of this year, in St Albans, its first regional location. The decision is likely to have drawn on postcode-level, geodemographic analysis of online sales, alongside performance data from its M&S store concessions, to identify areas with a high density of existing loyal customers.

Other high-growth companies are signalling longer-term intentions to enter physical retail. Montirex, for example, is due to open a pop-up in Liverpool ONE this autumn, a low-risk test site in its home city, where existing brand familiarity should provide a useful read on sales performance, format preferences, and future store viability.

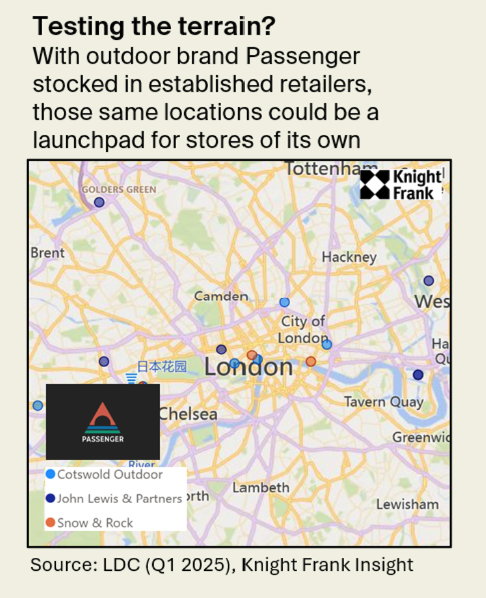

Similarly, Passenger, another high-growth outdoor clothing brand identified, is currently stocked in third-party retail stores such as Cotswold Outdoor, John Lewis and Snow+Rock, and seeking space in the capital. These store partnerships offer valuable insight into where product sells well offline, data which will be informing any future standalone store strategy.

Precision over presence

While many high-growth brands are entering physical retail, most are doing so selectively, prioritising catchment fit over national coverage. This signals a more mature phase in occupiers’ retail strategy, where expansion is driven by audience alignment rather than vanity. The risks of overexpansion in retail are ; what’s emerging is a more disciplined, data-led approach to store growth.

That is not to say these companies won’t be ambitious. Wingstop, the US chicken wing brand, is opening 20 new UK stores this year, following 18 in 2024. New sites include Newcastle, Swansea and Lakeside. Having entered the UK market in 2018, the company now appears to be scaling with greater confidence.

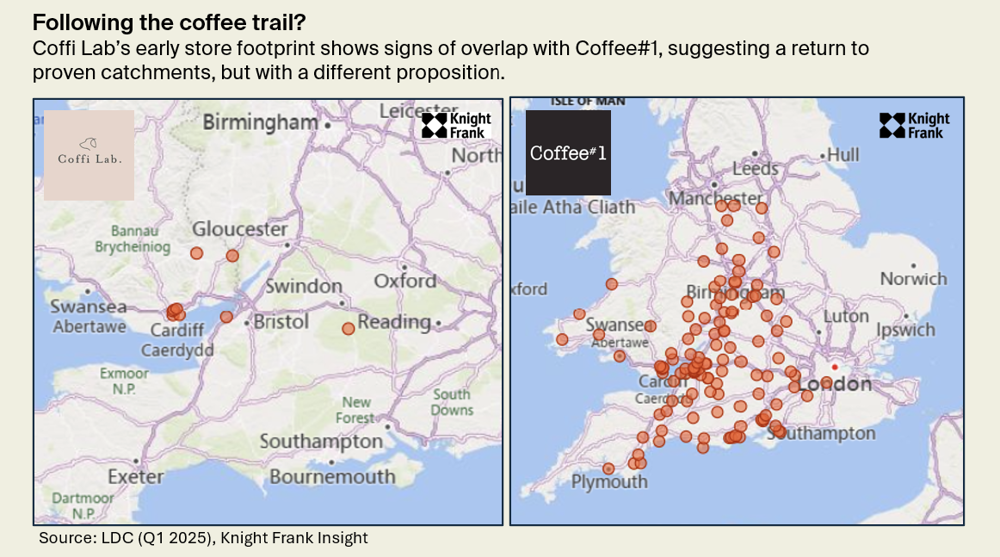

Coffi Lab is taking a more selective and strategic path. Founded by James Shapland, creator of Coffee#1, the dog-friendly café chain has grown to 11 sites, mostly across the South West and Wales. Its location strategy undoubtedly shaped by Shapland’s deep understanding of where, and how, people buy coffee, favouring local catchment fit over national presence. Also, the benefits of scaling up from a distinct regional base, as opposed to opening disparate sites at opposite ends of the country.

Flat Iron, originally a Soho steakhouse, has added regional locations in Manchester, Leeds and Cambridge, with Brighton and Bristol to follow. After a strong trading year in 2024, the group is expected to reach 20 sites by 2025 year end.

Daisy Green, meanwhile, has built a dense portfolio across Central London (Marylebone, Southbank, Soho, South Kensington), and may be nearing the point where regional cities or outer London neighbourhoods become the next logical step.

Data on both sides

For landlords, monitoring high-growth companies is a good way of understanding who the next tenant may be. Many won’t be acquiring space immediately, but some will cross that threshold within the next 12 to 24 months. The challenge is identifying which brands are nearing that inflection point, and where their customer base is most likely to be.

For occupiers, store location strategy is increasingly grounded in data. Physical retail remains where many retailers generate the majority of their revenue, but performance depends on the right catchment, complementary mix, and operational model.

At KF, we work across both sides. Our retail agency and research teams advise on location planning, tenant targeting and rollout strategy using national store databases, demographic tools and competitor analytics to help retailers and landlords make informed decisions.

The class of 2025

We’ve identified 38 high-growth retail brands from 2025 The Sunday Times 100.

Want the full list? Get in touch with our research insight and retail agency teams.

Sign up to Knight Frank Research