Residential Development Land Index Q2 2025

Persistent planning delays and Gateway 2 bottlenecks slow delivery as soft demand and viability pressures weigh on land values

08 August 2025

UK residential development land values dropped in the second quarter as housebuilders grappled with planning delays, viability challenges, skills shortages and weak demand from purchasers.

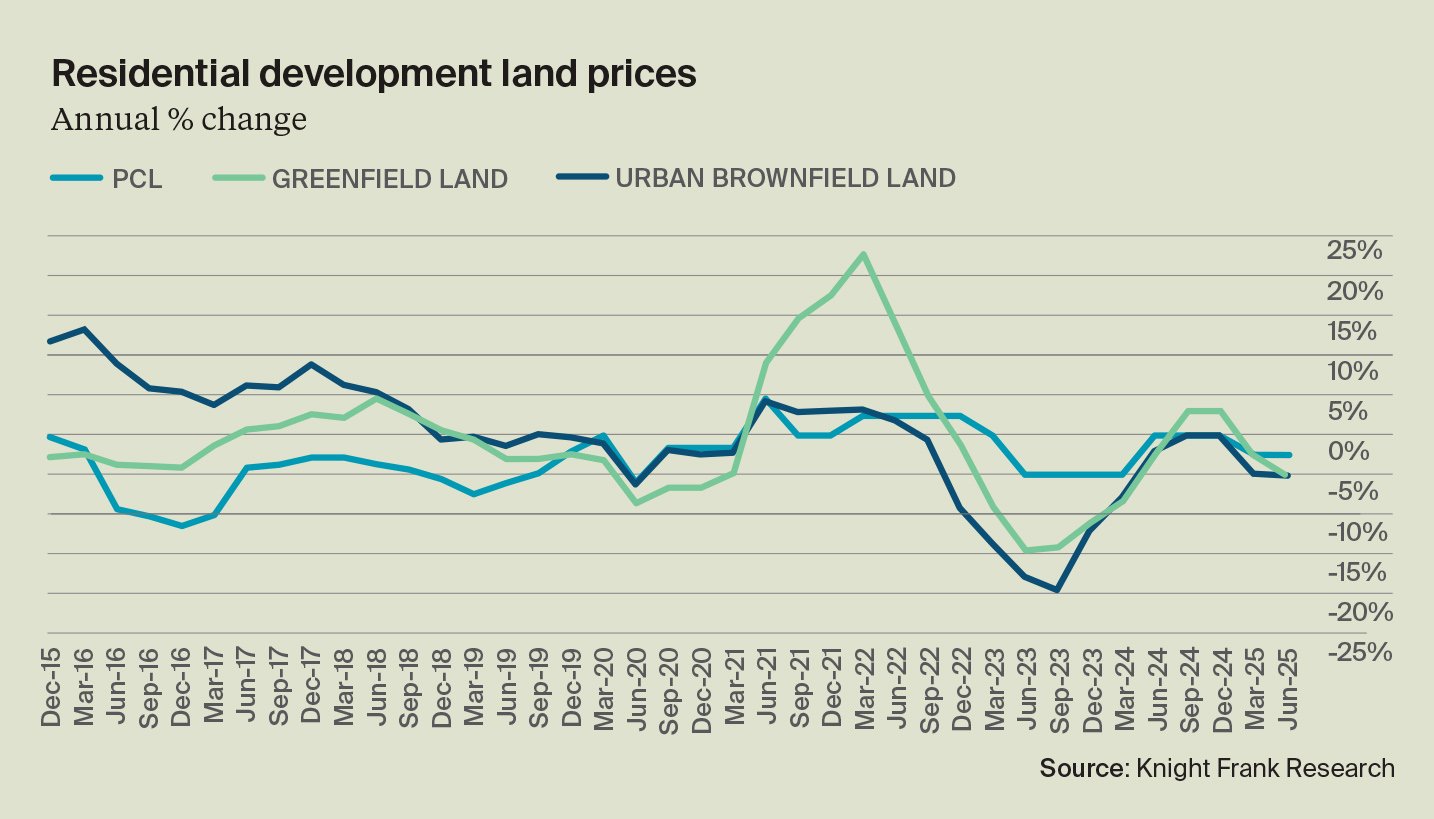

Urban Brownfield land values dropped marginally during the quarter, bringing the annual decline to -5%. Greenfield land values also dropped, bringing the annual decline to 5%. Prime Central London values held steady on the quarter, supported by a lack of supply. That brings the annual decline to 2.5%.

Land values are falling amid substantial drops in output, particularly in the UK’s towns and cities. Developers in London, for example, started just 731 new private units between April and June, the lowest quarterly total ever, according to consultancy Molior London.

Market conditions

Our quarterly survey of small and volume housebuilders suggest conditions have worsened in the past three months, which will weigh further on both land values and output in the second half of the year.

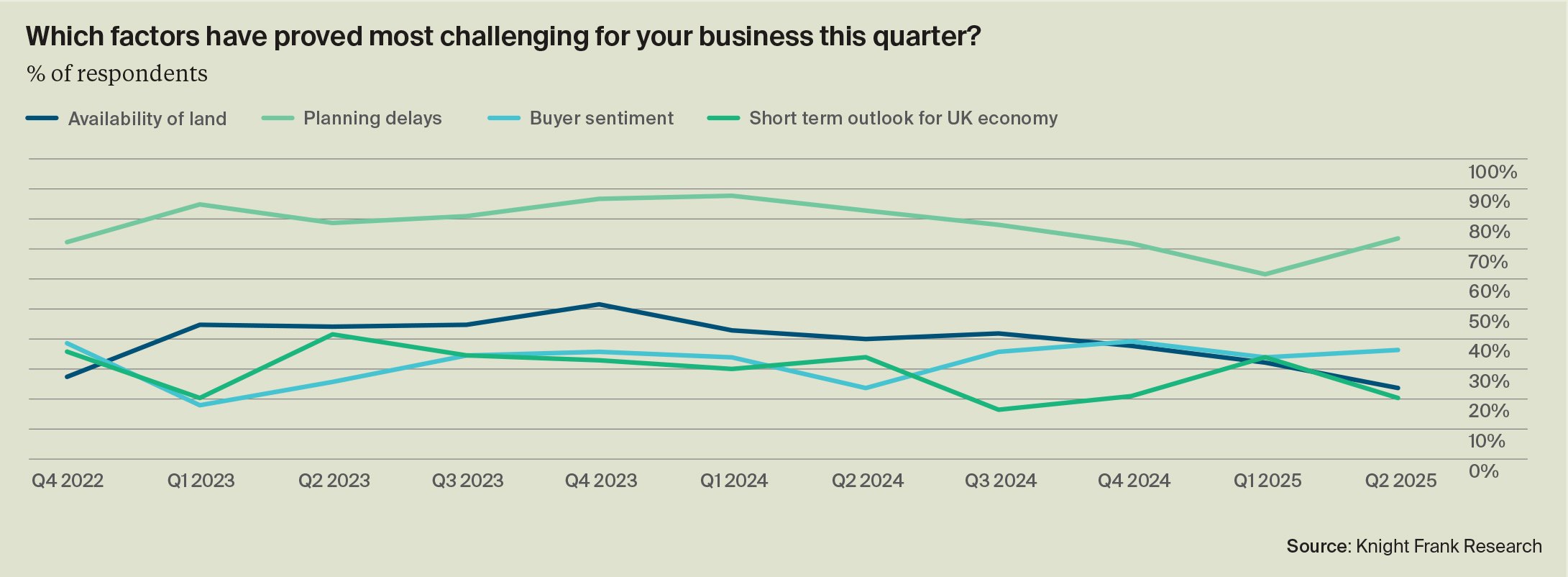

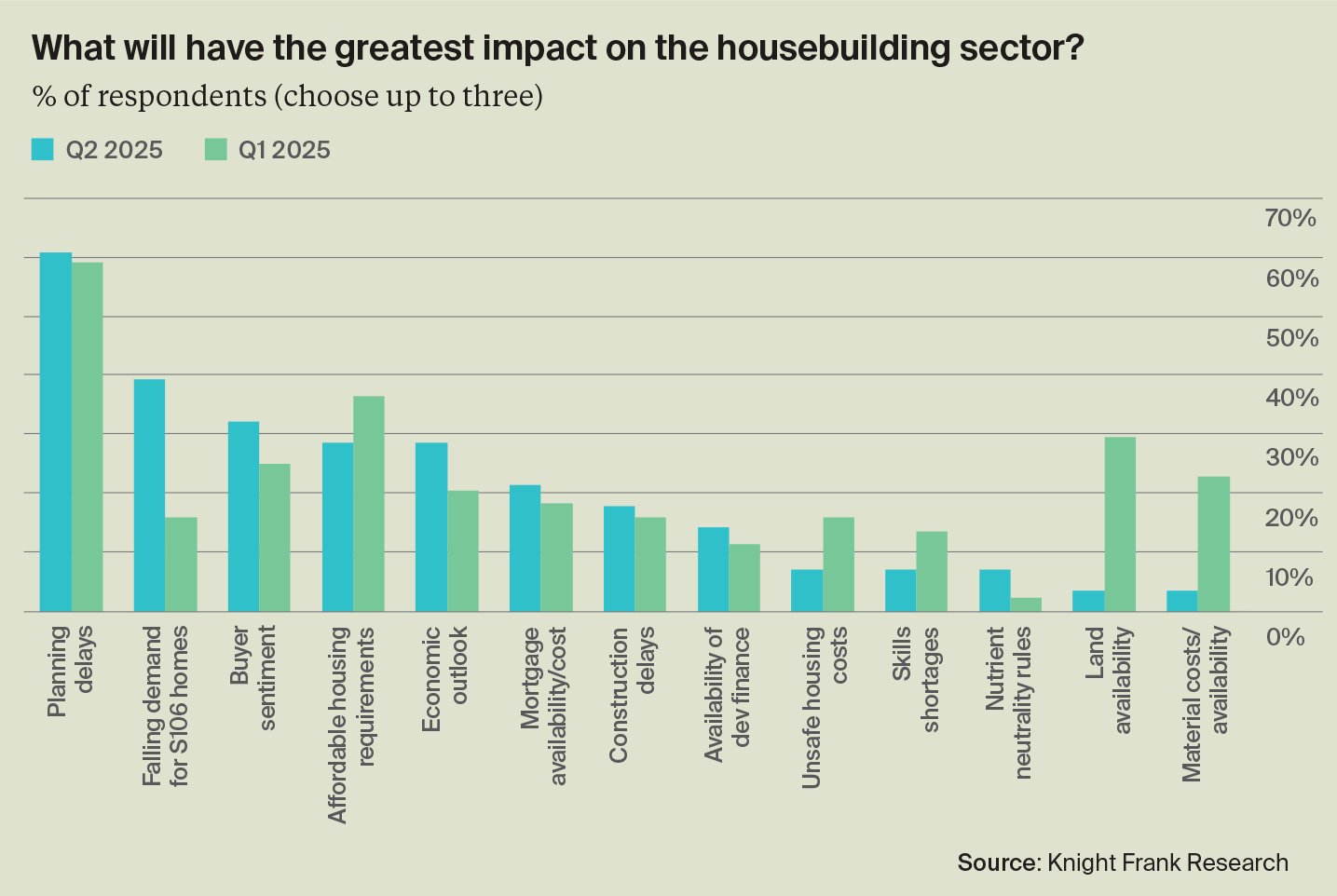

Despite government efforts to speed up planning, almost three quarters of our respondents cited planning delays as their biggest challenge during the quarter, up from 60% in Q1.

This may be a temporary shift; several major housebuilders have expressed optimism that planning reforms already announced will have a positive impact over time. The reinstatement of mandatory local housing targets and a commitment to greenfield/greybelt flexibility has boosted sentiment outside of urban markets. Increased funding for planning departments and the appointment of more officers should soon begin to ease local authority resourcing issues. Persimmon, Barratt Redrow and Bellway have all recently highlighted the updated NPPF and the Planning and Infrastructure Bill as important steps that should support delivery in the medium term, even if near-term challenges remain.

Buyer sentiment followed planning delays at 37%. While there are still fixed rate mortgages available below 4%, the easing in mortgage rates has largely plateaued in recent months. Rising wages will improve affordability in-time, but it’s a slow process and without government support many buyers at the foot of the property ladder continue to struggle to raise deposits.

The low level of registered providers active for Section 106 affordable homes came in third at 27%. The government’s June Spending Review included a £39 billion investment over 10 years for a new Affordable Homes Programme (AHP), which should soon begin to ease financial pressures at Registered Providers (RPs), however it’s unclear how much funding will be geared towards purchasing Section 106 units while RPs grapple with investing in building safety and decarbonization.

High density difficulties

These issues impact developers across the board, but those developing higher density schemes in key employment hubs face unique challenges – particularly when it comes to Gateway 2, a checkpoint in the Building Safety Act for buildings higher than 18 meters, or seven storeys.

While our Q1 index referenced Gateway 2 as a barrier in qualitative terms, Q2 provides concrete scale: our respondents have in excess of 6,600 homes in the Gateway 2 process. The unpredictability of the process, particularly repeated delays, is

meaningfully reducing demand for land and appetite to begin new projects. Of those respondents impacted, nearly half say the process is adding more than 12 months to project timelines. A third expect to wait more than six months for checks to complete. Respondents also highlighted that late-stage viability reviews continue to slow urban schemes by adding uncertainty to project finances and timelines.

Optimism over the long-term

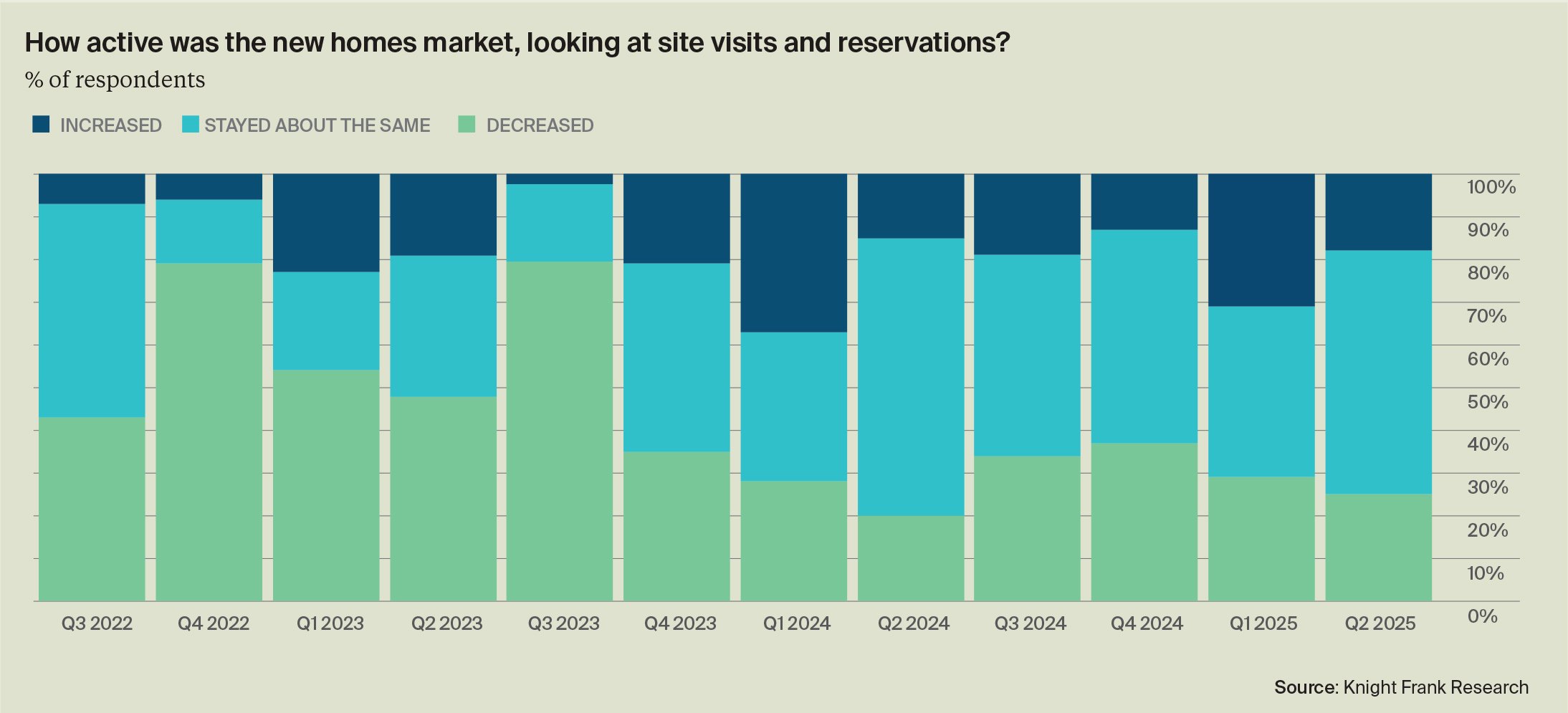

Broader demand indicators remain soft. A quarter of our respondents said site visits and reservations cooled during the quarter, while 57% said they’d remained the same. Respondents are slightly more optimistic over the medium term; 21% expect reservations to tick up in the second half compared to the first, while 18% expect a deterioration. Sixty percent expect no change.

Without buy-side incentives and further supply-side reform, housing delivery is very likely to continue contracting over both the short and medium term. A quarter of respondents expect a fall in starts in the three months through September, compared to 18% that expect an increase. Fifty seven percent expect no change.

Developers’ willingness to begin new projects, a good leading indicator for delivery over the medium term, also remains weak. We asked respondents to list issues preventing them from pursuing planning applications; almost half chose S106 Affordable Housing obligations/viability. Thirty six percent said planning authority resourcing, while 29% said Local Plan delays. More than half (55%) don’t expect to submit more planning applications during 2025 than they did last year.

Those that do seek to increase delivery are struggling to find tradesmen. Four-in-ten housebuilders report struggling to meet output targets in the past twelve months due to labour and skills shortages. Almost half cited bricklayers as the trade most impacted, followed by carpenters and plasterers.

Land values take time to react to market conditions - many landowners have the means to wait for conditions to improve rather than sell at values they deem unattractive. Our respondents do suggest some softening may take place during the coming months; 26% expect land values to fall, while the remaining 74% expect no change.

Economic pressures

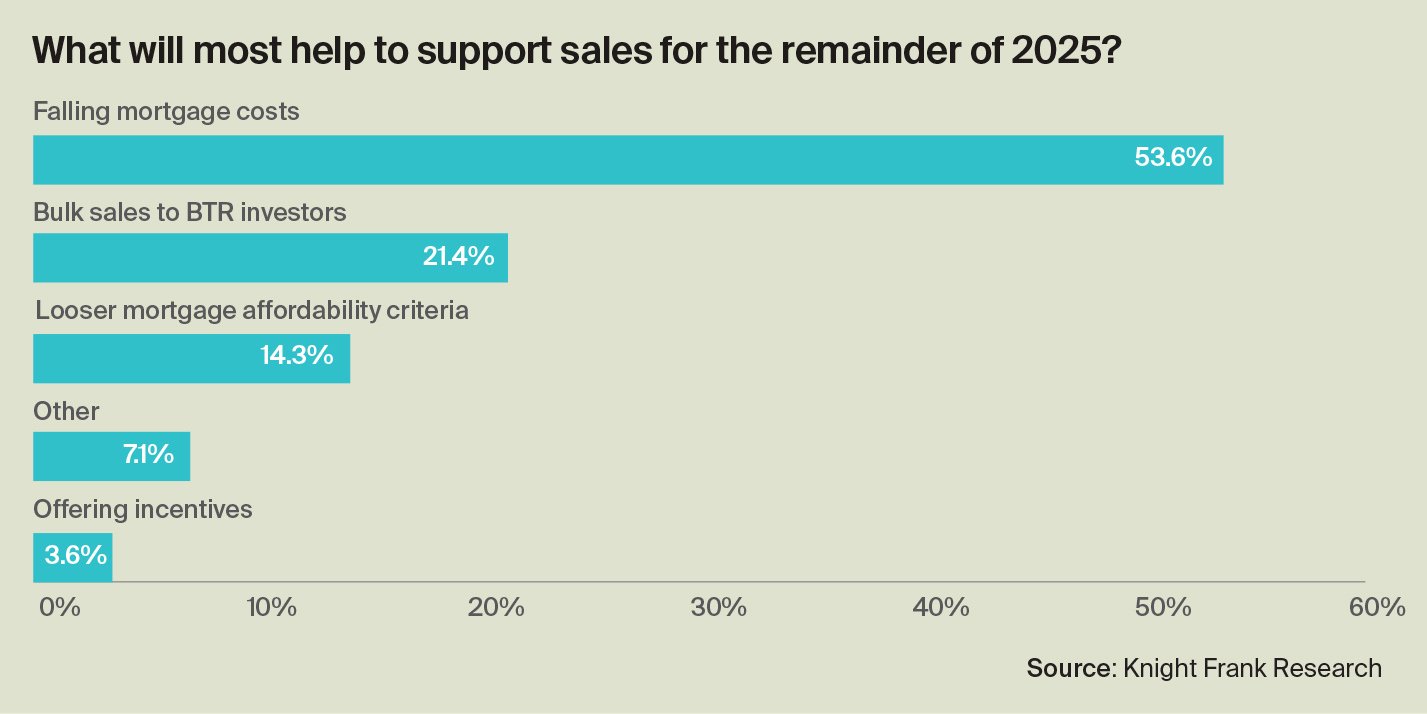

Bank of England policymakers have turned a little more dovish in recent weeks; officials including Governor Andrew Bailey have increasingly emphasised the weak jobs market over the threat of inflation. Developers are hoping easing mortgage rates will bring some relief; more than half of respondents say falling mortgage costs would most help sales through the remainder of 2025, followed by bulk sales to build-to-rent operators or single family housing investors (21.4%) and looser mortgage affordability criteria (14%).

Still, should the BoE continue with its current once-a-quarter pace of cuts, leading fixed rates may drop to around 3.7% by the year end, which is unlikely to unlock delivery at the scale the government is hoping. Rather, achieving that would require a mixture of policy interventions which could include renewed support for first-time buyers, or some efforts to revive the off-plan sales market – a key pillar in the funding and delivery of high density, speculative development. Measures to address viability challenges would also be required, particularly the functioning of the Gateway process and the application of late stage reviews for affordable housing.

Overall, the survey results depict a market constrained by policy delays, weak demand and rising costs, with little short-term relief expected until financing conditions ease or recent planning reforms start to take effect.

Sign up to Knight Frank Research.