Is ESG just inherent in business operations?

In this month’s newsletter we discuss our latest global occupier research (Y)OUR SPACE which shows how ESG is being integrated into real estate strategies, and the UK government’s newest EV incentives.

07 August 2025

Is ESG just inherent in business operations?

ESG is being woven into real estate decisions for occupiers, rather than standing alone. That’s my key takeaway from the 2025 Knight Frank (Y)OUR SPACE report, which captures the views of respondents directly managing some 650 million sq ft of space globally.

The report's tagline ‘Rising to the Challenge’, highlights the complex and often competing demands faced by corporate occupiers today. When asked to rank the top three forces shaping their real estate decision-making, respondents placed growth and innovation first, followed by cost control and volatility. ESG was singled out by just 14%. Is this because ESG is now viewed as a long-term consideration, less urgent than immediate ‘firefighting’? Or has it become so embedded within other priorities that it no longer needs to be called out separately?

The evidence suggests the latter: ESG is interwoven with broader business drivers. While nine out of ten occupiers see real estate as a strategic asset, the main aspects they view it supporting are: operational efficiency and cost management (68%); corporate brand and image (45%); and employee wellbeing (40%), all of which have ESG elements embedded. More efficient buildings may reduce energy costs, amenity-rich and wellbeing focused spaces have been found to improve employee productivity and health, and real estate choices will contribute to business targets and goals.

Yet, only 18% of respondents listed sustainability and ESG commitments among their top three priorities. This may indicate that sustainable, ‘good ESG’ buildings are simply expected by the market, not always the headline priority. This is evident as new and refurbished buildings, often built to rigorous sustainability standards sometimes shaped by planning requirements, account for a growing share of lettings. In London, for example, lettings of new or refurbished office space (typically achieving or targeting a minimum EPC B rating) reached a record high in Q2 2025, with 2.6 million sq ft signed, over 74% of total leased space.

Furthermore, with ESG at its core about risk mitigation and seizing opportunities, resilient buildings will be evermore important as extreme weather becomes the new normal. Nearly two-thirds of occupiers draw this out, noting that sustainability and ESG are ‘somewhat’ or ‘very’ critical to mitigating financial and operational risks. This includes limiting business interruption and managing insurance costs and availability among other value chain influences.

Considered space

Asset owners are prioritising upgrades, with three-quarters pursuing this strategy according to our separate ESG Property Investor Survey. Occupiers recognise the need too: nearly half report that more than a tenth of their portfolio consists of ageing assets requiring significant upgrades or capital expenditure, while 45% say it’s up to 10%.

Delivering the right type and amount of space is critical for owners and developers. As discussed in our Meeting the Commercial Retrofit Series, it is not about defaulting to the highest specification or most amenities, mainly as cost sensitivity rises. Over 40% of occupiers say they will ‘slightly’ or ‘moderately’ reduce the quality of future space due to rising rents and occupancy costs, underscoring the need for considered, efficient space.

Certifications remain important: 45% of occupiers expect to increase the number of sustainably-certified buildings in their portfolio, while half expect it to stay stable. But, as highlighted above, what goes into those certification strategies needs careful consideration.

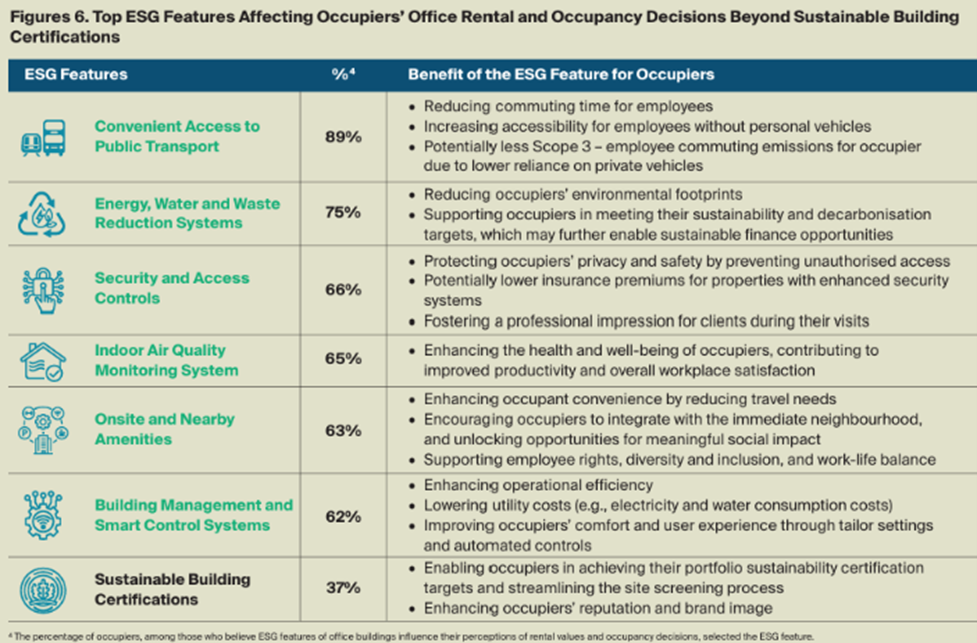

A separate study, from our Hong Kong team, found a disconnect between what landlords deliver and occupier priorities: four of the top six ESG features prioritised by occupiers had adoption rates below 50%, including energy, water, and waste management systems. While 75% prioritise indoor air quality monitoring, less than half of buildings provide it. Interestingly, Hong Kong occupiers are less focused on certifications, reflecting local market nuances and reminding us that context is always key.

More on electric vehicles

The UK government has announced £650 million for grants to support electric vehicle (EV) sales, with motorists able to get up to £3,750 each. The most environmentally sustainable vehicles will receive the most significant grants, with a maximum sales value of £37,000.

Battery electric vehicle sales rose 26% in the three months to June compared to the same period last year, according to The Society of Motor Manufacturers and Traders. They accounted for nearly a quarter of all cars sold in June 2025 and have averaged just over 22% of new cars in the past year. However, this still falls short of the Zero Emissions Mandate target of 28% for 2025.

Range anxiety, inconsistent charging infrastructure, and charging costs remain constraints. Charging at home or a mix of home and public rapid charging is cheaper than running an internal combustion engine, according to Zapmap, but relying solely on public chargers can be more expensive. A Reuters article highlights that EV charging has a ‘pricing problem’, but a Centre for Net Zero trial showed that dynamic pricing can prompt drivers to respond to ‘green’ or ‘plunge pricing’ notifications, supporting grid management and flexibility—something we’ve highlighted in the Modern Industrial Strategy, and through AI opportunities.

On charging availability, the National Audit Office reports that while the target of 300,000 charge points by 2030 is on track, there is an under-provision along strategic road networks. As of July 2024, only 62% of highway service areas met the government’s target of at least six ultra-rapid charge points by 2023. Our research found that 30% of 572 road networks analysed have no rapid or ultra-rapid chargers within 500 metres.

Deployment is growing: rapid and ultra-rapid chargers now make up about one-fifth of all public chargers (17,000), up from under 19% at the end of 2023. For real estate owners, there’s a growing need to provide chargers as EV ownership rises, offering both revenue opportunities and efficient use of space. Solar car ports, highlighted in the Solar Roadmap, present further opportunities to generate energy and power chargers.

For more on the new UK Solar Roadmap, see our takeaways here.

What else I am reading

Heat pump homes to get £200 a year off energy bills, commuting in a heatwave – the need to future-proof transportation infrastructure, real estate owners don’t want to ditch energy efficiency programme in the US, International Court of Justice (ICJ) landmark ruling that states are responsible under international law for the climate impact of the private sector in their jurisdiction.

Sign up to Knight Frank Research.