Chips on the table: Real Estate’s Role in the Semiconductor Race

28 August 2025

Key takeaways

- Semiconductors, also known as chips, are essential for modern technology. They are the foundation of our connected world and are crucial for future technologies like AI and quantum computing.

- The semiconductor industry is a globally interconnected ecosystem. The US and the UK lead in R&D and chip design, while Asia, particularly Taiwan, South Korea, Japan and China, dominates chip manufacturing.

- Governments globally are investing heavily to strengthen domestic semiconductor capabilities. These initiatives aim to reduce reliance on a single region and mitigate risks.

- The semiconductor industry's growth drives demand for specialised real estate, including R&D centres, manufacturing facilities and logistics hubs.

- The industry faces challenges related to sustainability and talent shortages. Leading manufacturers are integrating green technologies to reduce environmental impact and governments are investing in training programs to address the talent gap.

SMALL BUT POWERFUL

Semiconductors - or chips - are the invisible force powering modern life. Found in smartphones, data centres, medical equipment and defence technologies, they are the brains behind many of the systems we rely on every day.

Made primarily from silicon, chips contain billions of transistors that switch electrical signals on and off in patterns of ones and zeros - the binary language powering every email, video, and app we use today. Without them, modern technology wouldn’t exist.

Chips don’t just power today's world; they’re shaping the future. From AI to quantum computing, they underpin the next generation of innovation.

With global demand expected to double by 20301, the semiconductor market is projected to exceed $1 trillion2. It already ranks as the world’s fourth-largest industry, behind oil production, automotive, and oil refining & distribution3. The race to produce them has never been more crucial.

For real estate investors, they also represent one of the most exciting growth opportunities of the decade.

THE GLOBAL LANDSCAPE

The semiconductor industry is a globally interconnected ecosystem in which chips are designed, manufactured, assembled, tested, and packaged before being installed in devices.

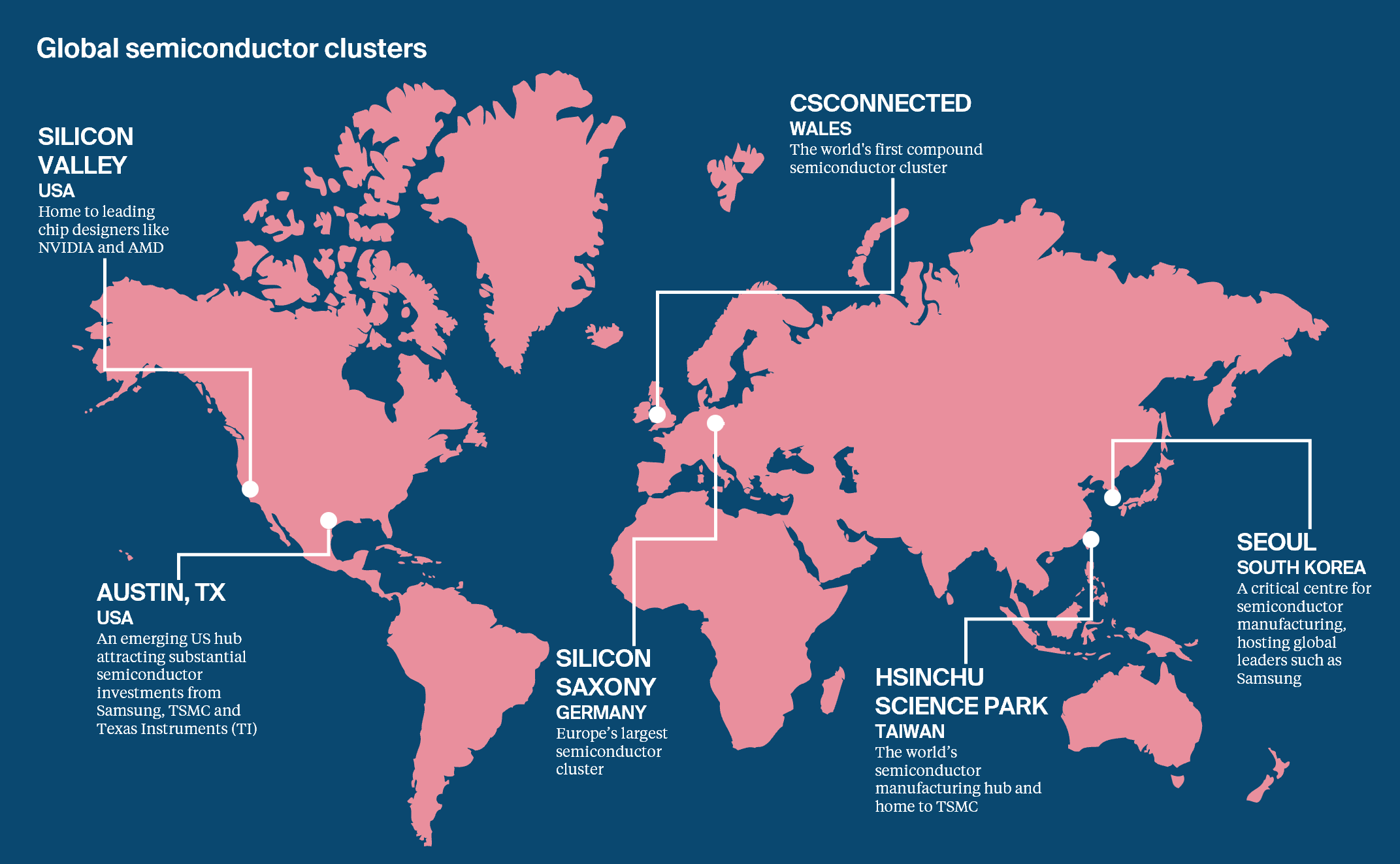

The US and the UK are at the forefront of semiconductor R&D and chip design. Major chip designers like Nvidia and AMD are based in the US, powering AI and gaming advancements. The UK leads in semiconductor intellectual property (IP), with Arm Holdings providing chip architectures in most smartphones worldwide.

Asia dominates chip manufacturing. Taiwan, South Korea, Japan, and China lead the way. Taiwan alone accounts for over 60% of global semiconductor production and 90% of the most advanced chips4. Taiwan Semiconductor Manufacturing Company (TSMC) - the world’s largest contract chipmaker - holds more than half of the global foundry market, suppling industry giants like Nvidia and Apple5. By 2030, China is expected to surpass Taiwan in semiconductor production6.

Beyond fabrication, the assembly, packaging, and testing (AT) phase is even more concentrated. 90% of these processes occur in Asia, particularly in Taiwan and China7.

Supporting this entire process are essential tools and materials from the Netherlands, the US, Japan, and Germany, forming the backbone of the global semiconductor supply chain.

GOVERNMENTS ACT

The heavy reliance on a single region poses significant risks. Geopolitical tensions, trade disputes, or natural disasters could disrupt supply chains. During COVID-19, global chip shortages exposed these vulnerabilities, stalling industries and increasing prices across multiple sectors.

In response, governments are racing to strengthen domestic semiconductor capabilities.

United States

The CHIPS and Science Act (2022) allocated $52 billion for domestic semiconductor manufacturing and R&D8, alongside tax incentives to attract private investment.

Two years later, $32 billion has funded new factories across 15 states9. Notably, TSMC received $6.6 billion in funding for its third manufacturing plant in Arizona, set to begin commercial production before the end of the decade10.

However, future funding is uncertain. President Donald Trump advocates for tariffs over subsidies, potentially affecting long-term investment strategies.

Europe

The EU’s €43 billion Chips Act targets doubling Europe’s global market share to 20% by 203011. The act prioritises research, manufacturing, and skills development.

Major projects include STMicroelectronics’ wafer plant in Sicily13 and Infineon’s €5 billion Smart Power Fab in Dresden14, a manufacturing facility designed for energy and water efficiency.

Yet, slow progress and fragmented funding threaten competitiveness, prompting calls for a streamlined “Chips Act 2.0.”

United Kingdom

The UK’s £1 billion semiconductor strategy focuses on its R&D, IP, and compound semiconductors strengths rather than large-scale manufacturing14.

Key investments include the £20 million ChipStart incubator, backing startups like Wave Photonics, which develops photonic chips for data centres and quantum computing.

The government also acquired a chip factory in Newton Aycliffe, County Durham. It remains the UK’s only producer of gallium arsenide chips, critical for military technologies such as fighter jets15.

Industry experts urge a greater focus on compound semiconductors and an open-access foundry to sustain growth.

THE REAL ESTATE OPPORTUNITY

Governments are investing billions to strengthen domestic chip production and innovation, fuelling demand for specialised real estate to support growth.

LOCATION MATTERS

Semiconductor firms thrive in hubs where universities and chip companies collaborate. Clusters foster innovation, attract talent, and optimise supply chains, driving demand for prime real estate. Locations with strong transport links - motorways, rail networks, and ports - help build resilient supply chains and boost asset value.

REAL ESTATE DEMANDS

The semiconductor industry relies on facilities tailored to each stage of production.

Chip Design and R&D Centres: Office and lab spaces are designed for researchers and engineers to collaborate and innovate. These areas must provide seamless access to cleanrooms, testing labs, and high-performance computing infrastructure. Access to talent, research institutions, and clusters is key.

Manufacturing Facilities (Fabs): Fabs need expansive floor space, substantial investment, and temperature-controlled environments. Cleanrooms are vital to prevent contamination, supported by advanced filtration systems and ultra-clean air. Reliable access to power and clean water is critical to keep operations running smoothly. Raised flooring conceals essential infrastructure such as gas pipes, water lines, and electrical systems.

Assembly and Testing (AT) Facilities: Unlike fabs, which demand ultra-stringent cleanroom environments, AT facilities require less rigorous cleanrooms - yet still essential for maintaining quality. For these operations, location is everything. Proximity to logistics hubs ensures rapid distribution. As firms look to integrate AT earlier in the chip design process, the demand for AT facilities closer to R&D hubs is expected to increase.

Semiconductor investments can trigger broader demand for real estate, including local offices and logistics centres. In locations like Arizona and Dresden, the influx of workers has fuelled urban development, reshaping local economies.

INDIA: A GROWING MARKET

India is rapidly emerging as a semiconductor hub. Its market is projected to reach $110 billion by 203016. As firms diversify supply chains beyond traditional Asian hubs, India’s strategic location, competitive labour costs and growing infrastructure make it a prime destination for high-tech real estate investments.

Recent investors include US chipmaking tool provider Lam Research, committing to invest over $1.2bn in the Indian state of Karnataka over the coming years. The company has signed an agreement with the local government to lease and eventually purchase a land parcel owned by the Karnataka Industrial Areas Development Board (KIADB), located in Whitefield, Bengaluru.

SUSTAINABILITY PRACTICES

Semiconductor fabs are resource-intensive, consuming vast amounts of power, water, and chemicals. As sustainability and efficiency remain top priorities, leading manufacturers are integrating innovative green technologies to reduce their environmental impact.

Micron’s 1 million sq ft fab in Taiwan provides a blueprint for sustainable chip production:

- Chemical recycling - Converts waste chemicals, like isopropyl alcohol, into reusable materials.

- Water reclamation - Recovers 80% of water used during wafer processing.

- Vertical greening - Incorporates nearly 200,000 sq ft of vegetation, regulating temperature and reducing energy consumption.

- Renewable energy - Powered by solar, saving enough electricity for a small town.

As global demand for chips surges, sustainable practices will be crucial for balancing growth with environmental responsibility.

THE TALENT GAP

The industry faces a global talent shortage, with labour gaps already delaying the construction of TSMC's Arizona fabs17.

According to Deloitte, one million additional skilled workers, including technicians and operations specialists, will be needed by 203018.

Governments are investing in training programmes to ensure talent pipelines have the necessary skills. In the short term, companies may rely on internationally skilled workers to bridge the gap, underscoring the importance of flexible immigration policies.

Well-designed workplaces with quality amenities help employers attract and retain top talent.

SO WHAT?

The semiconductor boom offers more than multi-billion-pound fabs, which require significant capital. R&D centres, AT facilities and logistics hubs present accessible, high-value investments that attract long-term tenants.

As the industry expands, demand for supporting real estate - including housing, retail, and leisure - will likely rise, creating further opportunities for investors.

Infrastructure is fundamental. Properties with reliable power, water and transport links are set to attract demand. Investors can also capitalise on utility infrastructure and industrial parks supporting semiconductor clusters.

In emerging markets like India, government subsidies and a strong talent pool make semiconductor-related real estate an attractive investment.

Strategic site selection near talent hubs and logistics corridors will allow investors to capitalise on a growing, government-backed sector while securing long-term value.

References

- European Commission. (2022). European Chips Report.

- McKinsey & Company. (2022). The Semiconductor Decade: A Trillion-Dollar Industry.

- CSConnected. (CM00023).

- The Economist. (2023). Taiwan’s dominance of the chip industry makes it more important.

- Statistica. (2024). Semiconductor foundries revenue share worldwide from 2019 to 2024, by quarter.

- VLSI Research, SEMI, BCG Analysis. (2024). Semiconductor Production Growth Projections.

- Statista. (2022). Share of global semiconductor assembly, testing, and packaging (ATP) capacity in the Asia-Pacific region, by country.

- Congressional Research Service. (2023). CHIPS Act of 2022: Provisions and Implementation (Report R47523).

- National Institute of Standards and Technology (NIST). (2024). CHIPS for America: 2-Year Progress Report Infographic.

- TSMC. (2024) Press Release - TSMC Arizona and U.S. Department of Commerce Announce up to US$6.6 Billion in Proposed CHIPS Act Direct Funding, the Company Plans Third Leading-Edge Fab in Phoenix

- European Commission. (2022). The European Chips Act: Strengthening Europe’s Semiconductor Ecosystem.

- Infineon. Smart Power Fab Dresden Project.

- STMicroelectronics. (2024). New Wafer Plant Investment in Sicily.

- UK Government. (2023). National Semiconductor Strategy.

- UK Government. (2024). UK Defence Supply Chain and Semiconductor Industry Updates.

- India Electronics and Semiconductor Association (IESA). India Semiconductor Market Projection Report 2030.

- CNN. (2024). TSMC delays Arizona chip factory due to labor shortages.

- Deloitte. (2025). Semiconductor Industry Outlook 2025.

Sign up to Knight Frank Research.