What will it take to defrost the US housing market?

Making sense of the latest trends in property and economics from around the globe

27 June 2025

You’d have to go back to Barack Obama’s first presidential win to find a spring selling season this weak in the US housing market.

Sales of existing homes increased 0.8% to an annualized rate of 4.03 million last month, according to the National Association of Realtors. Bloomberg makes that the weakest May since 2009.

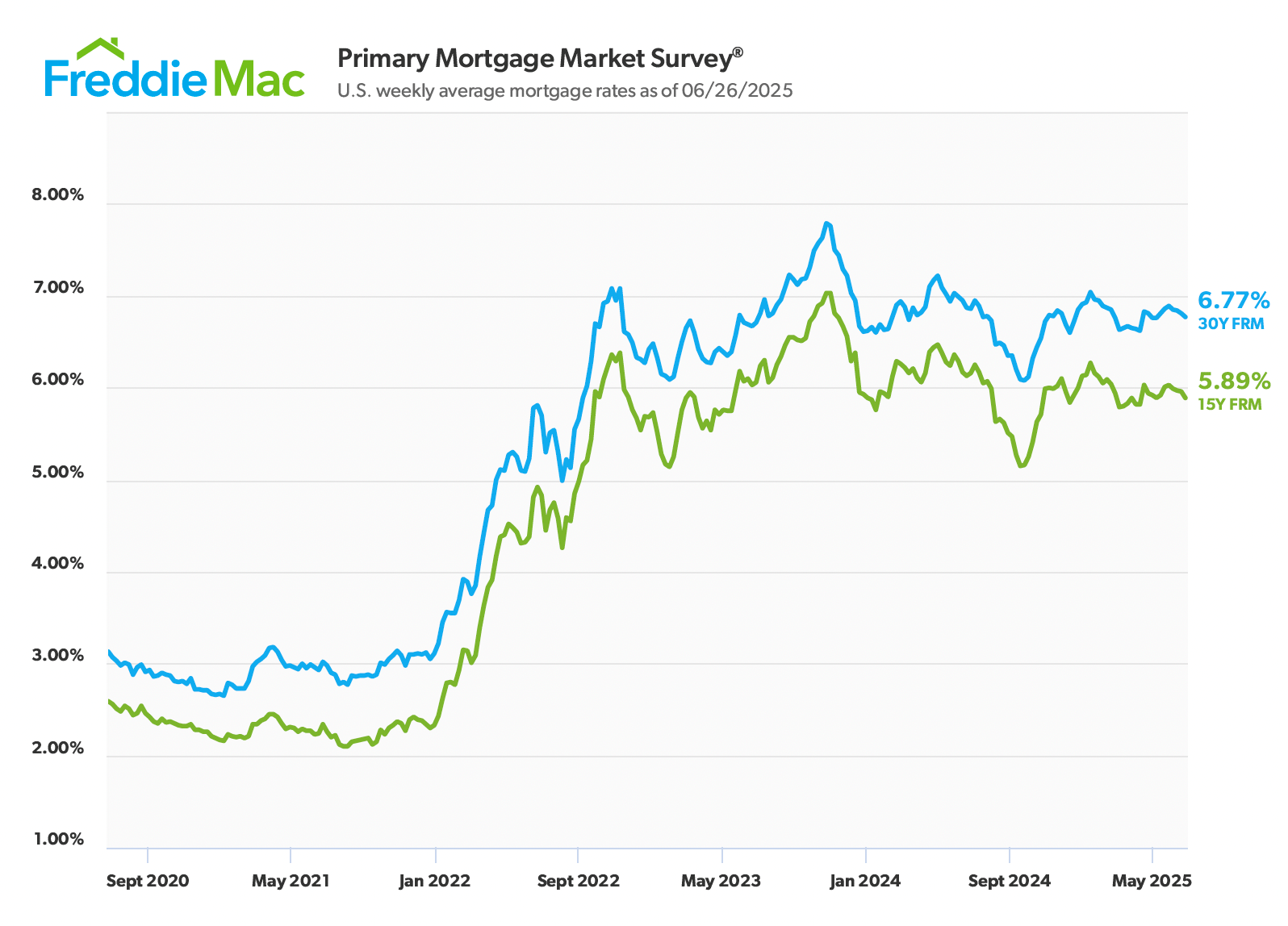

Elevated mortgage rates have effectively frozen the market. Under normal circumstances, you'd expect affordability to be improving by now – the economy is weakening and the Federal Reserve's preferred gauge of inflation is hovering a smidgen above target. That's fertile ground for mortgage rate cuts, but it's not happening to a degree that will coax would-be buyers off of their current rates. Average 30-year rates are still hovering below 7% and have stayed within a 15 basis point range since April (see chart).

Greasing the wheels

Federal Reserve officials aren't sure what to make of the new tariff regime. The Fed's latest projections suggest two rate cuts this year and whether we'll see one this summer looks very uncertain. That uncertainty is preventing mortgage rates from falling, but even when they do, expect marginal declines – the Mortgage Bankers Association reckons the average 30-year rate will sit at 6.7% in 2025, before easing to just 6.4% next year and 6.3% in 2027.

Inventory is now rising, which should help grease the wheels. The 1.54 million units on the market represents a 6.2% increase from the previous month and is a fifth higher than a year earlier, according to the NAR figures. At current sales rates, that would take 4.6 months to shift, up from 4.4 months in April and 3.8 months a year earlier.

“We think that a growing number of homeowners who were holding out for lower rates before moving home are throwing in the towel,” Oliver Allen, senior US economist at Pantheon Macroeconomics, said in a note to clients published in the Bloomberg article linked above.

Still, that's had little impact on pricing so far. Average values edged up 1.3% to a record high for the month of May. That's the 23rd consecutive month of year-over-year increases. Unfreezing the market will be tricky then. Marginal declines in mortgage rates may combine with rising wages to fuel a modest recovery, but that alone would be a slow grind. Meaningful declines in values are the other alternative, and that looks very unlikely – at least for now.

Stark differences

Knight Frank's Q1 Residential Development Land Index highlighted the various obstacles to housebuilding across our major cities.

While inflation has eased and interest rates are expected to fall further this year, the cost of development remains elevated. Labour shortages for key trades, particularly bricklayers and groundworkers, continue to inflate build costs and restrict delivery. For urban schemes, additional constraints linked to Gateway 2 and Section 106 requirements are limiting appetite for sites. Delays associated with the Building Safety Act and viability review mechanisms are adding more risk.

The policy landscape doesn't yet account for the stark differences in outlook between volume building in the suburbs and countryside, and development in our urban centres. In London, the situation is now very serious indeed – Molior London's Tim Craine Over said his team had visited 800 development sites with planning permission across London, and only seven developments commenced construction during Q2 2025. The firm expects fewer than 2,000 private housing starts in the first half of 2025, and completions could wilt to fewer than 5,000 private homes by 2028.

A reminder that London needs 88,000 additional homes a year to meet current and future demand, according to government estimates. For more on this topic, read this piece by Oliver Knight, published yesterday.

Breaking the rules

I talked on Wednesday about the degree to which the government's tax and spending plans rely on famously optimistic productivity forecasts from the Office for Budget Responsibility.

Successive governments have viewed real estate as an easy target for taxation, so whether or not Chancellor Rachel Reeves manages to maintain her wafer thin headroom of about £10bn could be among the key questions for the housing market through the next three years. Not long after the government's spending plans were announced in March, Bloomberg Economics pointed out that a mere 0.6% rise in gilt yields would be enough to wipe out the headroom, leaving Reeves with the choice of raising taxes, cutting spending or breaking their own fiscal rules.

The government is at the mercy of forces well beyond its control, and that includes its own MPs. In the face of a parliamentary rebellion, the government has offered to water down its proposed cuts to welfare – the offer, which still might not go far enough, according to the Times, would cost the Treasury £1.5 billion. The concession would require Reeves to “raise taxes or find other savings," the Institute for Fiscal Studies tells the paper.

In other news...

Knight Frank's Jennifer Townsend unpacks the government's ten year industrial strategy.

Elsewhere – Developer Jamie Reuben: ‘London needs to make foreign investors feel welcome’ (FT).

Sign up to Knight Frank Research.